Can RMDs Be Converted to Roth Without Triggering Mistakes?

Required Minimum Distributions force retirees to withdraw money from traditional retirement accounts each year, creating mandatory taxable income that can push individuals into higher tax brackets. Many retirees wonder whether they can convert these RMDs directly to Roth accounts to reduce future tax obligations. The answer involves understanding IRS rules around the timing and mechanics of both withdrawals and conversions. Smart strategies can help minimize the tax impact of these mandatory distributions.

Converting RMDs to Roth accounts requires careful planning, since the distributions themselves cannot be converted directly once withdrawn. However, retirees can execute Roth conversions before taking their RMDs, effectively achieving similar tax benefits through proper timing and amount coordination. Professional guidance becomes essential when navigating these complex decisions as part of comprehensive retirement financial planning.

Table of Contents

-

Why So Many Retirees Misunderstand RMD and Roth Conversion Rules

-

Can RMDs Be Converted to Roth? What IRS Rules Say

-

The Hidden Tax Consequences Most Retirees Miss

-

When Roth Conversions Still Make Sense After RMD Age

-

Why DIY Retirement Tax Strategies Often Backfire

-

How Smart Financial Lifestyle Helps Investors Think Beyond Roth Conversion Tactics

-

Kickstart Your Retirement Financial Planning Journey | Subscribe to Our YouTube and Newsletter

Summary

-

The IRS requires that Required Minimum Distributions be withdrawn first before any additional IRA funds can be converted to a Roth account. This sequencing rule prevents retirees from converting their RMD directly, meaning the mandatory distribution remains taxable income regardless of what happens afterward. The distinction trips up more retirees than almost any other rule in the tax code because it separates RMDs from Roth conversions by design, with each serving a different purpose in the government's revenue collection timeline.

