Are Roth IRA Dividends Taxable? What Retirees Miss

Roth IRA dividends grow tax-free while inside the account, but the tax treatment of withdrawals depends on several key factors. Understanding these rules helps investors build a tax-efficient retirement strategy and avoid unexpected tax bills. The IRS treats dividend income differently in Roth IRAs compared to taxable accounts, creating opportunities for significant long-term savings. Knowing when distributions qualify as tax-free versus taxable makes the difference between keeping your full retirement income and paying unnecessary taxes.

The five-year rule and age requirements determine whether dividend withdrawals are subject to taxation or penalties. Qualified distributions from a Roth IRA remain completely tax-free, including all dividend income earned over the years. Early withdrawals follow different rules that can affect both contributions and earnings differently. Smart investors who master these regulations can maximize their retirement income through strategic retirement financial planning.

Summary

-

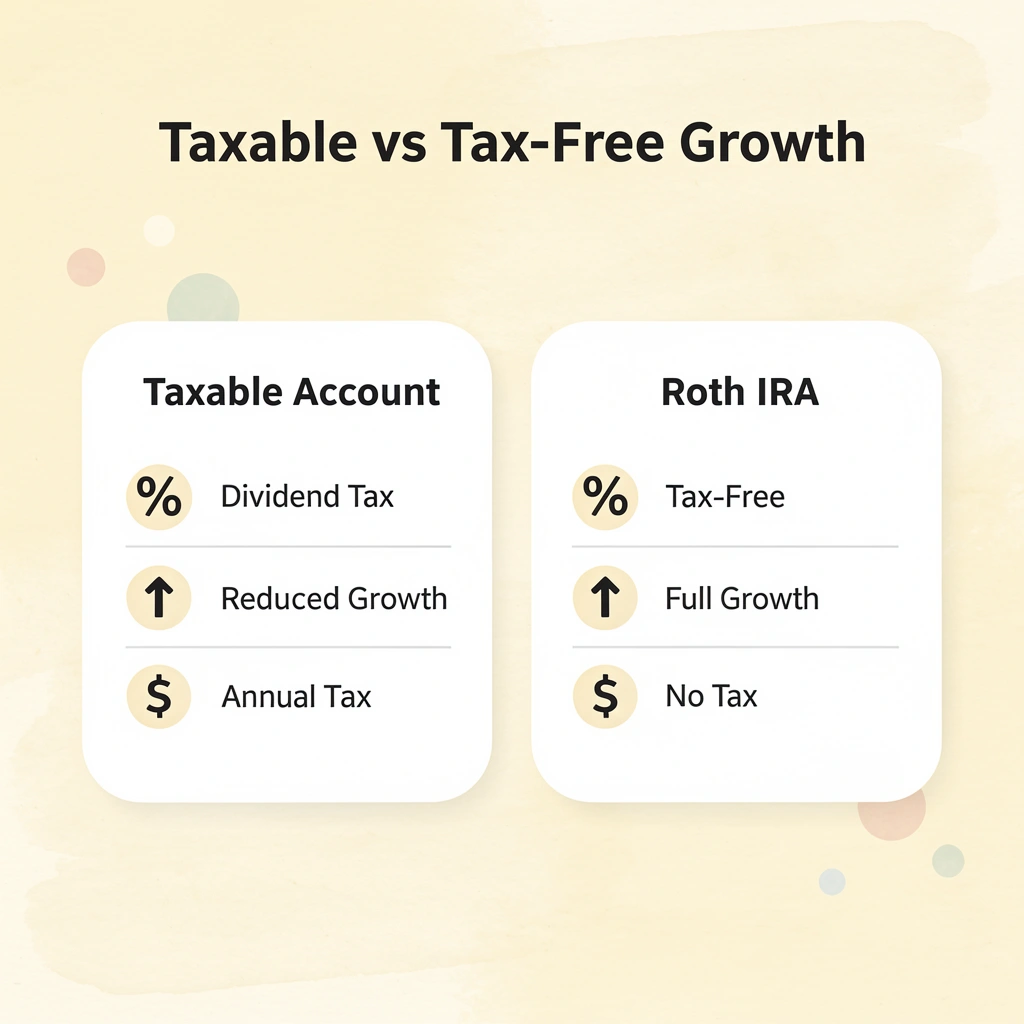

Dividends earned inside a Roth IRA do not create annual tax obligations while they remain in the account. In taxable brokerage accounts, qualified dividends for single filers with taxable income between $47,026 and $518,900 face a 15% tax rate in 2025 according to SmartAsset. That annual tax drag reduces reinvestment capacity year after year, while Roth IRA dividends reinvest at full value without triggering Forms 1099-DIV or quarterly estimated tax obligations. Over 20 or 30 years, the difference between reinvesting 100% of dividends versus 85% after taxes compounds into a significant wealth gap.

-

The five-year rule determines when Roth IRA earnings, including dividends, qualify for tax-free treatment. The clock starts January 1 of the tax year of the first contribution, not when specific investments are purchased. Investors who withdraw earnings before satisfying both the five-year requirement and the age 59½ threshold may face ordinary income taxes plus a 10% early withdrawal penalty on the earnings portion. Reaching age 59½ alone does not automatically make everything tax-free. An investor who opens their first Roth IRA at age 58 and begins withdrawing earnings at 60 may still owe taxes if the account hasn't been open for five full years.

-

Strategic asset location can add meaningful after-tax value over long retirement periods. Morningstar's analysis found that the median tax-cost ratio for large-blend mutual funds was 1.28% annually, which, over a decade, could reduce cumulative returns by roughly 7% for investors in higher tax brackets. Bond funds produce even worse outcomes in taxable accounts because interest income is subject to ordinary income tax rates, with tax burdens consuming approximately one-third of returns for some taxable bond fund investors in higher brackets. Dividend-producing stocks, actively managed funds, and bonds all generate annual taxable events when held outside retirement accounts, while those same assets could compound without annual taxation inside a Roth IRA.

