For far too long, financial advice has been served up as a one-size-fits-all solution. But that’s like giving everyone the same map, regardless of their destination. When it comes to financial planning, women are often navigating a much different journey—one with unique challenges and opportunities that the standard advice just doesn't cover.

This isn’t about better or worse; it’s about acknowledging a different reality. Creating a financial strategy that recognizes this isn't just smart—it's essential for building real, lasting financial independence.

Why Your Financial Journey Needs a Different Map

Think of it like planning a road trip. If you're just driving from point A to point B on a straight highway, a basic map works just fine. But what if your trip is longer, has a few important detours, and maybe a few extra hills to climb? You’d want a much more detailed and strategic map for that, right? That’s the reality for so many women.

The old-school financial model often glosses over the specific variables that shape a woman's financial life. Recognizing these differences isn’t a sign of weakness—it's the first and most powerful step you can take toward building a stronger, more resilient financial future.

To get a clearer picture, let's break down the key societal and economic factors that make a tailored financial plan for women so critical.

Unique Financial Factors for Women at a Glance

| Factor | Impact on Financial Planning | Strategic Consideration |

|---|---|---|

| Longer Life Expectancy | Retirement savings must last for more years, often 5 to 7 years longer on average. | Prioritize long-term growth and create a plan that accounts for increased healthcare costs later in life. |

| Gender Pay Gap | Lower lifetime earnings directly translate to smaller savings, retirement contributions, and Social Security benefits. | Develop an aggressive savings and investment strategy to close the gap over time. Negotiate salaries effectively. |

| Career Interruptions | Time off for caregiving can halt savings momentum and slow down career and income progression. | Plan for these breaks by building robust savings, exploring spousal IRAs, and having a strategy to re-enter the workforce. |

| Greater Risk Aversion | Women sometimes invest more conservatively, which can lead to lower long-term returns and missing out on growth. | Build financial literacy and confidence to embrace a well-diversified, growth-oriented investment portfolio. |

Each of these factors, on its own, would be enough to justify a different approach. When you combine them, it becomes clear that a standard plan just won’t cut it.

The Real-World Impact

These aren’t just abstract statistics; they are real circumstances that directly impact savings, investments, and retirement security.

- Living Longer: Women, on average, live about five years longer than men. That’s five more years of expenses that your retirement nest egg needs to cover, making long-term growth absolutely crucial.

- The Pay Gap: Despite all the progress, the wage gap persists. Over a 40-year career, this can add up to hundreds of thousands of dollars in lost earnings, which means less money for saving and investing.

- Caregiving Detours: Women are still far more likely to step out of the workforce to care for children or aging parents. These breaks can disrupt career momentum, reduce lifetime earnings, and put a pause on crucial retirement contributions.

Acknowledging these realities is the most empowering step you can take. Your financial plan shouldn't ignore your life's unique contours; it should be built around them, turning potential challenges into strategic advantages.

This unique landscape highlights a growing need for advisors who actually get it. Yet, a significant gap remains. Women make up only 24% of Certified Financial Planner (CFP) professionals in the United States, even as their control over wealth grows.

This is especially noteworthy when you consider that women are on track to control 60% of the UK's wealth in the near future, showing a clear demand for more representative financial guidance. You can learn more about advancing women in financial planning from CFP Board.

By understanding this context, you can start building a financial plan that is not just effective, but also deeply aligned with your personal journey.

