When it comes to your financial legacy, you want things to be crystal clear. A will is a great start, but a lot of people are surprised to learn it doesn't actually control every asset you own. This is where a beneficiary designation becomes one of the most powerful—and simplest—tools in your entire estate plan.

So, what is it? A beneficiary designation is a direct instruction you give to a financial institution, like a bank or insurance company. It tells them exactly who should inherit that specific account when you pass away. Think of it as a special delivery slip for your assets that avoids the long, often expensive trip through probate court.

The Power of a Beneficiary Designation

This simple form acts as a direct, legally binding contract between you and the institution holding your money. It's a clear order that says, "When I'm gone, give this asset directly to this person." This direct-transfer mechanism is incredibly efficient for a few key reasons:

- It Bypasses Probate: Assets with a named beneficiary are not part of your probate estate. That means they skip the delays, court fees, and public nature of the probate process.

- It Overrides Your Will: This is the big one. If your will says your estate goes to your kids, but your IRA beneficiary is your brother, your brother gets the IRA. The designation form wins, no matter what your will says.

- It Provides Speed and Simplicity: Beneficiaries can typically claim the assets within weeks, just by providing a death certificate and filling out some paperwork. It offers swift financial support when it's needed most.

To put it in perspective, let's take a look at the core functions of a beneficiary designation.

Key Features of a Beneficiary Designation

This table offers a quick summary of what makes this tool so effective in an estate plan.

| Feature | Description | Primary Benefit |

|---|---|---|

| Direct Transfer | Assets pass directly from the financial institution to the named person(s). | Avoids probate court entirely. |

| Legal Precedence | The designation form legally overrides instructions written in a will for that specific account. | Ensures your exact wishes for that asset are followed. |

| Speed of Access | Beneficiaries can typically access funds quickly, often within weeks. | Provides immediate financial support to loved ones. |

| Simplicity | It's usually a simple, one-page form provided by the financial institution. | Easy to set up and update as life changes. |

Understanding these features is the first step toward building a truly effective plan that protects your family from unnecessary complications.