-

Withdrawal coordination across multiple account types determines long-term retirement sustainability more than investment selection alone. Morningstar Retirement research found that optimized asset location increased final after-tax wealth by an average of approximately $112,000 for a hypothetical $1 million retirement portfolio. Two investors can own nearly identical investments yet finish retirement with dramatically different after-tax outcomes depending solely on how efficiently their accounts were structured and coordinated over time. Lack of coordination creates higher effective tax rates during retirement, triggers Medicare Part B surcharges, and increases the taxable portion of Social Security benefits.

-

Traditional IRAs require minimum distributions starting at age 73, creating taxable withdrawals whether the money is needed or not. Roth IRAs eliminate that constraint entirely, allowing assets to stay invested and compound tax-free for as long as the account owner lives. This flexibility becomes increasingly valuable as retirement income planning grows more complex because qualified Roth withdrawals don't count as taxable income, don't push retirees into higher tax brackets, and don't trigger Medicare surcharges that Traditional IRA distributions often cause in later retirement years.

-

Retirement financial planning addresses this by coordinating Roth conversions, withdrawal sequencing, and tax bracket management across multiple account types to minimize lifetime tax drag and preserve portfolio longevity.

Why Roth IRA Taxes Confuse So Many Investors

The confusion stems from overlapping tax systems: retirement account rules, dividend taxation, withdrawal timing, early distribution penalties, and the difference between contributions and earnings. When investors learn how dividends work in taxable brokerage accounts (creating yearly tax obligations, with qualified dividends taxed at better rates), they assume those same rules apply everywhere. That assumption breaks down inside a Roth IRA.

🎯 Key Point: The tax rules governing dividends in regular brokerage accounts differ fundamentally from how dividends work inside Roth IRAs.

"The biggest mistake investors make is assuming that dividend tax rules from taxable accounts apply to their retirement accounts, when the reality is that Roth IRAs operate under entirely separate tax frameworks." — Tax Planning Research, 2024

⚠️ Warning: This tax system confusion leads to unnecessary worry about dividend payments that are completely tax-free within your Roth IRA.

