How to Create Multiple Income Streams

So, what does it actually take to create multiple income streams? It starts with taking a hard look at your unique skills and resources, figuring out a good mix of active, passive, and portfolio income options, and then mapping out a realistic plan to get them off the ground. The whole point is to diversify how you earn, breaking free from that total reliance on a single paycheck to build real financial strength.

Why Bother With Multiple Income Streams?

This idea of building wealth from different sources isn't just some trendy financial goal anymore; it's become a cornerstone of modern financial security. Relying on one salary in today's economy is like trying to balance on a one-legged stool—it might feel stable for a moment, but it's incredibly vulnerable.

For family stewards, retirees, and anyone navigating a big career transition, diversifying your income is no longer a luxury. It’s a flat-out necessity.

And this isn't just a hunch; the numbers back it up. By 2025, it’s expected that over 50% of Americans will have more than one source of income. This isn't happening by accident. It's a direct response to the cost of living climbing faster than wages, giving people a powerful reason to take control of their financial futures.

Getting Off the Paycheck-to-Paycheck Treadmill

For generations, the path seemed so clear: land a good job, put in your 40 years, and ride off into the retirement sunset. That model is definitely showing its age. Layoffs, unexpected career changes, and life's curveballs can throw a wrench into even the most seemingly stable job. Building multiple income streams is your personal safety net—one you build yourself, for yourself.

This guide is designed for real life, not some get-rich-quick fantasy. We’re going to walk through how to use what you already have: your skills, your passions, and your life experience.

The goal isn’t to juggle three different jobs. It’s about building a smart, interconnected system where your time, knowledge, and capital work in concert to create a stable financial future.

Your Roadmap to Financial Diversification

This journey is all about taking intentional action, not just adding more to your plate. Before we get into the weeds, it helps to see the path ahead. This guide breaks the entire process down into manageable phases, so you can build momentum without getting overwhelmed.

To give you a better sense of the big picture, here's a quick look at the core phases we'll be covering. Think of it as your high-level map from idea to implementation.

Your Income Stream Roadmap At a Glance

| Phase | Objective | Key Action |

|---|---|---|

| 1. Self-Assessment | Identify your unique skills, passions, and available resources. | Complete a personal inventory of your strengths and assets. |

| 2. Ideation & Validation | Brainstorm and research potential income streams that align with your assessment. | Test your top ideas with small-scale experiments to check viability. |

| 3. Strategic Planning | Develop a detailed action plan, including financial projections and timelines. | Create a business plan for your chosen stream(s), setting clear goals. |

| 4. Implementation | Launch your first income stream and begin generating revenue. | Execute your plan, focusing on initial setup and customer acquisition. |

| 5. Scaling & Optimizing | Grow your existing streams and explore adding new ones. | Analyze performance, refine your processes, and reinvest for growth. |

Each phase builds on the one before it, shifting your mindset from just earning a living to actively designing one. If you're serious about building wealth, you might also find our guide on the 5 essential steps to becoming rich a helpful next step.

Discovering Your Untapped Assets and Skills

Before you can build anything new, you have to know what materials you’re working with. Most people I’ve worked with over the years drastically underestimate the value of the skills, knowledge, and resources they've picked up over a lifetime. This is why the journey to multiple income streams always starts with a personal inventory—one that goes far beyond a resume.

This isn’t just a box-ticking exercise. It's the foundational step that ensures whatever you build feels authentic and sustainable, not just like another job you have to do. It’s about building on who you already are. Truth is, many of your most valuable assets are hiding in plain sight, often dismissed as "just a hobby" or an everyday responsibility.

Looking Beyond Your Job Title

Your professional life is a goldmine, but not just for the job title you held. Think about the other skills you had to develop just to get the work done. Did you spend years navigating tricky office politics or managing tight household budgets? That’s high-level negotiation and financial planning right there.

I once worked with a retired accountant. He thought his expertise with spreadsheets was a retired skill. But we reframed it. That knowledge became the foundation for a profitable financial coaching service for young families just starting out. It’s the same for a stay-at-home parent who has mastered meal planning and organization—that’s the exact framework for a valuable digital planner or an online course.

This shift in perspective is everything. You aren’t starting from scratch; you’re building on decades of lived experience.

“You don’t need MORE customers. You need more products and services to sell to the same customers.” - Lynsey Taulbee, Muddy Acres Flower Farm

Lynsey’s insight here is powerful. Monetization often comes from deepening the value you offer, and that always begins by recognizing the full spectrum of value you already possess.