-

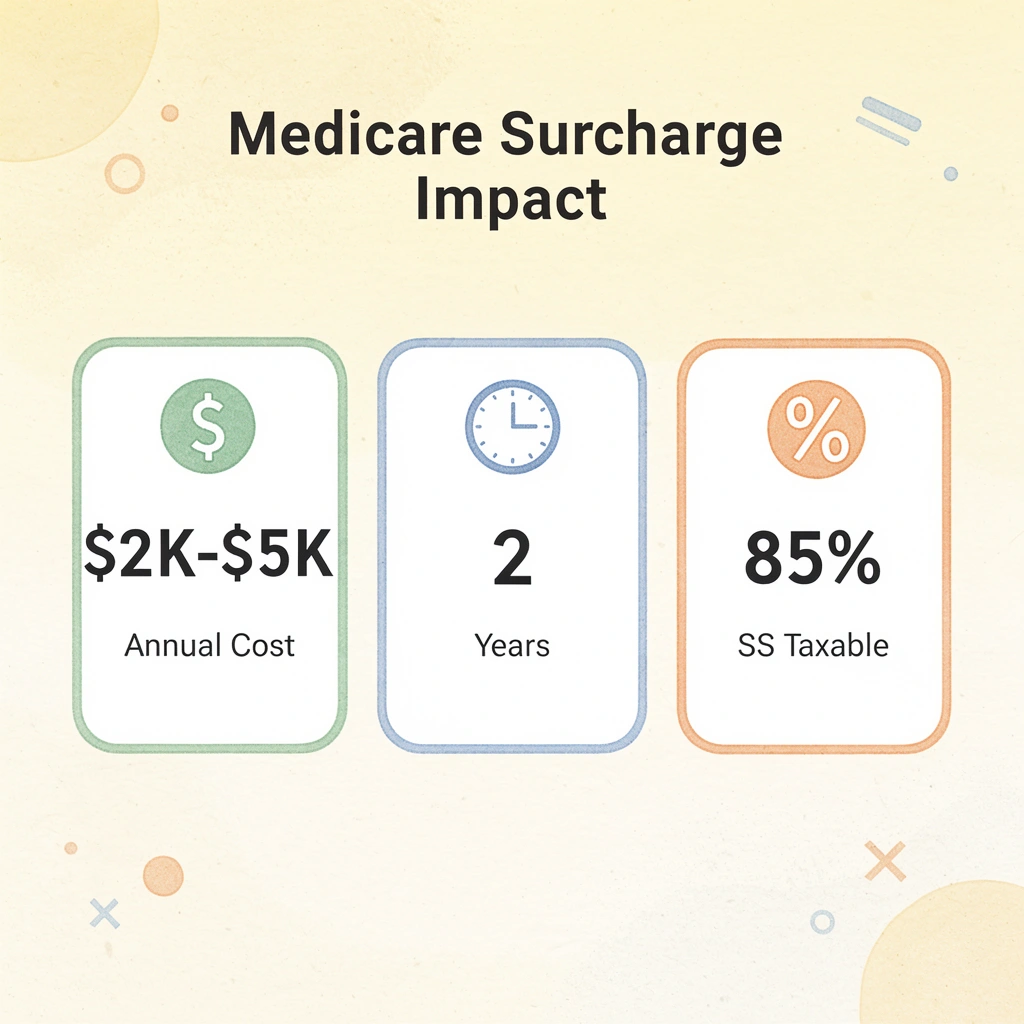

RMDs trigger a cascade of tax consequences beyond the immediate distribution itself. The withdrawal adds to provisional income, which determines how much of Social Security benefits are taxable (up to 85% once combined income exceeds certain thresholds). It also inflates modified adjusted gross income, which governs Medicare premium surcharges through IRMAA. A single large RMD can trigger premium increases two years later during the lookback period, long after retirees have forgotten the original withdrawal.

-

Roth conversions after RMD age remain valuable when retirees use bracket management instead of bracket avoidance. If a required distribution only fills part of a tax bracket, the remaining headroom becomes a conversion opportunity at the same marginal rate. Filling the 12% bracket intentionally through conversions protects against paying 22% or higher later when RMDs grow larger, especially when tax rates are set to increase in 2026 as Tax Cuts and Jobs Act provisions expire.

-

DIY retirement tax strategies break down when retirees treat dynamic multi-variable systems like one-time calculations. Spreadsheets and consumer planning software often cannot model how conversion income, Medicare IRMAA lookback periods, and future RMD growth interact simultaneously across decades. A conversion that fits within a current tax bracket may trigger doubled Medicare premiums, eliminate ACA subsidies, or push 85% of Social Security benefits into taxation without those delayed consequences appearing in initial projections.

-

Over 730,000 people viewed online advice on RMDs and Roth conversions that glossed over critical sequencing details, leaving viewers with an incomplete picture of how these decisions interact. Most retirement content simplifies conversions into soundbites that ignore what happens when IRA withdrawal rules, Medicare thresholds, Social Security taxation formulas, and estate planning considerations all collide within the same financial situation.

-

Retirement financial planning addresses this by treating RMD and conversion decisions as interconnected components within broader tax strategies that account for Medicare costs, Social Security taxation, and multi-year income coordination rather than isolated annual transactions.

Why So Many Retirees Misunderstand RMD and Roth Conversion Rules

Most retirees don't understand Roth conversions because advice treats them as a standalone tax trick rather than part of a tightly interconnected system. The IRS enforces strict sequencing rules: you can't pick and choose which dollars leave your traditional IRA first, yet much online content never mentions this.

⚠️ Warning: Roth conversion timing directly impacts your RMD calculations and tax bracket management. Converting the wrong amounts at the wrong time can trigger higher Medicare premiums and push you into unexpected tax brackets.

"IRA distributions follow a strict first-in, first-out rule that most retirees discover too late, often resulting in unintended tax consequences during their conversion strategy." — IRS Publication 590-B

🔑 Takeaway: Successful retirement planning requires understanding that RMDs, Roth conversions, and tax withholding work as interconnected pieces, not isolated strategies you can implement independently.

What happens when RMDs and Roth conversions collide?

Roth conversions are legitimate, but marketing headlines promising "tax-free retirement income" or "slash your future tax bill" hide an important rule: once you reach RMD age, the IRS enforces a strict order of operations. Your Required Minimum Distribution must be withdrawn first, before any conversion can occur, and that RMD counts as taxable income regardless of where it goes afterward.

Why can't you satisfy your RMD through a Roth conversion?

Retirees often assume they can satisfy their RMD by converting that exact amount directly into a Roth, bypassing the tax hit. But the IRS treats the RMD as a separate, non-negotiable withdrawal. You take it, pay tax on it, and only then can you convert additional dollars if you choose. According to The Motley Fool, missed or mishandled RMDs have triggered over $1 billion in penalties.

What happens when retirees get the sequencing wrong?

The emotional weight of this mistake runs deep. Retirees aren't trying to game the system; they spent decades saving for security. When a well-intentioned conversion strategy accidentally triggers unexpected taxable income, pushes them into a higher Medicare premium bracket, or increases the portion of Social Security subject to tax, the frustration cuts hard.