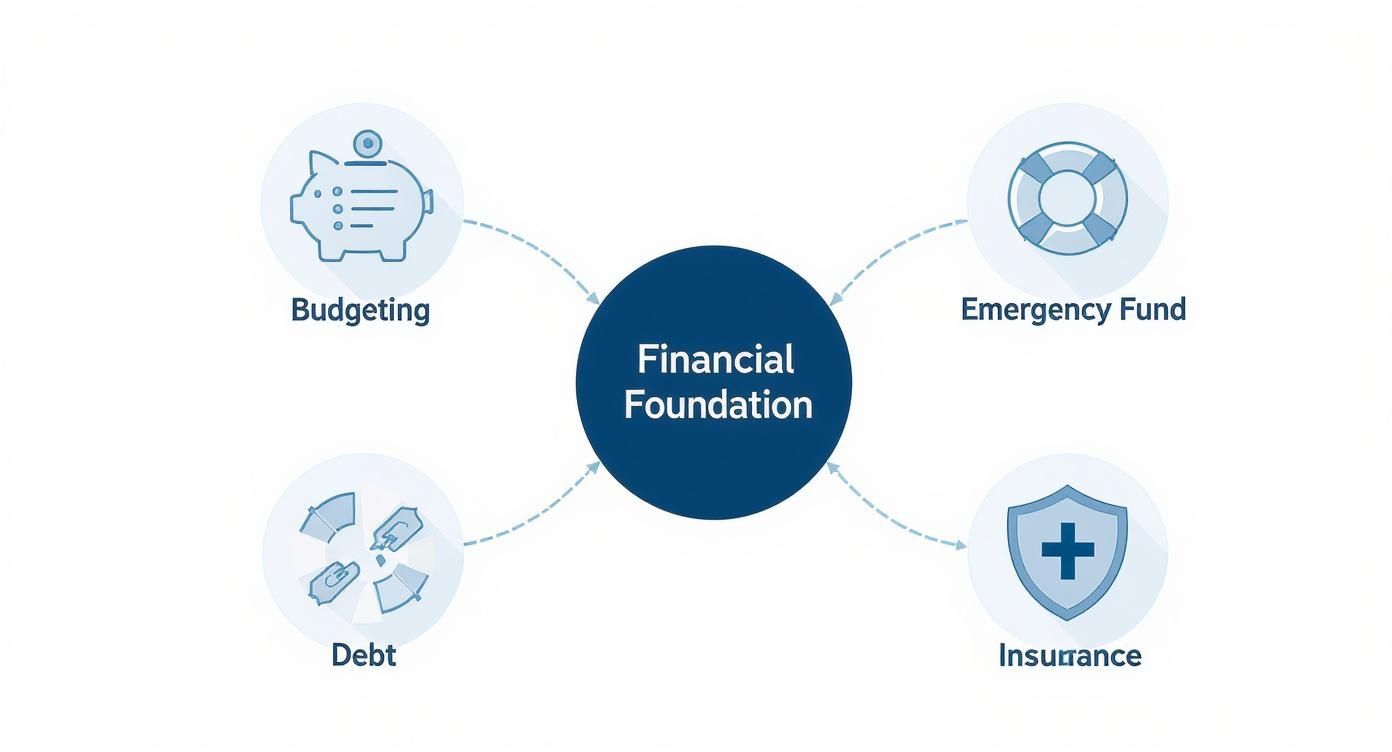

Building Your Core Financial Foundation

A strong financial future is built just like a house—one solid layer at a time, starting with a powerful foundation. Without this base, any attempts to grow wealth later on will be shaky at best. This is where we move from theory to action, breaking down the essential pillars of your financial security into clear, manageable steps that give you control and confidence.

Getting started often feels like the hardest part, but it’s also the most empowering. I’ve seen firsthand how many women feel anxious about money conversations, which can create a real barrier to taking that first step. It’s not just a feeling; a significant confidence gap persists, particularly among younger generations. A recent survey revealed that only 38% of Gen Z and Millennial women felt confident discussing money, compared to 56% of men in the same age groups. This isn't a personal failing; it's a systemic issue, but one you can absolutely overcome by taking small, deliberate actions. You can read more about the findings on women's financial confidence from PlanAdviser.

Reframe Your Budget as a Spending Plan

The word "budget" often brings to mind restriction and sacrifice, like a strict diet that’s no fun to follow. Let's throw that idea out.