Cataloging Your Hidden Strengths

To truly figure out how to create multiple income streams, you need to get specific about your assets. So, grab a notebook and start brainstorming. Don't filter yourself or second-guess what comes up; just write it all down.

- Professional Expertise: What were you known for at work? Were you the go-to person for solving a particular problem, organizing events, or mentoring new hires?

- Perfected Hobbies: Do you bake incredible bread, have a knack for gardening, or enjoy woodworking? These passions can become workshops, local sales, or digital guides. A recent study even showed that nearly 44% of hobbyists have turned their pastime into a source of income.

- Life Experiences: Have you successfully navigated a complex process like helping your kids with college applications, caring for an elderly parent, or planning a massive family reunion? This firsthand knowledge is a marketable skill.

Assessing Your Tangible and Intangible Resources

Your assets aren't just skills. They also include things you own and people you know. This part of your inventory can reveal opportunities to generate income with very little upfront effort.

Tangible Assets to Consider

- Property: A spare room, a vacation home, or even an unused garage can be rented out for short-term stays or storage.

- Vehicles: Have a spare car, truck, or RV just sitting there? It can be rented on platforms like Turo or Outdoorsy, turning a depreciating asset into a cash-flowing one.

- Equipment: Specialized tools, camera gear, or sound equipment you own can easily be rented out to others in your community.

Intangible Assets Are Just as Powerful

- Your Network: Who do you know? Your web of former colleagues, community members, and friends is an incredible resource for finding clients, partners, or your first customers.

- Your Reputation: If you're known in your community as trustworthy and knowledgeable on a certain topic, you already have a brand. That credibility is invaluable.

- Your Digital Presence: Do you have a small following on social media or a blog you write for fun? You already have an audience you can potentially serve in new ways.

By completing this deep-dive inventory, you’re not just listing skills; you’re uncovering potential business models. Each asset is a seed for a new income stream, one that is genuinely grounded in your unique life. This is the authentic starting point for building a resilient, diversified financial future.

Choosing the Right Income Stream for You

Now that you have a good handle on your personal assets, let's talk about the fun part: exploring the different kinds of income streams you can build. Not all income is created equal, and knowing the difference is critical to putting together a financial plan that actually fits your life. The real secret to how to create multiple income streams isn't just about adding more; it's about choosing the right ones for the right reasons.

The three big categories are Active, Passive, and Portfolio income. Each has its own distinct role, and frankly, the most durable financial plans I've seen over the years have a healthy mix of all three. Think of it like building a well-rounded team—you need different players with different strengths. One isn't necessarily "better" than another; its value comes down to your personal situation and what you're trying to accomplish.

Understanding Active Income

Active income is what most of us know best. It’s the money you earn by directly trading your time and effort. Your main job, a pension, even Social Security benefits—they all fall under this umbrella. When you're branching out, a new active income stream usually looks like a side hustle where you're actively doing something for someone else.

The big appeal here? It’s often the quickest way to get cash flowing. For anyone in a career transition or a retiree with a lifetime of experience, this is the lowest-hanging fruit. Your professional expertise is an asset you can monetize almost immediately.

Examples of Active Income Streams

- Consulting or Coaching: A retired project manager I know started offering his services to small businesses. They were struggling with organization, and his decades of experience were exactly what they needed.

- Freelancing: A former marketing pro can easily pick up freelance writing or social media management gigs.

- Direct Services: One grandmother I worked with loved baking. She started selling custom cakes for local family events and built a wonderful little business from her passion.

The upside is the direct control—the more you work, the more you can earn. But there’s a trade-off, of course. It’s not scalable. If you stop working, the money stops coming in.

Exploring the Power of Passive Income

Passive income is one of the most misunderstood concepts in personal finance. It’s not about getting something for nothing. It’s about doing the work upfront to create an asset that keeps generating revenue with very little ongoing effort from you. This is how you start to truly separate your time from your earnings, which is a game-changer.

And it’s not just a niche strategy anymore. Recent data shows just how much side hustles are contributing to people's finances. In the United States, over 36% of the population has a side hustle. The average person doing this brought in about $891 per month in 2024, a noticeable jump from $810 in 2023. You can see more on the rise of side hustle earnings in Hostinger's recent report. This tells us that even smaller, secondary income streams are making a real financial impact.

For a family steward, this could be as simple as creating an e-book of treasured family recipes. All the effort is in the beginning—compiling, formatting, and publishing it. Once it's available online, it can sell for years with almost no additional work.