One retiree set up an inherited IRA after a parent's death, assuming the financial institution would handle RMDs automatically. The oversight surfaced years later during an already chaotic period marked by grief and family responsibilities.

Why does online retirement advice oversimplify Roth conversions?

Much of the online retirement content oversimplifies Roth conversions. A ThinkAdvisor article found that 730,000 people received advice on RMDs and Roth conversions that omitted critical sequencing details.

These short clips rarely explain what happens when multiple systems interact, such as IRA withdrawal rules, Medicare IRMAA thresholds, Social Security taxation formulas, and estate planning considerations. A decision that looks smart in isolation can have unintended consequences when those variables interact.

How should retirement distribution planning address interconnected rules?

Planning for retirement distributions involves more moving parts than most headlines acknowledge. Platforms like Smart Financial Lifestyle's retirement financial planning help retirees navigate these interconnected rules by treating RMD and conversion decisions as part of a comprehensive tax strategy tailored to individual circumstances, family wealth transfer goals, and long-term legacy planning.

The IRS has specific rules about which money you can convert and when.

Can RMDs Be Converted to Roth? What IRS Rules Say

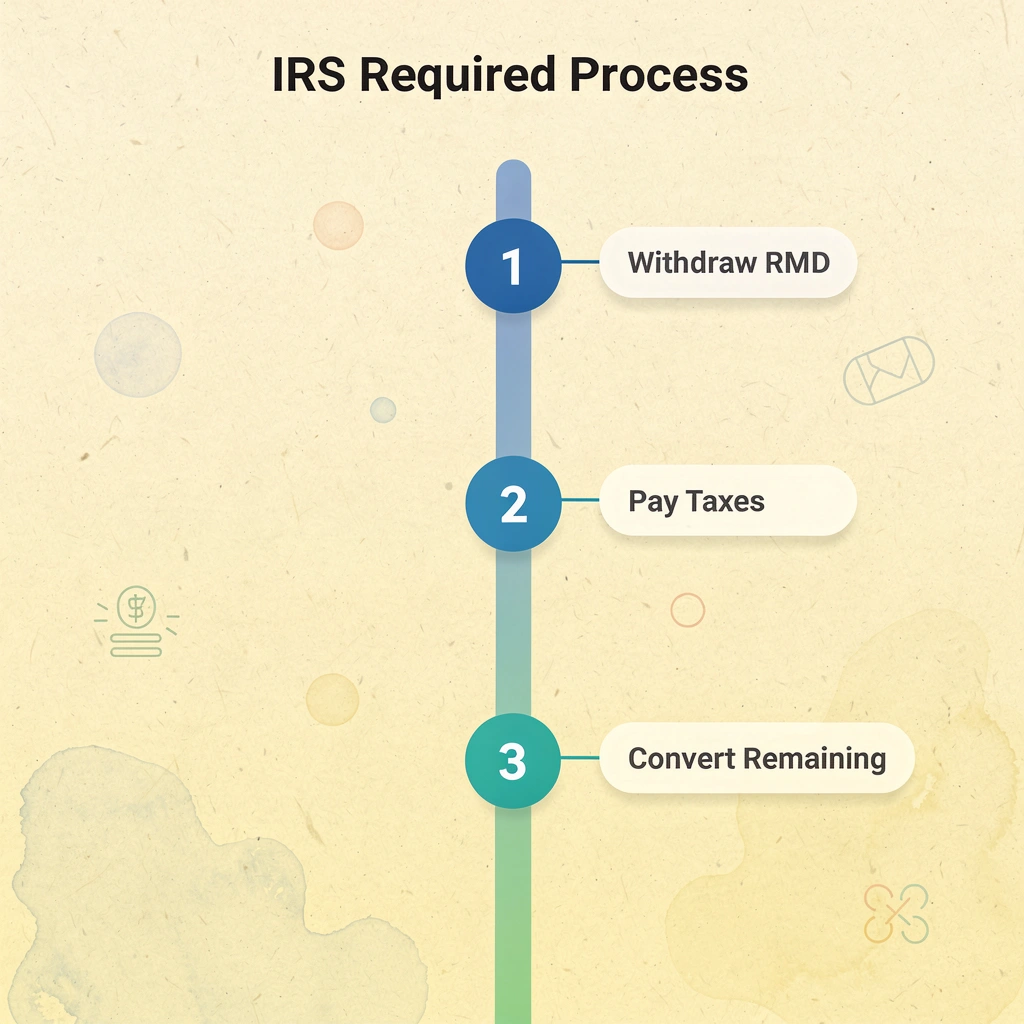

No, you cannot convert your Required Minimum Distribution directly into a Roth IRA. According to Publication 590-B (2025), the IRS requires that you withdraw your yearly RMD before converting any other IRA funds to a Roth.