Instead, think of it as a spending plan—a proactive tool designed to align your money with what you truly value. A spending plan isn’t about cutting out everything you love. It’s about making conscious choices. It answers the question, "Where is my money going, and is it making me happy?" By tracking your income and expenses, you gain incredible clarity and can start directing your resources toward your goals, whether that’s traveling the world, starting a business, or simply achieving peace of mind.

Expert Insight: "Your spending plan is your personal roadmap. It’s not about restriction; it's about direction. It ensures you’re using your money to build the life you actually want, not just the one that happens by default."

Build Your Financial Safety Net

Life is messy. A car breaks down, a medical bill shows up out of nowhere, or a job situation changes unexpectedly. An emergency fund is your financial safety net, designed to catch you when these things happen without forcing you to rack up high-interest debt.

This is a non-negotiable part of financial planning for women, providing a crucial buffer against instability. The standard advice is to save three to six months' worth of essential living expenses. That might sound like a huge number, but you don't have to get there overnight. Start small. Set up an automatic transfer of just $25 or $50 a week into a separate high-yield savings account. The key is to start building momentum. For a detailed guide, check out our Emergency Fund Checklist with 8 must-have steps for true financial resilience.

Create a Smart Debt Management Strategy

Not all debt is created equal. But high-interest debt—especially from credit cards—can be a major drain on your ability to build wealth. It’s like trying to fill a bucket with a hole in the bottom; your money leaks out in interest payments before you can use it for anything else.

Tackling this debt requires a clear strategy. Two of the most popular methods are:

- The Avalanche Method: You focus on paying off the debt with the highest interest rate first while making minimum payments on everything else. This approach saves you the most money in interest over time.

- The Snowball Method: Here, you focus on paying off the smallest debt balance first, regardless of the interest rate. This method provides quick psychological wins that build momentum and keep you motivated.

Choose the method that works for your personality. The goal is simple: systematically eliminate the debt that costs you the most, freeing up your cash flow for saving and investing.

Protect Your Foundation with Insurance

Finally, think of insurance as the protective shield around your financial foundation. It’s the one piece you hope you never have to use, but its presence protects everything you’ve worked so hard to build from a catastrophic event.

Key types of insurance act as safeguards for different areas of your life:

- Health Insurance: Protects you from devastating medical bills.

- Disability Insurance: Replaces a portion of your income if you become unable to work due to illness or injury—a critical and often overlooked protection.

- Life Insurance: Provides for your dependents if you pass away.

- Auto and Homeowners/Renters Insurance: Protects your major assets.

Reviewing your coverage annually is a vital part of sound financial planning. By putting these foundational pillars in place, you create a secure base from which you can confidently begin to grow your wealth for the long term.

How to Start Investing and Grow Your Wealth

Once your financial foundation is solid—with a budget, emergency fund, and debt plan in place—it’s time to shift your focus. You’ve done the hard work of saving money; now it's time to put that money to work for you. This is where investing comes in, and while it might feel intimidating at first, it's the single most powerful tool you have for building real, long-term wealth.

Think of it this way: saving is like putting water in a bucket. It's safe and predictable, but it just sits there. Investing is like planting a seed. With a little time and care, that small seed can grow into a massive tree, creating a cycle of growth that can last a lifetime. That's the magic of compound interest—the engine that will drive your wealth forward.

The Snowball Effect of Compound Interest

Compound interest is your best friend in finance. It’s the process of your money making money for you.

Picture a small snowball at the top of a very long hill. As you give it a little push, it starts rolling, picking up more snow. As it gets bigger, it picks up even more snow, accelerating faster and faster. That’s exactly how compounding works with your investments. The returns you earn start earning their own returns, creating a powerful growth cycle that builds on itself over time.

This concept is absolutely vital for women. Given our longer life expectancies, our money simply needs to last longer. Starting to invest, even with small amounts, gets that compounding snowball rolling early, giving it decades to grow into a substantial nest egg for your future.