The real magic of passive income is that it builds a financial foundation that supports you even when you’re not actively working. It buys you time, freedom, and peace of mind.

Examples of Passive Income Streams

- Digital Products: Create and sell an online course, an e-book, or a set of digital planners.

- Rental Income: Earn money from a spare room, a vacation property, or even a vehicle you're not using.

- Affiliate Marketing: Get a commission by recommending products you genuinely use and trust on a blog or social media.

This approach requires some patience and an initial investment of either time or money, but the long-term rewards can be massive.

When deciding between putting your effort into an active or passive stream, it helps to see the trade-offs side-by-side.

Active vs Passive Income Trade-Offs

This table breaks down the key differences to help you decide which type of income stream best fits your current goals and resources.

| Characteristic | Active Income (e.g., Freelancing) | Passive Income (e.g., Digital Product) |

|---|---|---|

| Time Investment | Ongoing; directly tied to earnings | Heavily front-loaded; minimal ongoing effort |

| Income Speed | Fast; can start earning almost immediately | Slow; takes time to build the asset |

| Scalability | Low; limited by the hours you can work | High; can earn 24/7 without your direct involvement |

| Risk | Lower initial risk; based on existing skills | Higher upfront risk; no guarantee of success |

| Control | High direct control over tasks and output | Less direct control after the initial creation |

Ultimately, your choice depends on whether you need money now (active) or are willing to build something for future freedom (passive). Many people start with active income to fund their passive income projects.

Making Your Money Work with Portfolio Income

Portfolio income is money generated from your investments. This is the classic definition of making your money work for you, and it’s an absolutely crucial piece of the puzzle for long-term wealth, especially for retirement planning or creating a legacy. It's the most hands-off form of income, relying on your capital and a solid investment strategy rather than your time.

This type of income can come from many different places, and its real power is in compounding—it grows on itself over time, which can dramatically accelerate your wealth.

- Dividend Stocks: Receiving regular cash payments from companies you've invested in.

- Interest Earnings: Gaining income from high-yield savings accounts, bonds, or even peer-to-peer lending platforms.

- Capital Gains: Profiting from selling an asset—like stocks or real estate—for more than you paid for it.

Portfolio income is the bedrock of long-term financial independence. If you're curious about how to build a strategy around this, our guide on how living off interest is a real possibility dives deeper into making your capital your primary earner. A smart, balanced approach that combines active, passive, and portfolio streams is what creates a truly diversified and resilient financial life.

Creating Your Financial Action Plan

An idea without a plan is just a wish. After exploring what income streams are possible, it’s time to get practical about the two resources everyone is short on: time and money.

This is where you stop dreaming and start building. You create a blueprint that respects your current life while laying the foundation for your future financial stability. A solid action plan turns those big, abstract goals into small, concrete steps you can take today.

Don't just gloss over this part. The planning phase is absolutely critical, especially as people's mindsets around money have shifted. Surveys show that in 2025, an overwhelming 83% of Americans now see multiple income streams as essential. It's not a "nice-to-have" anymore; it's a necessity.

And it’s not just about active work. Nearly 88% agree that passive income is a critical piece of the retirement puzzle. This highlights a massive shift toward building wealth through diversified means. You can see more data on this in a comprehensive IPX 1031 report. The message is clear: a thoughtful plan is what separates success from failure.

Mastering Your Time with Intentional Planning

For family stewards, retirees balancing grandkids and hobbies, or anyone with a full plate, the biggest hurdle is almost always time. The answer isn't to magically create more hours in the day—it’s to manage the ones you have with purpose.

A strategy I've seen work wonders for countless people is time blocking.

Instead of a vague to-do list that gets pushed to tomorrow, you schedule appointments with yourself. Your calendar becomes your command center.

- Sunrise Session (6:00 AM - 7:00 AM): Carve out one hour, three days a week, to work on your new venture before the rest of the world demands your attention.

- Lunch Break Power Hour (12:00 PM - 1:00 PM): Use just 30 minutes of your lunch break for quick admin tasks—firing off emails, scheduling a social media post. It adds up.

- Quiet Evening Block (8:00 PM - 9:30 PM): Once the kids are in bed or the house is quiet, schedule a 90-minute block for deep work. This is prime time for writing blog content or developing that digital product.

Treat these appointments with the same respect you'd give a doctor's visit. By protecting this time, you build real, tangible momentum.

Allocating Capital Smartly

Next up is capital. One of the most persistent myths I hear is that "you need money to make money." That's just not true anymore. Many powerful income streams can be started with little to no initial investment. Your plan just needs to match your financial reality.