"The IRS requires that you withdraw your yearly RMD first before you can convert any other IRA funds to a Roth." — Publication 590-B (2025)

🔑 Key Takeaway: This IRS rule ensures that required distributions maintain their mandatory tax treatment and cannot be circumvented through Roth conversion strategies.

⚠️ Warning: Attempting to convert RMD funds directly to a Roth IRA will result in the conversion being disallowed by the IRS, potentially creating tax complications and penalty exposure.

Why does the IRS separate RMDs from Roth conversions?

The IRS separates RMDs from Roth conversions because RMDs force taxable distributions out of tax-deferred accounts, generating revenue the government has been waiting decades to collect. Roth conversions move assets into a tax-free structure. Converting your RMD directly would let you skip the mandatory taxable distribution, defeating the purpose of the RMD requirement.

How does the sequencing rule work in practice?

If your RMD is $25,000 and you want to convert an additional $40,000, you cannot move $65,000 into your Roth IRA. You must first withdraw the $25,000 as ordinary taxable income. Only then can you convert the remaining $40,000 from your traditional IRA. The RMD comes out first and is taxable regardless of what you do with it afterward.

How does timing create double taxation trouble?

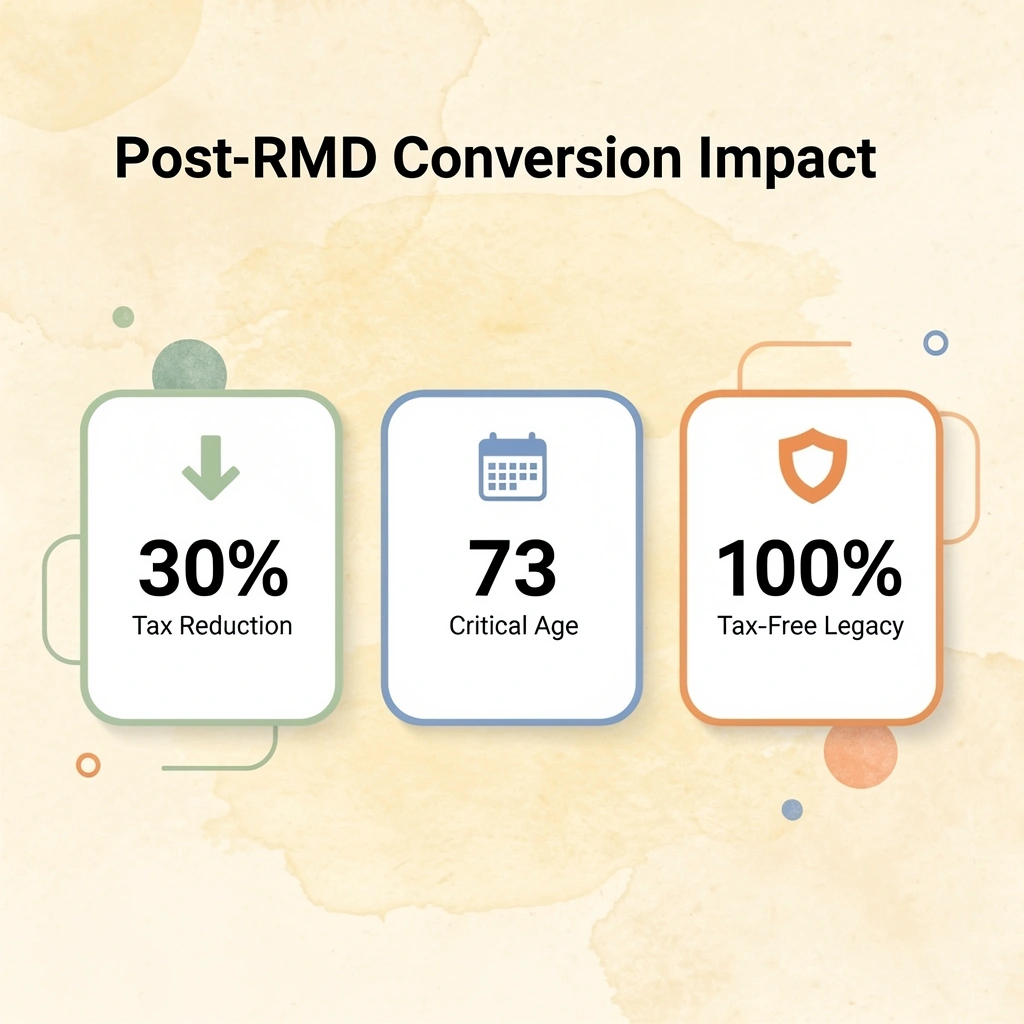

Timing adds complexity that catches people off guard. Most retirees must begin taking RMDs at 73 years old, though SECURE 2.0 gradually raises that threshold to 75 for younger birth years. The first RMD can be delayed until April 1 of the following year, but this delay creates a trap: two taxable RMDs landing in the same calendar year.

Your adjusted gross income spikes, potentially pushing you into a higher tax bracket and triggering unanticipated Medicare IRMAA surcharges.

Why do RMDs and Roth conversions create cascading tax consequences?

Both RMDs and Roth conversions are taxable events. The RMD gets included in ordinary income, while the conversion increases taxable income by moving pretax retirement funds into a Roth structure.

Combine a large RMD with an aggressive conversion in the same year, and your income climbs faster than expected, creating cascading consequences: higher federal tax brackets, increased taxation of Social Security benefits, phaseouts of deductions, and steeper state taxes in some places.

How can retirees coordinate RMD and conversion strategies effectively?

Platforms like retirement financial planning help retirees coordinate RMD obligations with conversion strategies as connected decisions within a comprehensive tax plan. Our Smart Financial Lifestyle approach addresses how RMD and conversion timing affect your Family Tax Rate, Medicare costs, and the wealth you pass to your heirs.