The infographic below shows how all the foundational pieces fit together before you can start investing with confidence.

This visual reminds us that budgeting, managing debt, building an emergency fund, and having the right insurance are all interconnected pillars. They support your ability to invest with confidence and build for the long term.

Overcoming the Investing Confidence Gap

Historically, many women have felt hesitant about investing, but that trend is changing—fast. Research shows a remarkable rise in financial confidence and asset ownership among women. Still, there’s a lot of ground to cover. Globally, an estimated 53% of assets controlled by women are unmanaged, sitting on the sidelines, compared to 45% of assets controlled by men.

But the momentum is building, especially among younger generations. For instance, millennial women in Europe saw their financial confidence soar from 45% to 67% between 2018 and 2023. You can explore more about the rise of the female investor from McKinsey's research to see just how much this landscape is shifting.

The best way to build your own momentum? Start small. You don’t need a huge lump sum to get started. Many platforms today let you begin with as little as $50. The key is just to take that first step and turn investing into a regular habit.

Your Financial Toolkit: Different Investment Types

Think of different investments as tools in a financial toolbox, each designed for a specific job. Understanding the basics will help you build a strong portfolio that works for you.

- Stocks: Buying a stock means you own a tiny piece, or a share, of a public company. This is your growth tool. Stocks offer the highest potential for long-term returns, but they also come with higher risk as the company's value goes up and down.

- Bonds: When you buy a bond, you're essentially loaning money to a government or a corporation. This is your stability tool. Bonds generally offer lower but more predictable returns than stocks, acting as a steadying force in your portfolio.

- ETFs (Exchange-Traded Funds): ETFs are like a basket containing a mix of many different investments—sometimes hundreds of stocks or bonds all at once. They're a fantastic tool for beginners because they provide instant diversification, which means spreading your money across various assets to lower your risk.

Building a diversified portfolio is like preparing a balanced meal. You wouldn't just eat one type of food, right? In the same way, you shouldn't put all your money into a single investment. A healthy mix of stocks, bonds, and other assets helps protect you from the market's inevitable ups and downs.

To make these options clearer, let's break them down.

Common Investment Options Explained

Here’s a simple table comparing some of the most common investment vehicles. This can help you understand where each one fits into a broader strategy.

| Investment Type | What It Is | Typical Risk Level | Best For |

|---|---|---|---|

| Stocks | A share of ownership in a single public company (e.g., Apple, Amazon). | High | Long-term growth potential, for those comfortable with volatility. |

| Bonds | A loan you make to a government or corporation in exchange for interest payments. | Low to Medium | Generating steady income and providing stability to a portfolio. |

| Mutual Funds | A professionally managed fund that pools money to buy a diverse mix of stocks, bonds, or other assets. | Medium | Hands-off diversification without having to pick individual investments. |

| ETFs | A basket of assets (like stocks or bonds) that trades on an exchange, similar to a stock. | Varies (Low to High) | Low-cost, instant diversification that’s easy to buy and sell. |

| Real Estate | Physical property or funds that invest in property (REITs). | Medium to High | Generating rental income and potential long-term appreciation. |

Understanding these basic tools is the first step. You don't need to be an expert in all of them, but knowing what they are and what they do is empowering.

A great way to get started is by opening an account with a low-cost brokerage and investing in a broad-market ETF. This simple strategy allows you to own a small piece of the entire market without the pressure of picking individual winners. It's a single, powerful step that officially moves you from being a saver to an investor, putting your money to work for your future.

Planning for Retirement and Major Life Goals

Investing is the engine that grows your wealth, but that growth needs a destination. For most women I talk to, the big goals are a secure retirement and the freedom to chase other dreams, like buying a home or finally launching that business idea.

Because women often live longer and might have gaps in their earnings from taking on caregiving roles, our retirement planning has to be especially robust. We're not just saving for an endpoint; we're funding a whole new chapter of life that could last for decades.