Zero-Capital Launch Plan

This is all about monetizing what you already have: your skills, your knowledge, your experience. The startup costs are practically zero, making it a fantastic low-risk way to get started.

- Offer a Service: Put your professional skills to work with freelance writing, virtual assistance, or consulting.

- Package Your Knowledge: Create a simple e-book or guide using free tools like Canva and sell it on a platform with low fees.

- Build a Community: Start a free newsletter or social media group around a topic you love. Build an audience first, and monetization will follow.

Small-Investment Launch Plan

Some ideas do require a little seed money to get off the ground. The key is to be strategic and keep those initial costs lean.

- E-commerce: Use a small budget to buy your first batch of inventory for an Etsy shop or a store on Shopify.

- Digital Tools: Invest in specialized software for an online course or paid subscriptions that help with marketing.

- Basic Equipment: A good microphone can make all the difference for a podcast. Specific tools might be needed for a crafting business.

And for those of you eyeing portfolio income, remember that even a small, consistent investment can grow into something substantial over time. To get a better handle on the basics, you might want to look over our beginner's guide on investing for dummies in 2025.

Managing Risk and Taxes from Day One

Finally, let's talk about the less glamorous but absolutely essential side of things: risk and taxes. Ignoring these from the beginning can turn a profitable idea into a stressful nightmare down the road.

Your first and most important financial step is to open a separate bank account for your new income stream. Do not mix business and personal funds. This simple action will make tracking income, managing expenses, and handling taxes infinitely easier.

Risk Mitigation:

Don't go all-in right away. Start with a small, testable version of your idea. Before you pour hundreds of hours into a full online course, offer a single live webinar to see if people will actually pay for it. Instead of buying a thousand units of inventory, start with twenty and see what sells. This "validation" step protects your wallet by confirming there's real demand.

Tax Considerations:

Remember, the money you earn from a side business isn't taxed like a regular paycheck. No one is withholding for you. A good rule of thumb is to set aside 25-30% of every dollar you earn into a separate savings account just for taxes. Do this from day one. It ensures you’re ready for quarterly estimated tax payments and won’t get a nasty surprise from the IRS come tax time.

How to Launch and Scale Your Income Streams

Alright, this is where the rubber meets the road—turning all that careful planning into actual, tangible income. We're moving from idea to profit, but it requires a smart, deliberate process. The goal here isn't to just give yourself another job. It's to launch a cohesive system of income streams that grows your wealth without burning you out.

It all starts with one critical phase: validation. Before you pour significant time or money into a big launch, you need to prove your idea has legs in the real world.

Start with Low-Risk Validation

Validation is just a fancy word for a small, low-risk test. You're basically asking the market, "Hey, would you actually pay for this?" and getting a "yes" before you go all-in. Think of it as a pre-launch to your official launch.

This simple step can save you from pouring your heart, soul, and savings into something nobody wants. It’s the smart, calculated way to begin.

- Got a Service Idea? Offer it to a small group at a discounted "beta" rate. Their feedback will be pure gold, and their testimonials will become your very first marketing assets.

- Thinking of a Digital Product? Instead of building a massive 10-module course, host a single paid webinar on the topic. If you can sell 20 spots, you've just proven your concept is viable.

- Creating a Physical Product? Don't order 500 units from a manufacturer right away. Make a small batch of 10-15 items and try selling them at a local market or to your social circle.

Mini Case Study: The Engineer Turned Etsy Woodworker

I worked with a client, Mark, a retired engineer who loved woodworking. He dreamed of selling his handcrafted cutting boards but was terrified of investing in expensive tools and bulk lumber before he knew if anyone would buy them.

Instead of launching a full-blown business, he took a validation-first approach. He made just five unique boards, snapped some photos with his smartphone, and listed them on Etsy. He then shared the listings with family and friends. Within two weeks, all five had sold. That initial interest was the green light he needed. It wasn’t a massive windfall, but it was proof of demand, and it gave him the confidence to slowly invest more.

Moving from Validation to Launch

Once you have proof that people are willing to open their wallets, it’s time for a more formal launch. This is where you put a simple but effective system in place to attract customers and process sales.

Now, don't get bogged down by the need for perfection. A "good enough" launch that's actually live is infinitely better than a "perfect" plan that never sees the light of day. Your initial setup should be lean and focused.

Your Essential Launch Toolkit:

- A Simple "Storefront": This could be an Etsy shop, a basic one-page website, or even a well-optimized social media profile. It's just a central place where people can learn about what you're offering and make a purchase.