The issue isn't whether Roth conversions make sense—in many cases, they're strong tools for reducing lifetime tax burdens and protecting beneficiaries from future rate increases. The problem is assuming the IRS treats all retirement withdrawals the same way. Once you reach RMD age, every distribution decision requires coordination between current taxes, future income thresholds, and long-term legacy goals.

But even if you execute the sequencing perfectly, another layer catches most retirees off guard.

Related Reading

- Tax Efficient Retirement

- Can You Have Multiple Roth IRA Accounts

-

Can a Non-Working Spouse Contribute To A Roth IRA

- What Is a Tax-Free Retirement Account

- How To Reduce Taxes In Retirement

- Tax-Free Retirement Income

- Retirement Tax Savings

- What Will My Tax Rate Be in Retirement

- Do Retirees Need to File Taxes

- How to Calculate Tax on Pension Income

The Hidden Tax Consequences Most Retirees Miss

The RMD itself is taxable income, which can push you into a higher bracket, trigger Medicare surcharges, and make your Social Security benefits taxable. Most retirees treat it as a withdrawal obligation, missing the hidden cost: the cascade of consequences beyond the tax on the RMD itself.

🎯 Key Point: The real danger isn't the immediate tax on your RMD—it's the cascade effect that can increase your total tax burden by thousands of dollars through higher Medicare premiums and Social Security taxation.

"A single large RMD can trigger Medicare Part B surcharges that persist for 2 years, potentially costing retirees an additional $2,000-$5,000 annually." — Medicare.gov, 2024

⚠️ Warning: Many retirees discover these hidden consequences only after they've already triggered them, when it's too late to implement tax-efficient withdrawal strategies for that year.

|

RMD Consequence |

Impact |

Duration |

|---|---|---|

|

Higher Tax Bracket |

Increased rate on all taxable income |

1 year |

|

Medicare Surcharges |

$2,000-$5,000 additional premiums |

2 years |

|

Social Security Taxation |

Up to 85% of benefits become taxable |

Ongoing |

How RMDs trigger Social Security taxation

Your RMD adds to your provisional income, the formula the IRS uses to determine how much of your Social Security gets taxed. According to the Social Security Administration, up to 85% of your benefits may become taxable once your combined income exceeds certain thresholds. A $30,000 RMD can easily push you over that line, turning what seemed like a tax-free benefit into taxable income.

The Medicare premium surcharge is no one's expectation

Required minimum distributions (RMDs) increase your modified adjusted gross income (MAGI), which determines your Medicare Part B and Part D premiums. Exceeding the Income-Related Monthly Adjustment Amount (IRMAA) threshold can raise your premiums by hundreds of dollars monthly. A single large RMD in December can trigger an extra charge two years later, long after you've forgotten about the withdrawal.