On average, women live about five to seven years longer than men. That’s a simple fact with huge financial implications—it means our retirement savings just have to stretch further. This reality makes starting early and being strategic an absolute must.

Understanding Your Retirement Toolkit

The main tools you'll use for this journey are retirement accounts, which come with powerful tax advantages to help your money grow more efficiently. Think of them as different types of luggage for your financial trip; each one has a specific purpose.

- 401(k) or 403(b) Plans: These are the plans you get through work. You contribute pre-tax, which lowers your taxable income right now. The best part? Many employers offer a "match." This is free money they add to your account when you contribute, and it's a benefit you should never, ever leave on the table.

- Traditional IRA (Individual Retirement Account): Anyone with earned income can open one. Your contributions might be tax-deductible, and your investments grow tax-deferred until you pull the money out in retirement.

- Roth IRA: With a Roth, you contribute with after-tax dollars, so there's no immediate tax break. But here’s the magic: your investments grow completely tax-free, and every qualified dollar you withdraw in retirement is also tax-free. This can be a massive advantage down the road.

Using a combination of these accounts is often the smartest strategy. You don't have to pick just one!

Strategies for a Longer, Secure Retirement

Planning for a longer life means building a nest egg that can handle inflation, unexpected healthcare costs, and the simple test of time. For many, Social Security is a big piece of the retirement income puzzle. But the amount you get can vary wildly based on your work history and, most importantly, when you decide to start taking it.

Crafting a smart claiming strategy is vital. To dig deeper into this, check out our guide on how to maximize Social security benefits.

Beyond Social Security, your personal savings will do the heavy lifting. If you've taken time off from your career for caregiving, it’s easy to feel like you're playing catch-up. But there are powerful ways to close that gap.

Paul Mauro's Actionable Insight: "If you are over 50, the government allows for 'catch-up contributions.' This lets you save thousands of extra dollars per year in your 401(k) and IRA above the standard limits. It’s one of the most effective tools available to supercharge your savings later in your career."

Planning for Other Major Life Milestones

Your financial plan isn't just about retirement. It's the roadmap for all the big moments you want in your life. Whether that’s buying your first home, helping with a child's education, or launching that passion project, the principles are the same.

- Define the Goal Clearly: What do you want to achieve, and what’s a realistic cost?

- Set a Timeline: When do you want this to happen? Is this a five-year goal or a twenty-year plan?

- Create a Dedicated Savings Plan: Open a separate savings account for each goal. Automating your contributions is the key to consistency.

- Choose the Right Account: For shorter-term goals (under five years), a high-yield savings account is a safe bet. For longer-term dreams, you might consider investing in a balanced portfolio to give your money a better chance to grow.

By creating a real roadmap with clear checkpoints, you turn vague dreams into goals you can actually hit. It's how you stop just preparing for the future and start actively building the life you truly want.

Managing Your Finances Through Life's Transitions

Life is rarely a straight line. It's really a series of seasons, each with its own joys, challenges, and financial realities. The moments of greatest change—getting married, starting a family, shifting careers, or navigating a loss—are often the times when having a clear financial plan becomes most critical.

These transitions aren't just emotional events; they are significant financial events that demand your attention.

Navigating these shifts with intention is a core part of financial planning for women. It’s about building a plan that’s flexible enough to adapt with you, ensuring you maintain your financial independence and security no matter what comes your way. Each new chapter requires a fresh look at your financial map to make sure you're still heading in the right direction.

Navigating Joyful Milestones

Positive changes, like marriage or a career leap, are exciting, but they definitely bring a new layer of financial complexity. Proactive planning helps you merge lives and goals smoothly, setting you both up for shared success.

Getting Married

Joining your life with a partner also means joining your financial worlds. This is a great time to build a foundation of open, honest communication about money. It’s everything.

- Have the Money Talk: Get it all out on the table. Talk about your financial histories, debts, assets, and what you both want for the future.