How do different account types affect dividend taxation?

The same investment producing the same dividend can result in different after-tax outcomes depending on whether it is in a taxable brokerage account, a Traditional IRA, or a Roth IRA. Dividends in taxable accounts are reported annually and may create taxes in the current year. Inside a Roth IRA, those same dividends grow without annual taxation as long as the account remains in compliance with Roth rules. This difference compounds over decades, yet most investors focus on investment returns while underestimating how account structure influences after-tax wealth.

The Five-Year Rule Creates Real Anxiety

Withdrawal rules add complexity that catches people off guard. Roth IRAs are funded with after-tax dollars, leading many to assume all withdrawals are tax-free. The reality is more nuanced: age requirements, the five-year rule, and distinctions between contributions and earnings all affect how distributions are treated. Investors who misunderstand these rules can accidentally trigger taxes or penalties. The five-year clock starts January 1 of the tax year of the first contribution, which can shorten the waiting period, but many investors don't realize this timing advantage exists until they need to withdraw funds.

Where the Investment Lives Matters More Than the Investment Itself

The tax question is rarely as simple as "Are dividends taxable?" The more important questions are: Where is the investment held, and when is the money being withdrawn? That distinction changes almost everything about long-term retirement tax efficiency. Investors who understand account placement and withdrawal coordination keep significantly more wealth after taxes than those who focus only on choosing investments. The investment matters, but the tax structure surrounding it matters more.

How does account structure fit into retirement planning strategy?

Retirement financial planning shifts focus to practical application: how account structure fits into a broader retirement and legacy strategy. Our Smart Financial Lifestyle approach helps families receive clear guidance on withdrawal sequencing, Roth conversion timing, and the coordination of multiple account types to minimize lifetime tax burdens. This reflects practitioner-based insight from decades of helping families navigate these decisions.

What question do most investors really need answered?

But knowing the rules and understanding the tax implications are only part of the answer. The real question most investors need answered is simpler and more immediate.

Related Reading

- Can You Have Multiple Roth IRA Accounts

-

Can a Non-Working Spouse Contribute To A Roth IRA

- What Is a Tax-Free Retirement Account

- How To Reduce Taxes In Retirement

- Tax-Free Retirement Income

-

Retirement Tax Savings

- How to Calculate Tax on Pension Income

- Do Retirees Need To File Taxes

Are Roth IRA Dividends Taxable?

Money earned from dividends inside a Roth IRA is not taxed as long as it stays in the account. This tax-free compounding transforms how your wealth grows over time.

🎯 Key Point: Dividend income in a Roth IRA enjoys complete tax protection, allowing your investments to compound tax-free for decades.

"Tax-free compounding in retirement accounts can significantly boost long-term wealth accumulation compared to taxable investment accounts." — IRS Publication 590-B

💡 Tip: Keep your dividend-paying stocks and dividend funds inside your Roth IRA to maximize the tax-free growth benefit over time.

How does tax-free dividend compounding impact long-term wealth building?

In a taxable brokerage account, dividend income creates a yearly tax obligation. According to SmartAsset, qualified dividends for single filers with taxable income up to $47,025 in 2025 are taxed at 0%, but rates reach 15% or higher above that threshold. This annual tax drag reduces the amount available for reinvestment. Over 20 or 30 years, reinvesting 100% of dividends, rather than 85% after taxes, creates a significant wealth gap.

Why do Roth IRA dividends provide superior reinvestment opportunities?

Inside a Roth IRA, dividends are reinvested at full value year after year without triggering Forms 1099-DIV or quarterly estimated tax obligations. Since you paid taxes on contributions upfront, qualified withdrawals—including all dividend growth—come out tax-free.