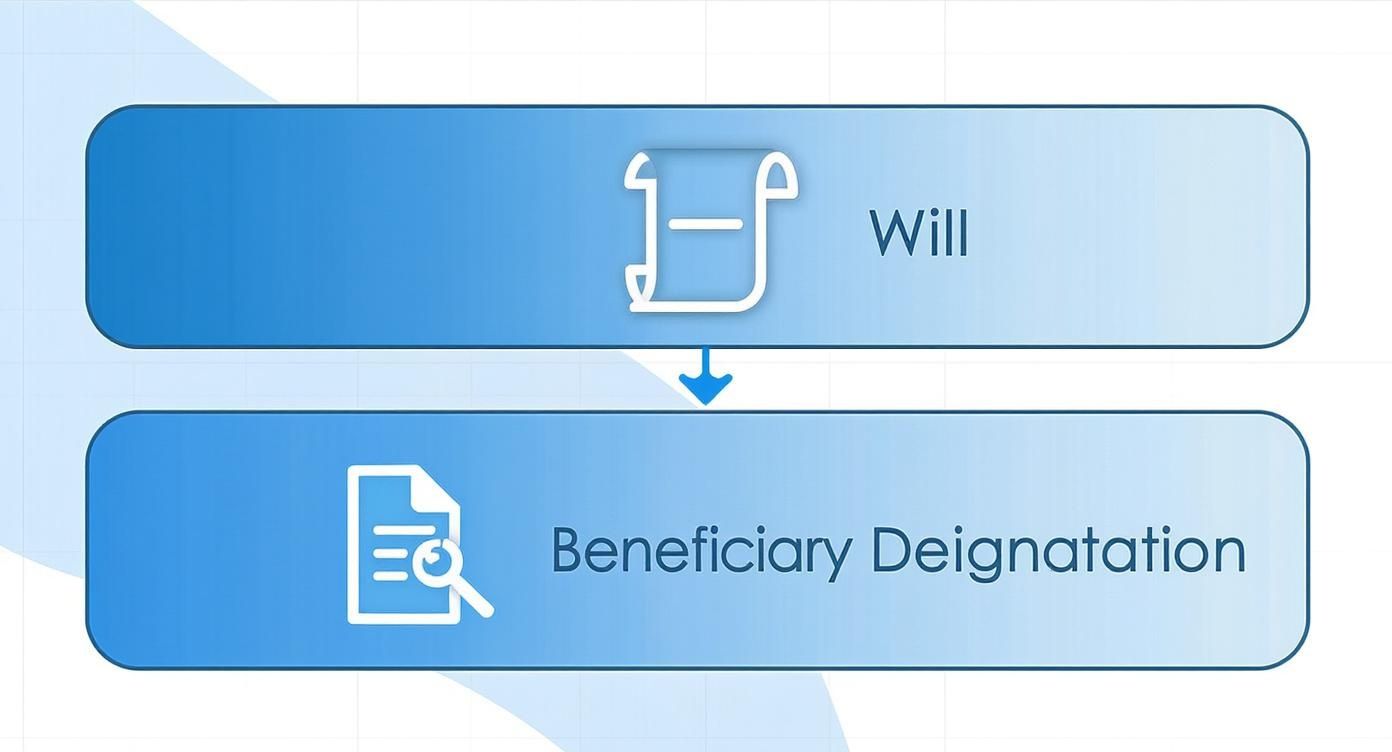

An Express Lane for Your Assets

Think of your will as a detailed road map for your estate's executor. It guides them through the complex legal system of probate court, with all its potential detours and traffic jams. A beneficiary designation, on the other hand, is like a non-stop flight for a specific asset. It takes that account directly to its intended destination, with no layovers in the court system.

This distinction is why forgetting to update these forms can be so devastating. In my 50+ years of experience, I've seen a family torn apart when a forgotten 401(k) beneficiary form sent a huge inheritance to an ex-spouse, directly contradicting a carefully updated will.

It's a common mistake. Statistics from the Social Security Administration show that over 90% of 401(k) participants name a beneficiary, but failing to keep that name current is where the trouble starts. For anyone serious about protecting their family, mastering this simple form is non-negotiable. It's the cornerstone of any strategy designed to keep your assets in the hands of your loved ones and out of legal limbo.

When you fill out a beneficiary designation form, you’re doing more than just jotting down a name. You’re actually creating a succession plan for your assets. Think of it like a sports team: you have your starting player and your backup, and each one has a very specific role. This is the core idea behind primary and contingent beneficiaries.

Your primary beneficiary is your first choice—the starting player, so to speak. This is the person, trust, or organization you want to receive the asset directly when you pass away. You can name one primary beneficiary or split the asset among several people by assigning percentages, just as long as it all adds up to 100%.

But what if your primary beneficiary can’t inherit the asset for some reason? This is where your backup plan comes in, and it's absolutely critical.

The Critical Role of Contingent Beneficiaries

A contingent beneficiary is your second choice. They only step in to inherit the asset if all of your primary beneficiaries have passed away before you do, or if they formally "disclaim" the inheritance (which just means they refuse to accept it). Naming a contingent beneficiary isn’t just a good idea; it's a vital safeguard for your entire financial plan.

Without a contingent beneficiary, if your primary beneficiary isn't around when you pass, the asset is left in limbo with no clear destination. In most cases, the financial institution has no choice but to pay the money to your estate. This is the exact scenario you were trying to avoid—it forces the asset into probate, triggering court involvement, legal costs, and long delays for your family.

"In my 50+ years of helping families, the most heartbreaking and avoidable mistakes often stem from a single missing name on a form. Failing to name a contingent beneficiary is like building a bridge with no support pillars—it only takes one point of failure for everything to collapse into a legal mess for your loved ones."

—Paul Mauro, Founder of Smart Financial Lifestyle

This hierarchy shows just how powerful a beneficiary designation really is. It’s a simple form that often carries more weight than your will for certain accounts.

As you can see, while a will is essential for your overall estate, a beneficiary designation acts as a direct command for specific assets, completely bypassing the will.

Real-World Scenarios: Why You Need Both

Let's look at how this plays out in real life. Imagine a married couple, Sarah and Tom. They have each other listed as the primary beneficiary on their retirement accounts but never got around to naming a contingent beneficiary.

-

Scenario 1: A Tragic Accident

If Sarah and Tom were in a car accident and Tom, the primary beneficiary on Sarah's account, passed away just hours before her, the outcome is the same as if he had died years earlier. Since he predeceased her, her retirement account is left with no living beneficiary. The money defaults to her estate, gets tied up in probate, and is eventually distributed according to her will—but only after months or even years of legal headaches. -

Scenario 2: The Proactive Approach

Now, let's say Sarah had named their adult daughter, Emily, as the contingent beneficiary. In the exact same tragic scenario, because Tom was no longer able to inherit, the asset would pass directly and immediately to Emily. No probate, no court, and no unnecessary stress during an already devastating time.