- Decide How to Merge Finances: Will you have joint accounts, separate accounts, or a hybrid of both? There's no single right answer, only what works for your partnership.

- Update Your Documents: This is a big one. Review beneficiaries on all your accounts (retirement, life insurance) and update your estate planning documents like wills.

Motherhood and Caregiving

Welcoming a child or taking on a caregiving role for a parent are profound life changes with significant financial impacts. Planning for new costs, from childcare to potential income adjustments, is crucial. This is the time to reassess your budget, review your life and disability insurance coverage, and start or boost contributions to college savings plans if that’s part of your plan.

A financial plan that doesn't account for life's transitions is like a ship built for a calm harbor—it's unprepared for the open sea. Your plan must be dynamic, ready to adjust to both the expected and unexpected turns in your journey.

Managing Difficult Transitions

Difficult life changes like divorce or widowhood are emotionally draining, and the financial side can feel completely overwhelming. Taking small, deliberate steps can help you regain a sense of control and build a new foundation for your future. These are the moments when financial independence truly shows its importance.

Divorce or Separation

Untangling shared finances requires patience and precision. Your goal is to emerge with a crystal-clear understanding of your new financial reality.

- Gather All Financial Documents: Collect statements for all assets and debts, tax returns, and insurance policies. You need the full picture.

- Create a New Personal Budget: Get a handle on your individual income and expenses to plan for your post-divorce life.

- Update Everything: Change beneficiaries, retitle assets, close joint accounts, and establish your own credit. This is your fresh start.

Widowhood

Losing a spouse is a devastating experience. While it's vital to give yourself time to grieve, there are a few financial steps that shouldn't be delayed for too long.

- Locate Important Documents: Find the will, life insurance policies, and all account information.

- Notify Key Institutions: Contact Social Security, financial institutions, and your spouse’s former employer about any pension or retirement benefits.

- Avoid Hasty Decisions: Give yourself time before making any major, irreversible financial choices, like selling your home or making large investments. This is not the time for rash moves.

In every transition, knowledge and preparation are your greatest allies. By addressing the financial implications of life’s biggest moments head-on, you ensure that you remain in the driver's seat of your own financial destiny, empowered to build a secure future on your own terms.

Building Your Legacy with Estate Planning

Let's be honest, "estate planning" can sound stuffy and a bit morbid. It's often pictured as something only for the super-wealthy or for those in their golden years. But that view misses the mark completely.

Good estate planning isn’t really about the end of life. It’s about taking control of your legacy and providing one last, powerful act of care for the people you love.

Think of it as the ultimate "life instruction manual." It's your clear, thoughtful guide that makes sure your wishes are honored, your assets are protected, and an incredibly difficult time is made just a little bit easier for your family. This is the final, crucial piece of the financial puzzle, giving you the last word on everything you’ve worked so hard to build.

The Core Components of Your Plan

Your estate plan is really just a collection of a few key legal documents that all work together to carry out your instructions. Getting familiar with them is the first step toward building your legacy with confidence.

Here are the main players:

- A Will: This is the foundational document. It spells out how you want your assets to be handed out and lets you name a guardian for any minor children—an absolutely non-negotiable step for any mother.

- Trusts: A trust is a more advanced tool that can give you much greater control over how and when your assets are distributed. Trusts are great for avoiding the long and very public probate process, protecting assets for your beneficiaries, and in some cases, even trimming down estate taxes. If you want to go deeper, our guide on what a trust fund is and how it works is a fantastic starting point.

- Healthcare Directives: You might know this as a living will. This document outlines your wishes for medical treatment if you ever get to a point where you can't communicate them yourself.

Bringing Your Legacy to Life

Once you understand the tools, the next step is making the important decisions. This means choosing the right people to carry out your wishes.

You'll need to name an executor for your will and a trustee for any trusts you create. These are the people you are entrusting to manage your affairs responsibly when you're no longer here. Pick them carefully.