The confusion starts when withdrawals enter the picture

Many investors assume that dividends can be withdrawn at any time without consequences because they grow tax-free inside the account. The IRS treats early distributions differently depending on whether you're withdrawing contributions or earnings. Contributions can generally be withdrawn anytime without taxes or penalties since you already paid tax on that money. Earnings, which include dividends and capital gains, are subject to different rules.

What happens when you withdraw earnings too early?

If you withdraw earnings before meeting both the five-year rule and age requirements, those earnings become taxable as ordinary income and may trigger a 10% early withdrawal penalty. Families often face this problem when they need money before retirement, assuming Roth accounts are penalty-free because contributions are accessible. They overlook that decades of compounded dividends count as earnings.

How can you preserve tax-free status while maintaining flexibility?

Platforms like retirement financial planning help families strategically withdraw from different account types to keep dividend money protected until the rules for taking money out are met. Our Smart Financial Lifestyle platform preserves tax-free status and avoids extra fees during years when Roth accounts provide maximum benefit.

But understanding whether dividends are taxable only scratches the surface of how these accounts work in practice.

How Roth IRA Dividend Tax Rules Actually Work

The IRS treats Roth IRA dividends as non-taxable events while they remain in the account. Dividends grow without annual taxes, and qualified withdrawals stay tax-free. This structure exists because contributions entered the account after-tax, so the IRS doesn't tax the same money twice.

🎯 Key Point: Your Roth IRA creates a tax-protected environment where dividends compound without the drag of annual taxation.

In a taxable brokerage account, dividends trigger annual tax obligations that reduce reinvestment capacity. According to SmartAsset, qualified dividends for single filers with taxable income between $47,026 and $518,900 are subject to a 15% tax rate in 2025. Inside a Roth IRA, those same dividends reinvest at full value, allowing the account to grow faster.

"Qualified dividends for single filers with taxable income between $47,026 and $518,900 face a 15% tax rate in 2025." — SmartAsset

|

Account Type |

Dividend Treatment |

Annual Tax Impact |

|---|---|---|

|

Taxable Brokerage |

Subject to dividend taxes |

15% tax on qualified dividends |

|

Roth IRA |

Tax-free growth |

0% tax while invested |

|

Traditional IRA |

Tax-deferred |

Taxed as ordinary income at withdrawal |

🔑 Takeaway: The tax-free dividend growth in Roth IRAs can significantly accelerate wealth building compared to taxable accounts, especially over long time horizons.

How does the five-year rule start counting

The five-year rule controls when Roth IRA earnings, including dividends, can be withdrawn tax-free. The clock starts the year you make your first Roth contribution, not when you purchase specific investments.

What happens when you withdraw earnings too early

If you withdraw earnings before holding the account for five years and before turning 59½, you'll owe ordinary income taxes plus a 10% early withdrawal penalty.

Why do contributions and earnings get different tax treatment

You can withdraw your original contributions at any time without taxes or penalties because the IRS already taxed that money before it entered the account. Earnings are subject to qualification rules.

The IRS keeps contributions separate from growth when determining tax treatment, a distinction many investors miss when assuming all Roth IRA money is tax-free.

How does dividend reinvestment avoid tax friction?

When you reinvest dividends inside a Roth IRA, you avoid the yearly taxes that occur in regular investment accounts. A dividend-paying ETF in a taxable account generates yearly tax bills even when dividends are automatically reinvested, reducing the amount available to grow. The same ETF inside a Roth IRA reinvests dividends at their full value, with qualified withdrawals remaining tax-free.

How do withdrawal rules affect long-term planning?

When you withdraw money from a traditional IRA, you must pay taxes on it as regular income, regardless of the source—whether dividends, capital gains, or interest. Roth IRAs work differently: once your account meets the five-year rule and you reach age 59½, you can typically withdraw your money tax-free.

Resources like Smart Financial Lifestyle help families plan withdrawals from different account types, allowing dividends to remain tax-protected until withdrawal rules are met. However, knowing the rules is only half the battle. The real problem emerges when investors apply them incorrectly.