This simple act of naming a contingent beneficiary creates a crucial "Plan B" that ensures your wishes are honored, no matter what life throws your way. It’s a foundational step in making smart financial decisions that truly protect your family’s future.

How Beneficiary Designations Affect Life Insurance and Retirement Accounts

While you can name a beneficiary on many different accounts, they carry the most weight by far on two specific types: life insurance policies and retirement plans like your 401(k) or IRA. For these assets, the beneficiary designation isn’t just a suggestion—it's an ironclad contract that dictates exactly who gets your money.

Think of it this way: your will is the captain of your financial ship, guiding where most of your estate goes. But when it comes to life insurance and retirement accounts, the beneficiary form is the admiral. It has the power to give a direct order that overrides everyone else, including the captain.

This is exactly why getting this part of your financial plan right is so critical.

The Unbreakable Promise of Life Insurance

With a life insurance policy, your beneficiary designation is the heart of the whole agreement. It names who receives the tax-free death benefit, and the insurance company is legally bound to pay that specific person directly and quickly.

This direct payment is a foundational feature of life insurance. In fact, about 51% of American adults have some form of life insurance, and industry data from places like ConsumerAffairs.com shows that over 95% of policies name at least one primary beneficiary. Spouses and children are the most common choices, which shows how this tool is used to provide immediate financial stability for loved ones.

Because it’s a direct contract, the money from a life insurance policy almost never has to go through the probate process. It also stays out of reach of creditors trying to make a claim on your estate. This ensures the funds are protected and get to your family when they need them most, which is a big reason why people decide life insurance is worth it for their situation.

Retirement Accounts and Their Tax Implications

For retirement accounts like a 401(k), 403(b), or IRA, the beneficiary designation is just as powerful—but with an added layer of complexity: taxes. Who you name determines not only who gets the money but also how and when it can be withdrawn and taxed.

A spouse who inherits a retirement account usually has the best options. They can typically roll the funds into their own IRA, letting the money continue to grow tax-deferred and pushing back any required minimum distributions (RMDs) until they reach their own retirement age.

It's a different story for non-spouse beneficiaries, like children or siblings. While they still get the money, they're generally required to withdraw all the funds within a 10-year period. If the account is large, that can trigger a massive tax bill.

In my 50+ years of experience, the most devastating financial mistake I’ve seen involves a forgotten beneficiary on an old 401(k). I once worked with a family where a man's entire retirement account from his first job—worth hundreds of thousands of dollars—went directly to his ex-wife of 20 years. His updated will meant nothing. His current wife and children got nothing from that account because a single form was never changed after his divorce.

This kind of story is a gut-wrenching reminder that beneficiary designations have massive, and often irreversible, financial consequences. They are not "set it and forget it" documents. Regularly reviewing and updating them is one of the most important things you can do to protect your legacy and make sure your money ends up exactly where you intend.

Navigating Complex Scenarios with Minors, Divorce, and Trusts

Life is rarely a straight line, and certain events can throw a real wrench into even the most carefully crafted financial plan. When you're dealing with something as powerful as a beneficiary designation, you absolutely have to navigate these situations with care to protect the people you love.

Major life changes are a flashing red light, signaling it's time to review these forms. Ignoring them can lead to unintended and often heartbreaking consequences. It’s in these messy, real-life moments that the true power—and potential pitfalls—of a beneficiary designation become crystal clear.

![]()

The Problem with Naming a Minor Directly

It’s the most natural instinct in the world to want to leave assets to your children or grandchildren. But naming a minor directly as a beneficiary is a classic mistake, one that can create a legal and financial nightmare for your family.

Here's why: financial institutions can't legally just hand over large sums of money to a child. If a minor inherits an account, the funds are essentially frozen. A court has to step in and appoint a legal guardian to manage the money until they're an adult. It's an expensive, public, and painfully slow process.

Worse yet, the court-appointed guardian might not be the person you would have chosen. The money will then be locked away in a restrictive account until the child turns 18 or 21, depending on your state.

Fortunately, there are far better ways to provide for a minor:

- Custodial Accounts: You can name a trusted adult as a custodian for the minor under the Uniform Transfers to Minors Act (UTMA). This lets someone you choose manage the funds for the child’s benefit, completely bypassing court intervention.