Your estate plan is your voice when you can no longer speak for yourself. It’s a profound expression of your values, ensuring your financial story concludes on your own terms and continues to support the people and causes you cherish.

Many women I work with also choose to extend their impact through charitable giving, weaving a favorite non-profit right into their estate plan. This is such a powerful way to support a cause you're passionate about, creating a legacy of generosity that can last for generations.

Finally, and this is important, your estate plan is not a "set it and forget it" task. Life happens. You need to review and update it after any major life event—getting married, a divorce, the birth of a child, or a big change in your financial picture. This keeps your plan current and ensures it always reflects your life and your wishes.

Common Questions About Financial Planning for Women

Navigating the world of personal finance always brings up questions, and that's a good thing. It's especially true when you're trying to build a plan that fits the real-world complexities of your life. Let's tackle some of the most common questions I hear from women, with direct answers to help you move forward with confidence.

These concerns are completely normal. The fact that you're asking them means you're already thinking like a savvy planner. Getting clear answers is how you build momentum and create lasting financial security.

How Can I Start Investing With a Small Amount of Money?

So many women hold back from investing because they think they need a huge pile of cash just to get in the game. This is one of the biggest myths out there. The truth is, you can start your investing journey today with as little as $50 or $100.

It’s all about finding the right entry point.

- Micro-investing apps: These are designed to let you invest small, regular amounts. Many even let you round up your daily purchases and invest the spare change automatically.

- Fractional shares: Gone are the days when you had to buy a full, expensive share of a company. Most brokerages now let you buy a piece of a stock, so you can own a slice of a major company without a massive upfront investment.

Honestly, the most important step is just to start. Consistency, powered by the magic of compound interest, will make even those small, regular investments grow into something significant over time. It’s about building the habit, not starting with a fortune.

What Is the Best Way to Catch Up on Retirement Savings After a Career Break?

Taking time out of the workforce for caregiving or other life events can create a gap in your savings. I see it all the time. But catching up is absolutely possible with a focused strategy. You're not "behind"—you're just starting from where you are today.

A smart "catch-up" plan isn't about frantically making up for lost time. It's about maximizing the time you have right now. With focus and the right tools, you can absolutely build a secure retirement, no matter what your career path has looked like.

Here's a three-step approach to put your savings on the fast track:

- Maximize Your Employer's Match: If your job offers a 401(k) match, contribute enough to get every single penny of it. Think of it as a 100% return on your money right out of the gate. It's the fastest way to give your savings a serious boost.

- Use Catch-Up Contributions: The IRS gives you a helping hand once you're age 50 or older. You're allowed to contribute thousands more to your 401(k) and IRA each year. Take advantage of it!

- Automate Your Savings: Set up automatic transfers from your paycheck directly into your retirement accounts. This classic "pay yourself first" method builds consistency without you even having to think about it.

Should I Pay Off Debt or Invest My Extra Money?

This is the classic financial tug-of-war, and the right answer really comes down to the interest rate on your debt. A good rule of thumb is to compare your debt's interest rate to the potential return you could earn from investing, which has historically averaged around 7-10% a year.

- Prioritize High-Interest Debt: If you're carrying debt with an interest rate above 7%—think credit cards, which often have rates of 20% or more—paying it down should be your number one priority. Wiping out that debt is a guaranteed, risk-free return on your money.

- Consider Investing with Low-Interest Debt: For debt with lower interest rates, like a mortgage or federal student loans below 6%, it often makes more mathematical sense to pay the minimum and invest your extra cash. The returns you could earn in the market are likely to outpace the interest you're paying on the loan.

By weighing these two sides, you can make a calculated decision that puts your money to work in the smartest way possible.

At Smart Financial Lifestyle, our commitment is to provide the clarity you need to build the secure future you deserve. When you're ready to take the next step, explore our resources and let us help you on your journey.