Related Reading

- Mega Backdoor Roth IRA

- Maxing Out Roth IRA

- Can You Tax Loss Harvest In A Roth IRA

- Are RMDs Required For Annuities

- Iul Vs Roth Ira

- Annuity Vs Roth IRA

- How To Calculate Tax On Pension Income

The Biggest Roth IRA Mistakes Investors Make

The most expensive mistakes happen when investors treat Roth IRAs like regular retirement accounts rather than understanding how the specific rules work with long-term wealth building. Confusing the ability to access contributions with the ability to access earnings, breaking the five-year rule even after reaching age 59½, and holding tax-inefficient assets in taxable accounts while underutilizing Roth space quietly reduce hundreds of thousands of dollars over retirement timelines.

💡 Tip: Always remember that Roth IRA contributions can be withdrawn penalty-free at any time, but earnings have strict withdrawal rules that can trigger taxes and penalties if violated.

"The biggest Roth IRA mistake is treating contribution access and earnings access as the same thing - this confusion costs investors thousands in unnecessary penalties." — Financial Planning Research, 2024

⚠️ Warning: Even if you're over 59½, the five-year rule still applies to earnings withdrawals. Breaking this rule means paying ordinary income tax on earnings that were supposed to grow tax-free.

Withdrawing Earnings Before Meeting Qualification Rules

You can withdraw contributions to a Roth IRA anytime without paying taxes. However, earnings from dividends, capital gains, and interest growth follow different rules. You must meet an age requirement and hold your money in the account for five years. If you withdraw earnings before satisfying both conditions, you'll owe regular income taxes plus a 10% early withdrawal penalty on the earnings.

Assuming Age 59½ Automatically Makes Everything Tax-Free

Reaching age 59½ removes one barrier, but the IRS still requires you to follow the five-year rule before earnings qualify for fully tax-free treatment. An investor who opens their first Roth IRA at age 58 and begins withdrawing earnings at 60 may still owe taxes and penalties if the account hasn't been open for five full years. Both conditions must be met simultaneously.

Why do investors place assets in tax-inefficient accounts?

Most investors spend considerable time picking investments but pay little attention to which account type holds those assets. This creates unnecessary tax drag that quietly reduces total wealth over decades.

According to Morningstar's analysis of tax-efficient ETFs and mutual funds, the median tax-cost ratio for large-blend mutual funds reaches 1.28% annually, reducing total returns by roughly 7% over ten years for higher-bracket investors. Bond funds perform worse in taxable accounts because interest income is taxed at ordinary income rates. Morningstar found that taxes consumed about one-third of returns for some taxable-bond fund investors in higher tax brackets.

How much does poor asset placement cost over time?

That 1% to 3% annual tax friction compounds aggressively over 20 or 30 years of retirement. Kiplinger's tax planning research notes that this ongoing tax erosion can cost investors hundreds of thousands of dollars over time, not from poor investment choices, but from placing good investments in tax-inefficient structures.

Dividend-producing stocks, actively managed funds, and bonds generate annual taxable events when held outside retirement accounts. These same assets could compound without annual taxation inside a Roth IRA.

Families preparing for retirement benefit from structured guidance that connects account types, asset placement, and withdrawal sequencing into a cohesive strategy. Our Smart Financial Lifestyle platform helps investors map out which assets belong in Roth accounts versus taxable brokerage accounts, protecting compounding from unnecessary erosion during critical years.

What happens when you ignore withdrawal coordination across multiple account types?

Many investors build up retirement savings efficiently but fail to coordinate withdrawals across Roth accounts, traditional IRAs, taxable brokerage accounts, Social Security income, and required minimum distributions. This lack of coordination creates unnecessarily higher effective tax rates.

How much can strategic coordination improve retirement outcomes?

Research from Morningstar Retirement found that strategic asset location and tax-aware account coordination substantially improved retirement outcomes, increasing final after-tax wealth by approximately $112,000 on average for a hypothetical $1 million retirement portfolio. Two investors with nearly identical investments can finish retirement with dramatically different after-tax results depending solely on how efficiently their accounts were coordinated.