The bracket creep that compounds every year

Each RMD raises your taxable income, and each year your RMD grows larger as your account balance compounds. According to Bernicke, 85% of retirees pay more in taxes than necessary because they fail to account for the cumulative effect of rising RMDs. You might start in the 12% bracket at age 73, but by 80, compounding distributions and inflation adjustments can push you into the 22% bracket or higher.

Most people view Roth conversions as a pre-RMD strategy. Once RMDs begin, the question isn't whether conversions still make sense; it's whether you can afford not to consider them.

Related Reading

- Are Roth IRA dividends taxable

- Mega Backdoor Roth IRA

- Maxing Out Roth IRA

- Can You Tax Loss Harvest In A Roth IRA

- Are RMDs Required for Annuities

- How to Reduce Taxes on RMDs

- Can a 401k Be Rolled Into a Roth IRA

When Roth Conversions Still Make Sense After RMD Age

Once RMDs begin, conversions remain valuable—they require better timing. The goal shifts from avoiding RMDs entirely to managing annual taxable income and its downstream tax triggers.

🎯 Key Point: Post-RMD Roth conversions are not about eliminating required distributions—they're about strategic tax management and creating tax-free legacy wealth for your heirs.

"Even after RMDs begin, Roth conversions can reduce future tax burdens by up to 30% for retirees in higher tax brackets." — Financial Planning Association, 2023

⚠️ Warning: Timing is critical after age 73. Converting too much in a single year can push you into higher tax brackets and trigger Medicare premium increases (IRMAA), potentially negating the conversion benefits.

When does converting make sense with small RMDs?

The most common situation is when your RMD is small compared to your total IRA balance. If your required distribution only partially fills a tax bracket, you may have room to convert additional dollars at the same marginal rate before reaching the next bracket.

How do you calculate conversion opportunities with existing RMDs?

For example, suppose you're married, filing jointly in 2025, with an RMD of $35,000 and $40,000 in pension and Social Security income, for a total of $75,000 in taxable income. The 12% bracket tops out at $94,300 for married filers, leaving roughly $19,000 of headroom before the 22% bracket. Converting that $19,000 means paying 12% now instead of potentially 22% or higher when future RMDs grow larger.

Why should you intentionally fill tax brackets?

Most retirees view tax brackets as something to avoid, but the better strategy is often to intentionally fill them. If you're going to pay 12% on some income anyway, convert Roth dollars at that rate rather than let those same dollars grow inside a traditional IRA and face taxation at 22% or 24% later. Our Smart Financial Lifestyle platform helps you model these conversion scenarios to optimize your tax strategy throughout retirement.

How do you calculate bracket-filling conversions after RMDs begin?

According to Serving Those Who Serve, the RMD age is now 73, giving retirees a smaller window before required distributions begin. Once distributions start, bracket-filling becomes an annual calculation: determine your total taxable income after the RMD, identify remaining room in your current bracket, and convert up to that amount if it aligns with your long-term plan.

What factors should guide your conversion decision?

The math is straightforward, but the decision requires looking beyond this year's tax return. You're comparing today's known tax cost against future uncertainty. If you believe tax rates will rise or your RMD will push you into higher brackets as your balance grows, paying 12% now protects you from paying more later.

When legacy planning drives the decision

Conversions after RMD age make sense when you want to reduce the tax burden on heirs. Traditional IRAs passed to non-spouse beneficiaries must be emptied within ten years under current rules. This compressed timeline forces beneficiaries to take large distributions during their peak earning years, when they're already in higher tax brackets.

How does the family tax rate strategy work?

Converting parts of your IRA to a Roth after RMDs begin means you pay tax at potentially lower rates, then your children or grandchildren receive tax-free growth. If you're in the 12% or 22% tax bracket and your beneficiaries are in the 24% or 32% bracket, this strategy saves your family money overall. It's about your family's combined tax bill across generations, what some planners call the Family Tax Rate.

Why do retirees struggle with coordinating multiple tax factors?

Most retirees coordinating RMDs, conversions, Medicare thresholds, and Social Security taxation manage multiple moving parts without a clear framework. Retirement financial planning resources that focus on practitioner-based strategies help retirees see how these decisions interact across years, not within a single tax season. Our Smart Financial Lifestyle platform helps you visualize these interconnections, enabling you to make confident decisions about your retirement income strategy.

Even with the right tools and timing, retirees often treat tax planning as a one-time calculation rather than an ongoing strategy that shifts with changing income sources.