- A Way to Get Paid: Set up a reliable payment processor. Tools like Stripe or PayPal are easy to integrate and keep things simple and secure.

- A Basic Marketing Plan: How will people find you? Start with one channel you already know well. If you're comfortable on Facebook, start there. If you prefer in-person connections, focus on local community groups.

Mini Case Study: The Nurse and the Niche Health Blog

Let's look at another example. Sarah, a nurse, wanted to build an income stream sharing her expertise on managing chronic pain. Instead of sinking thousands into a complex website, she started a simple blog and focused on one thing: writing incredibly helpful articles.

Her launch was as straightforward as it gets. She shared her posts in a few relevant online forums for chronic pain sufferers. Her authentic, expert advice resonated immediately, and a small but fiercely loyal audience began to form. Only after building that initial trust did she create her first product—a simple e-book on pain management techniques. The launch was a success because she had already validated the demand for her knowledge.

The most successful income streams aren’t born from a single grand opening. They are built through a series of small, validated steps, each one building on the success of the last.

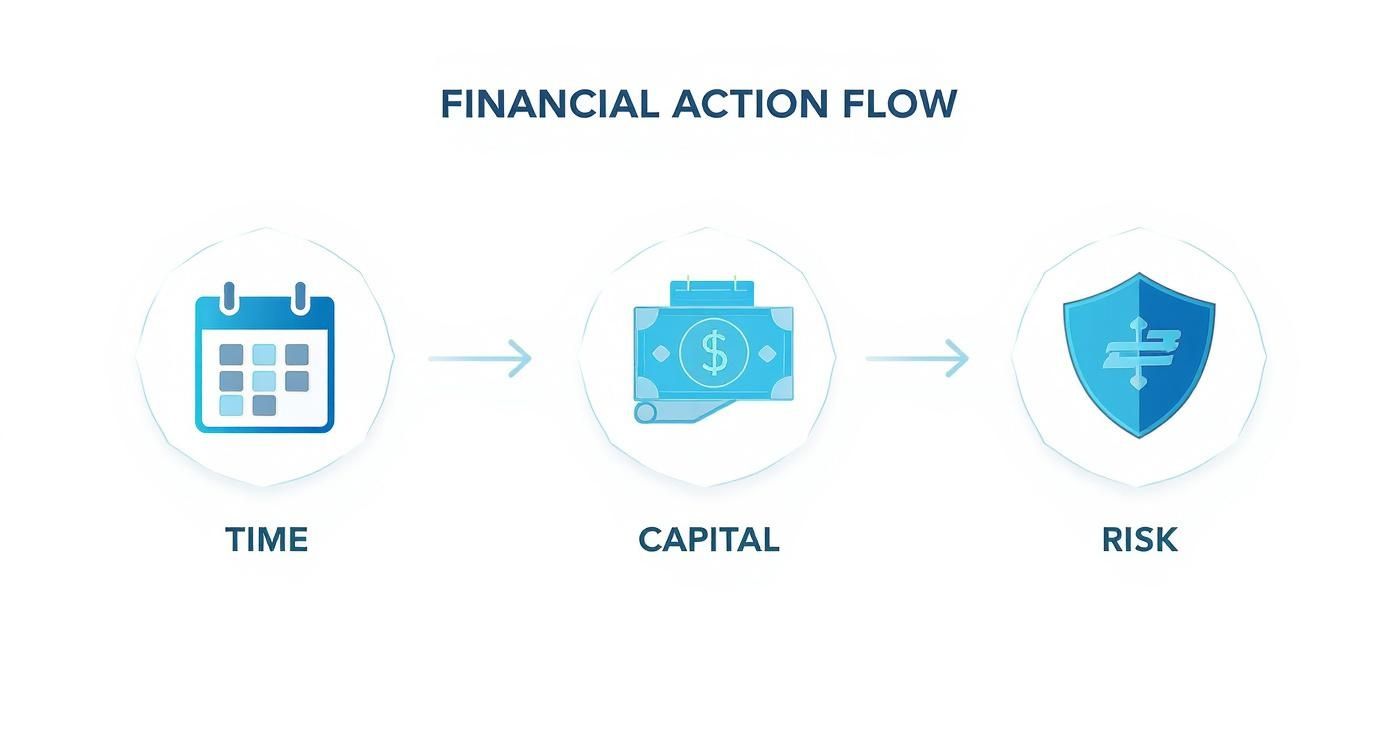

The Art of Scaling and Automation

Once your income stream is consistently bringing in money, it's time for the final phase: scaling and automation. This is how you reclaim your time and ensure your business can grow beyond your direct, daily involvement. Scaling isn’t about working harder; it’s about creating smart systems.