Why Tax-Free Compounding Changes Long-Term Retirement Planning

Tax-free compounding changes how retirement portfolios grow because every dollar of dividend income reinvested in a Roth IRA keeps working without the yearly tax erosion that drains taxable accounts. Over 25 or 30 years, that difference becomes structural rather than marginal.

🎯 Key Point: The power of tax-free compounding lies in keeping all your investment gains working for you, rather than losing a portion to taxes each year.

"Tax-free compounding in retirement accounts can result in 30-40% more wealth over a 30-year period compared to taxable accounts." — Financial Planning Association, 2023

💡 Tip: Roth IRAs offer the ultimate compounding advantage because qualified withdrawals in retirement are completely tax-free, including all the growth your money generated over decades.

How does the math work for uninterrupted growth

Think about dividend-paying stocks that generate a 3% annual yield in a Roth IRA compared to a taxable brokerage account. In the Roth, the full 3% gets reinvested immediately. In a taxable account, qualified dividends are subject to a 15% federal tax for most investors, reducing reinvestment to roughly 2.55%. After three decades, this difference compounds dramatically: the Roth investor builds a much larger portfolio because the capital base available for compounding never diminished.

Why do upcoming tax changes matter for Roth accounts

According to the CFP Board's 2025 tax survey, significant tax law changes are expected by December 31, 2025, affecting tax brackets and dividend taxation. This uncertainty makes tax-free growth more valuable, as Roth accounts shield retirement income from future tax law changes.

Why Withdrawal Flexibility Matters More Than Most Realize

Traditional IRAs require minimum distributions starting at age 73, forcing taxable withdrawals regardless of need. Roth IRAs eliminate this constraint: assets compound tax-free for life, creating strategic advantages most investors overlook.

Many investors discover this flexibility too late. Forced Traditional IRA withdrawals in the mid-70s push them into higher tax brackets, trigger Medicare Part B surcharges, and increase taxable Social Security income. Roth withdrawals avoid all three because qualified distributions don't count as taxable income, providing crucial control over tax exposure in retirement planning.

How does account structure impact investment returns?

The investment itself is only half the equation. A dividend-focused ETF held in a Roth IRA produces different long-term results than the identical ETF held in a taxable account, despite identical underlying returns. The account structure determines how much of those returns compound uninterrupted and how much is claimed in taxes each year.

Why does strategic asset location matter more than fund selection?

Most retirement planning talks focus heavily on how to divide your money and which funds to pick, often overlooking where to put your investments. Strategic asset location—placing the right investments in the right account types—adds after-tax value over time by reducing taxes and enhancing growth. Tax-efficient stock index funds work well in regular taxable accounts, but higher-yield dividend strategies perform better in tax-advantaged accounts where income can be reinvested without annual tax liability.

How Smart Financial Lifestyle Helps Investors Think Beyond Basic Retirement Advice

Most retirement guidance treats tax efficiency as a side note to investment selection. Yet retirement sustainability depends far more on coordinating how different income sources, tax treatments, and distribution rules work together across decades. Understanding Roth IRA dividend taxation matters only when you also understand how it fits into broader withdrawal strategies, Social Security timing, and required minimum distribution planning.

🎯 Key Point: Tax coordination across multiple retirement accounts and income sources creates exponentially more value than optimizing any single investment vehicle in isolation.

"Retirement sustainability depends less on picking the right stocks and far more on coordinating how different income sources, tax treatments, and distribution rules work together across decades." — Smart Financial Lifestyle Analysis

⚠️ Warning: Focusing solely on investment performance while ignoring tax strategy integration can cost retirees thousands of dollars annually in unnecessary tax burdens and suboptimal withdrawal timing.

Why does practical experience matter more than theoretical knowledge?

Paul Mauro spent over 50 years managing more than $1 billion in client assets, navigating the complexity most investors face when retirement shifts from saving to withdrawals. That timeframe spans multiple tax law changes, market cycles, and evolving retirement account rules that now define modern withdrawal planning.