- Trusts: For the ultimate control, naming a trust as the beneficiary is the gold standard. You can spell out exactly how and when the funds should be used for the child's education, health, and general well-being.

Divorce: A Dangerous Assumption

This is one of the most dangerous myths I see in estate planning: people assume their divorce decree automatically removes their ex-spouse as a beneficiary. This is completely false.

A beneficiary designation is a direct contract you have with a financial company. A divorce court order does not automatically override it. If you don't physically submit a new form to change the beneficiary, your ex-spouse will legally inherit that asset—no matter what your will or divorce settlement says.

In my 50+ years of experience, I've had to console a grieving widow who discovered her late husband’s entire multi-million dollar life insurance policy was going to his ex-wife from a brief marriage 30 years prior. He simply forgot to change the form. It was a devastating and completely avoidable tragedy.

After a divorce, updating your beneficiary designations should be at the absolute top of your financial to-do list.

Using Trusts as a Strategic Beneficiary

Beyond just providing for minors, naming a trust as a beneficiary is a powerful and strategic move for many families. When you name a trust, you’re not just handing over a lump sum of money; you're giving your loved ones a structured plan for how that money should be managed for the long haul.

This strategy really shines in a few key situations:

- Supporting a Beneficiary with Special Needs: Leaving assets directly to someone with special needs could disqualify them from critical government benefits. A special needs trust can hold the assets for their benefit without jeopardizing their eligibility.

- Protecting Assets for Heirs: If you have a beneficiary who might not be responsible with a large inheritance, a trust lets you control the distributions. A trustee you appoint manages the funds, making sure they're used wisely for that person's long-term well-being.

- Providing Long-Term Care: A trust can create a dedicated pool of money to support an elderly parent or another loved one, ensuring their needs are met for the rest of their lives according to your exact instructions.

For anyone looking to explore this powerful tool, understanding what is a revocable living trust is the perfect place to start. It offers a level of flexibility and control that a simple beneficiary form just can't match.

Common Mistakes to Avoid with Beneficiary Designations

A beneficiary designation is a remarkably simple tool, but in my 50+ years of helping families, I’ve seen just how incredibly easy it is to get wrong. A few common oversights can quickly spiral into devastating and costly mistakes, completely derailing a family's financial future. These aren't complex legal loopholes I'm talking about. They’re simple, everyday errors that can strip your loved ones of their inheritance and you of your peace of mind.

Understanding what a beneficiary designation is, is only half the battle. Knowing how to sidestep these common pitfalls is how you truly protect your legacy. Let’s walk through the mistakes I see most often.

Forgetting to Name a Beneficiary

The most basic mistake of all is simply leaving the beneficiary line blank. When no one is named, the financial institution has no choice but to treat the asset as part of your estate. This single omission completely defeats the purpose of having the designation in the first place, forcing that money directly into the lengthy, public, and expensive probate process.

Your executor will eventually get the money distributed according to your will, but only after it's been chipped away by legal fees and potential creditor claims. It's like buying a non-stop plane ticket and then choosing to send your luggage through a dozen different airports—it just creates unnecessary risk and delay.

The Fix: Always, always name a primary beneficiary for every single eligible account. No exceptions. Go through your life insurance, IRAs, 401(k)s, and even some bank accounts to make sure you have someone clearly listed.

Overlooking the Contingent Beneficiary

Just as critical is failing to name a backup. So many people list their spouse as the primary beneficiary and just stop there, assuming everything is handled. But what happens if your primary beneficiary passes away before you do, or even at the same time? Without a contingent, or secondary, beneficiary, you’re right back where you started: the asset gets dumped into your estate.

Think of it as having no emergency contact. Your contingent beneficiary is your financial first responder, ready to step in if your first choice isn't available.

Using Vague or Unclear Language

Precision is everything when it comes to these forms. Using vague terms like "my children" or "my heirs" is a recipe for disaster. I've seen this kind of ambiguous language lead to bitter, drawn-out family disputes.

- Does "my children" include the stepchildren you raised as your own? What about adopted children?

- What happens if one of your children passes away before you? Does their share go to their kids (your grandchildren), or is it split among your surviving children?

These aren't just hypotheticals. When the language is unclear, financial institutions are forced to freeze the account until a court can interpret your intentions, which costs everyone time, money, and emotional energy.