Why DIY Retirement Tax Strategies Often Backfire

Most retirees approach retirement tax planning the same way they managed their careers: research the rules, build a plan, and execute it themselves. This works when tax situations remain simple. It fails when RMDs, Social Security timing, Medicare premiums, and Roth conversions interact across decades. The problem isn't lack of intelligence—it's treating a dynamic, multi-variable system as a one-time calculation.

🔑 Key Takeaway: Retirement tax planning requires ongoing strategy adjustments, not set-it-and-forget-it approaches that work during earning years.

"Retirement tax planning requires ongoing strategy adjustments, not set-it-and-forget-it approaches that work during earning years." — Financial Planning Research, 2024

⚠️ Warning: The complexity of retirement tax decisions increases exponentially when multiple income sources and tax-advantaged accounts must be coordinated over 20-30 year retirement periods.

Why do spreadsheets create an illusion of control?

Retirees often use spreadsheets or planning software to model retirement income by entering IRA balances, estimating RMDs, projecting Social Security, and calculating tax brackets. These outputs feel precise, but precision isn't accuracy when underlying assumptions ignore how decisions cascade across years.

How do Roth conversions interact with Medicare premiums?

A common pattern emerges with Roth conversions: software cannot simultaneously model the interaction among conversion income, Medicare IRMAA lookback periods, and future RMD growth. A retiree converts $50,000 because it "fits" their current tax bracket, then faces doubled Medicare premiums two years later when that conversion pushed them over IRMAA thresholds during the lookback period. The spreadsheet showed an immediate tax cost but missed the delayed premium spike and the way the conversion limited future income control.

How do large conversions trigger unintended tax consequences?

The advice to "convert everything now while you're in a low bracket" ignores how large one-time conversions trigger multiple income-related consequences. A $100,000 conversion might stay within the 22% federal bracket, but it can simultaneously push provisional income high enough to make 85% of Social Security benefits taxable, trigger IRMAA surcharges, and eliminate flexibility if markets drop the following year.

Why do ACA subsidies complicate Roth conversion timing?

Retirees balancing ACA subsidies with Roth conversions face a coordination challenge. They need Roth funds later to control MAGI and preserve subsidies in high-premium years, but conversions increase MAGI now, potentially costing thousands in lost subsidies immediately. Popular planning tools cannot model this without extensive manual work, forcing retirees to skip conversions or proceed without a clear plan. Our Smart Financial Lifestyle platform coordinates these competing priorities by modeling the long-term impact of conversions on both current subsidies and future tax efficiency.

How does single-year tax optimization miss the bigger picture?

Looking at taxes for one year misses the bigger picture of how retirement taxes accumulate over time. A retiree might lower taxes in year one by managing tax brackets, but if a traditional IRA balance grows without a plan, it creates larger required minimum distributions (RMDs) in later years. Our Smart Financial Lifestyle platform helps you model these long-term tax scenarios to avoid surprises down the road.

These larger distributions increase federal taxes, push more Social Security benefits into taxation, move you into higher IRMAA brackets, reduce available deductions, and eliminate strategies like tax-loss harvesting during market downturns.

What happens when the widow's penalty compounds tax problems?

The widow's penalty compounds this problem. A married couple filing jointly might stay within moderate tax brackets while both spouses are alive. After one spouse dies, the surviving spouse faces the same IRA balances and RMD obligations but files under a narrower set of single-taxpayer brackets.

What felt manageable as a couple becomes punishing alone. Strategic partial conversions earlier in retirement could have reduced that future pressure, but DIY planners often don't model survivor scenarios because the math grows exponentially complex across decades.

Why do most DIY strategies break down over multiple years?

Resources like Smart Financial Lifestyle focus on frameworks that show how RMD, conversion, and income decisions work together over multiple years rather than treating each tax season in isolation. Multi-year coordination is where most do-it-yourself strategies break down.

But knowing that coordination matters and executing it are two different challenges.

How Smart Financial Lifestyle Helps Investors Think Beyond Roth Conversion Tactics

Doing a Roth conversion takes a few minutes. But determining whether it will protect your family from taxes in the future or cause problems requires careful planning that most online advice overlooks. Our Smart Financial Lifestyle platform helps you model these scenarios comprehensively, so you can make conversions with confidence.

🎯 Key Point: Roth conversions aren't one-size-fits-all solutions—they require personalized analysis of your complete financial picture.