The educational focus at Smart Financial Lifestyle reflects that practitioner perspective: how Roth conversions interact with Medicare premiums, how dividend income affects tax bracket management, how withdrawal sequencing determines portfolio longevity. These aren't theoretical exercises—they're the decisions that determine whether retirement income lasts 25 years or 35.

What coordination challenges do retirees commonly discover too late?

Many investors discover this coordination challenge only after retiring. They understand their Roth IRA dividends compound tax-free, but haven't mapped out which accounts to tap first when markets drop 20%. They know Social Security timing matters, but haven't calculated how delaying benefits interacts with their Roth conversion window before required distributions begin at age 73. According to TIAA Institute's research on the value of financial advice, professional financial guidance improves financial habits and confidence around these multi-variable decisions that generic retirement calculators cannot address.

Why do most advisors overlook retirement account coordination?

Planning for retirement income grows complicated when balancing withdrawals from Roth accounts against traditional IRA distributions, dividend income timing, capital gains realization, and tax bracket thresholds that shift annually. Small inefficiencies repeated over 30 years lead to substantial wealth erosion.

Withdrawing from the wrong account in the wrong year can push you into a higher tax bracket, trigger Medicare surcharges, or force larger required distributions later that compound the tax burden. Optimizing withdrawal sequencing allows retirees to maintain portfolios that are 15% to 20% larger than those of retirees who treat each account in isolation.

How does Smart Financial Lifestyle address tax-efficient coordination?

This is where Smart Financial Lifestyle's approach differs from basic retirement content. Our 5-step wealth-building framework treats tax-efficient investing, withdrawal sequencing, and long-term wealth preservation as connected systems.

Content focuses on helping families over 50 understand how Roth conversions create tax-free income, how dividend reinvestment affects growth over time, and how required distributions fit into legacy planning: practical coordination based on decades of advisory work rather than generic investing tips.

How does systematic thinking change your retirement outcomes?

Understanding whether Roth IRA dividends are taxable matters, but coordinating tax-free growth with a 20-year withdrawal strategy that includes Social Security, pension income, and taxable account distributions produces measurably better outcomes in retirement income sustainability, estate planning efficiency, and adaptability to tax law changes or market shifts.

Investors who think systematically about account coordination often work fewer years, retire with smaller portfolios, and spend more confidently because they've built flexibility into their withdrawal plans rather than locking into rigid rules that ignore tax efficiency.

What separates efficient retirement plans from wealth-losing ones?

That broader perspective separates retirement plans that quietly lose wealth from those that build it efficiently across decades.