The infographic below shows how your focus shifts as you move from planning to launching and eventually to scaling.

As you can see, your relationship with time, capital, and risk evolves. You move from hands-on effort toward strategic oversight and system-building.

Practical Ways to Scale:

- Automate Your Marketing: Use email marketing tools to send welcome messages or follow-ups automatically. You can also schedule social media posts weeks in advance.

- Systemize Fulfillment: If you sell physical products, create a streamlined, repeatable process for packing and shipping. For digital products, make sure the delivery is fully automated after purchase.

- Hire Targeted Help: You don’t need a full-time staff. Start small. Hire a virtual assistant for just five hours a week to handle the administrative tasks that drain your energy and time.

The real goal is to build an asset, not just another job. By validating first, launching lean, and then intentionally scaling, you create a resilient income stream that serves your financial goals for years to come.

Of course. Here is the rewritten section, crafted to sound like an experienced human expert and match the provided examples.

Common Questions About Building Income Streams

Venturing into the world of multiple income streams naturally kicks up a lot of dust. This is where the practical, "what-if" questions start to surface, and it’s easy to feel a bit intimidated. Let's tackle some of the most common ones I've heard over the years with some straight, actionable advice to get you moving forward with confidence.

How Many Income Streams Is Too Many?

There's no magic number here, and the goal is always quality over quantity. The single biggest mistake I've seen in my 50+ years of doing this is people trying to do way too much, too soon. That’s a fast track to burnout, not wealth.

Start by adding just one new stream to whatever your primary income is—be it your job or a pension. Pour all your initial energy into making that one stream stable and consistent. Only after it’s humming along should you even think about adding another.

For most folks, a solid, manageable portfolio often settles into three distinct sources:

- Your Primary Income: The main engine, like your job, business, or pension.

- A Semi-Passive Stream: Something like a digital product or a rental property that brings in money without your constant, hands-on effort.

- A Portfolio Stream: Investments that put your capital to work for you, think dividend stocks or interest from savings.

Trying to juggle five different active side hustles at once is just a recipe for failure. Start small, get it stable, and then expand thoughtfully.

What Are the Best Low-Cost Ideas to Start?

The best low-cost income streams are almost always the ones that use the skills you already have. These are the opportunities where you invest your time and expertise, not a pile of cash.

Service-based streams are a fantastic place to start. Think about offering your professional know-how through freelance writing, virtual assistance, or consulting in a field you know well. You're selling what's already in your head, so the financial outlay is practically zero.

Another powerful, low-cost area is creating simple digital products. If you have a knack for organization, you could sell downloadable planning templates. Or, if you have deep knowledge on a niche topic, you could write a short e-book using free tools like Canva, completely sidestepping the overhead and risk of physical inventory.

The real key is to monetize what you already know and have. Your life experience is your most valuable—and lowest-cost—asset.

How Should I Handle Taxes for Extra Income?

This is non-negotiable. You have to get this right from day one. A simple, safe rule of thumb is to set aside 25-30% of every single dollar you earn from your side income, just for taxes.

Go open a separate savings account for this purpose. Do it now. This is critical because, unlike a W-2 job, no one is withholding taxes for you. To avoid a nasty surprise and penalties from the IRS, you'll almost certainly need to pay estimated taxes quarterly.

Just as important, you need to track every single business-related expense—from software subscriptions to materials you buy. These are often deductible and will lower your total taxable income. Honestly, one of the smartest moves you can make is investing in a consultation with a tax professional for your first year. It pays for itself.

Can My Family Get Involved in This?

Absolutely! In fact, bringing family into the mix can be an incredibly powerful way to build wealth and legacy together. It transforms a personal project into a collaborative, multigenerational effort.

For instance, a tech-savvy grandchild could run the social media marketing for a business you start. Or a family might decide to pool resources to invest in a small rental property together. You could even launch a small business around a shared family passion, whether that’s crafting, baking, or gardening.

The foundation for making this work is crystal-clear communication. You have to define roles, responsibilities, and—most importantly—how any income will be shared or reinvested. When you get it right, it stops being just about money and becomes a project that truly strengthens family bonds.

At Smart Financial Lifestyle, our goal is to provide you with the wisdom to build a secure and meaningful financial future. To continue your journey, explore more of our guides and resources at https://smartfinancialifestyle.com.