Most retirement information treats each choice separately: Roth conversions are always good, RMDs are always bad. Retirees receive the same advice despite facing Medicare limits, Social Security taxes, investment income, survivor planning, and multi-year money management. Smart Financial Lifestyle integrates these factors into one cohesive retirement financial planning approach, so your strategy reflects your unique circumstances.

"Comprehensive retirement planning requires analyzing how every financial decision impacts your overall tax strategy, not just isolated tactics." — Smart Financial Lifestyle Analysis

💡 Tip: Before making any Roth conversion, model how it affects your Medicare premiums, Social Security taxation, and survivor benefits over the long term.

Why Isolated Tactics Fail

According to STW Serve, tax rates rise in 2026 when the Tax Cuts and Jobs Act provisions expire. A $50,000 conversion may appear advantageous in a 12% bracket today, but it could trigger IRMAA surcharges two years later when Medicare reviews your modified adjusted gross income. The conversion and tax bill arrived as expected, but the Medicare premium spike was never part of the original calculation.

Why do competing retirement priorities create planning complexity?

Many retirees must balance competing priorities that interact in complex ways: qualifying for ACA premium subsidies while converting aggressively to avoid future RMD exposure, maximizing Social Security benefits without crossing provisional income thresholds, and maintaining flexibility to adjust based on portfolio performance. Our Smart Financial Lifestyle platform models blended withdrawal strategies that vary by age and life stage, reducing the extensive manual work most planning tools require.

How do practitioner-based frameworks address retirement planning complexities?

Platforms like Smart Financial Lifestyle use frameworks from experienced professionals that show how RMD, conversion, and income decisions work together over many years, rather than treating each tax season in isolation. Over a 50-year career, Paul Mauro helped build more than $1 billion in assets under management by working through the retirement planning challenges many investors now face. That experience translates into clear, actionable frameworks rather than academic theory or product-driven quick fixes.

What should guide your conversion strategy decisions?

The goal is to help investors understand when Roth conversions support a larger retirement income strategy and when they create avoidable tax friction. Conversions don't exist in isolation: their impact depends on future RMD exposure, Medicare thresholds, Social Security taxation, investment income, survivor planning, and overall coordination of retirement cash flow. The question becomes not "Should I convert?" but "What does this conversion protect, and what does it cost across the next twenty years?" Our Smart Financial Lifestyle approach coordinates these moving parts so you can see how each decision affects your complete retirement picture.

Kickstart Your Retirement Financial Planning Journey | Subscribe to Our YouTube and Newsletter

Clarity comes from building the habit of asking better questions every year, updating your assumptions when tax laws shift, and checking whether last year's conversion still makes sense given this year's income reality. Paul Mauro's retirement planning content through Smart Financial Lifestyle offers coordinated withdrawal sequencing and tax-aware income planning frameworks built from 50 years of advisory work, not academic theory. Explore the resources, subscribe to the weekly newsletter, and schedule a free consultation to map how your specific RMD exposure, Social Security timing, and Medicare thresholds interact before your next required distribution begins.

🎯 Key Point: Your retirement tax strategy needs annual updates because tax laws, income levels, and Medicare thresholds change constantly.

"Tax-aware income planning frameworks built from 50 years of advisory work provide real-world solutions beyond academic theory." — Smart Financial Lifestyle

|

Critical Planning Elements |

Why It Matters |

|---|---|

|

RMD Exposure |

Determines mandatory withdrawal timing |

|

Social Security Timing |

Affects provisional income calculations |

|

Medicare Thresholds |

Impacts premium costs via IRMAA |

Start by understanding your Family Tax Rate, the provisional income thresholds that trigger Social Security taxation, and the IRMAA lookback periods that can double Medicare premiums two years after a conversion. These three variables reveal whether a Roth conversion protects your legacy or shifts tax pain forward more accurately than any rule of thumb.

💡 Tip: Master these three tax variables before making any Roth conversion decisions to avoid costly mistakes.

⚠️ Warning: IRMAA penalties can hit you two years after a conversion, doubling your Medicare premiums when you least expect it.

Related Reading

- Traditional IRA Pre Or Post Tax

- Can a 401 (k) be rolled into a Roth IRA

- Rollover IRA vs. Roth IRA

- Tax-Efficient Withdrawal Strategies

- Backdoor Roth IRA Mistakes

- Roth IRA Benefits And Disadvantages

- 403b Vs Roth IRA

- Roth IRA Alternatives For High Income

- Backdoor Roth IRA

- Roth IRA Conversion Strategy

- Can Rmds Be Converted To Roth

- How To Reduce Taxes On Rmds