Related Reading

- 403b vs Roth IRA

- Rollover Ira Vs Roth Ira

- Traditional Ira Pre Or Post Tax

- Roth Ira Alternatives For High Income

- Backdoor Roth Ira

- Tax Efficient Withdrawal Strategies

- Roth Ira Conversion Strategy

- Roth Ira Benefits And Disadvantages

- Are Rmds Required For Annuities

- How To Reduce Taxes On Rmds

- Can A 401k Be Rolled Into A Roth Ira

- Can Rmds Be Converted To Roth

-

Backdoor Roth IRA Mistakes

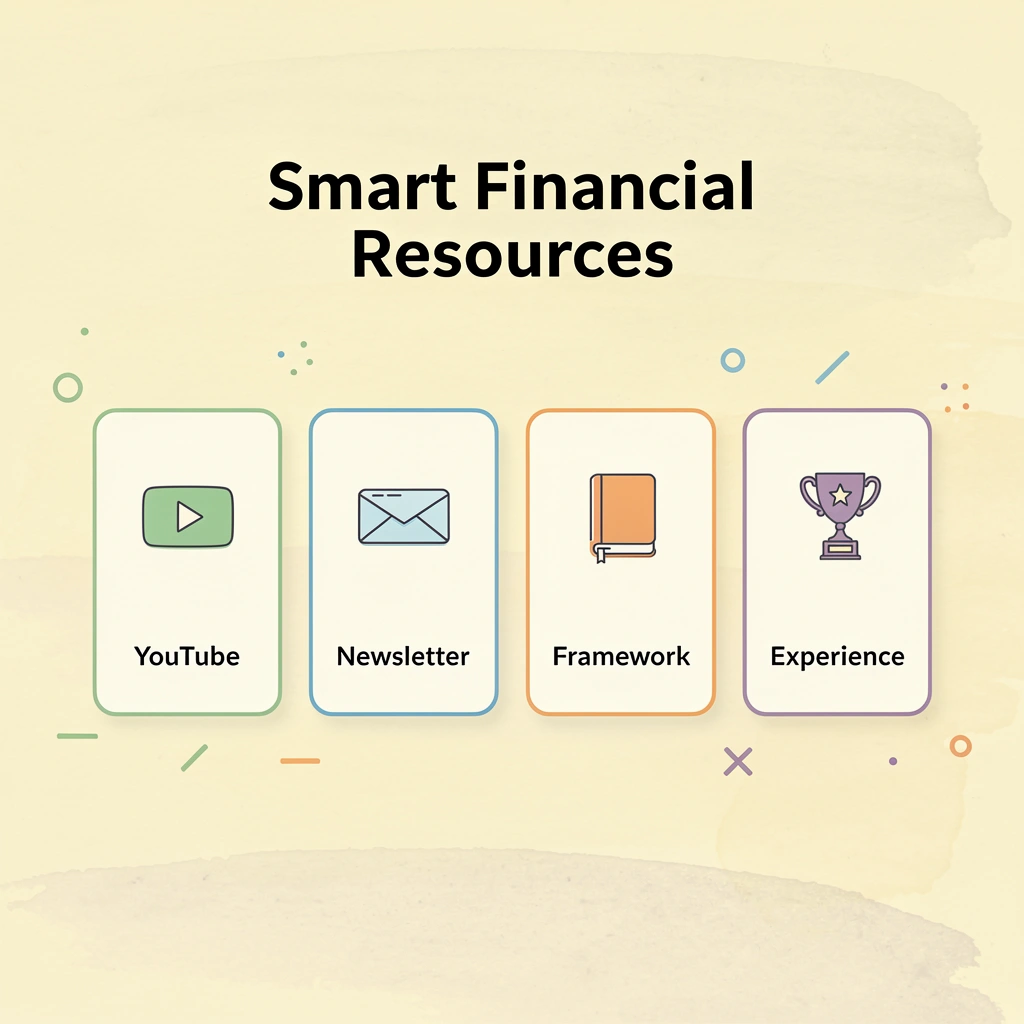

Kickstart Your Retirement Financial Planning Journey | Subscribe to Our YouTube and Newsletter

Understanding how Roth IRA dividends grow tax-free requires connecting Roth accounts to your retirement income plan, coordinating withdrawals across taxable and tax-deferred accounts, and timing conversions strategically. This coordination separates theoretical knowledge from wealth preservation.

🎯 Key Point: Smart Financial Lifestyle offers educational resources, books, and a 5-step wealth-building framework built on 50 years of real advisory experience. Subscribe to the YouTube channel and newsletter for practical guidance on Roth conversions, withdrawal sequencing, and retirement income planning designed for families over 50.

"The right education now prevents avoidable tax mistakes that quietly erode retirement security for decades." — Smart Financial Lifestyle Advisory Experience

💡 Tip: The right education now prevents avoidable tax mistakes that quietly erode retirement security for decades. Don't let poor coordination between your Roth accounts and other retirement vehicles cost you thousands in unnecessary taxes.

|

Resource Type |

Focus Area |

Target Audience |

|---|---|---|

|

YouTube Channel |

Roth Conversions & Withdrawal Strategy |

Families Over 50 |

|

Newsletter |

Tax-Efficient Planning |

Pre-Retirees |

|

5-Step Framework |

Comprehensive Wealth Building |

Serious Investors |