The Fix: Always use the full, legal names of your beneficiaries. If you're naming multiple people, specify the exact percentage each should receive (e.g., "Jane Marie Smith, 50%; John David Smith, 50%"). Leave absolutely no room for confusion.

The "Set It and Forget It" Mindset

This is probably the most common mistake of all—failing to update your designations after major life events. A beneficiary designation isn't a crockpot meal; you can't just set it and forget it.

Life changes, and your financial plan has to change right along with it. Certain events should trigger an immediate review of all your accounts:

- Marriage or Remarriage: You'll almost certainly want to add your new spouse.

- Divorce: A divorce decree does not automatically remove an ex-spouse from an account. You have to file a new form to make that change official.

- Birth or Adoption: A new child means your plan needs an update.

- Death of a Beneficiary: If someone you've named passes away, you need to revisit your primary and contingent choices right away.

Failing to make these updates is exactly how an ex-spouse from 30 years ago ends up inheriting a life insurance policy that was meant for your current family. This concept is fundamental, even in huge government programs like Social Security, which directs benefits to millions of designated survivors like spouses and children. It's a system built on clear, current instructions. You can discover more insights about Medicare and Social Security beneficiary data from KFF to see just how widespread these designations are.

Your Practical Checklist for Managing Beneficiaries

Knowing what a beneficiary designation is—and the common mistakes people make—is a great first step. Now it’s time to put that knowledge to work.

Managing these critical forms isn’t a one-and-done chore. It’s an ongoing act of care for the people you love. When you treat this process with intention, you make sure your financial plan unfolds exactly as you designed it to.

This isn’t just paperwork. Think of this checklist as your roadmap for sending a clear message of protection to your family and securing your legacy. Let’s walk through the steps to get your assets pointed in the right direction and keep them that way.

Step 1: Gather Your Documents

You can't review what you can't find. The first real step is to create a complete inventory of every single account you own that has a beneficiary designation. Don’t try to do this from memory—it’s too easy to forget an old account. It's time to track down the actual paperwork, whether it's digital or in a file cabinet.

Start by collecting the most recent statements and policy documents for all of these:

- Retirement Accounts: This means 401(k)s, 403(b)s, IRAs (both Roth and Traditional), and any pensions you might have.

- Life Insurance Policies: Pull together the documents for any term and whole life policies, whether they're plans you bought yourself or coverage through an employer.

- Annuities: These are contracts with insurance companies, and they have their own, separate beneficiary forms.

- Other Accounts: Don't overlook any payable-on-death (POD) bank accounts or transfer-on-death (TOD) investment accounts.

Once you have everything in one place, create a simple master list. For each account, note the financial institution, the account number, and where to find the beneficiary information.

Step 2: Conduct a Thorough Review

With all your documents in hand, it's time to perform a detailed audit. For each account, you need to ask yourself three crucial questions:

- Who is my primary beneficiary? Is this still the person (or people) you want to inherit this asset? Make sure you've used their full legal name and double-check the spelling.

- Who is my contingent beneficiary? Do you have a backup named in case your primary beneficiary can't inherit? If not, you have a major gap in your plan that needs to be fixed right away.

- Are the percentages correct? If you have multiple beneficiaries, do the shares you assigned still reflect your wishes? And remember, all the shares must add up to exactly 100%.

This review is your chance to catch problems before they become problems. You might find an ex-spouse still listed on an old 401(k) or spot vague language that could cause confusion for your family down the road.

Step 3: Schedule Regular Updates

A beneficiary designation is a living document because your life is always changing. The single biggest mistake I see people make is setting up their beneficiaries once and then completely forgetting about them.

Certain life events should be automatic triggers, prompting you to pull out your master list and review every single one of your forms.

In my 50+ years of experience, I’ve seen that the most loving and effective financial plans are the ones that are actively maintained. A beneficiary review isn’t just about money; it’s a powerful way to reaffirm your commitment to protecting your family’s future as your lives evolve together.

Life is unpredictable, so it pays to be prepared. When a major change happens, your first thought should be about how it impacts your financial plan and your beneficiaries. It's a habit that provides incredible peace of mind.

To make it easier, here's a table of common life events that should always trigger a review.

When to Review Your Beneficiary Designations

| Life Event | Reason for Review | Potential Action |

|---|---|---|

| Marriage or Divorce | Your primary relationship has fundamentally changed. A divorce decree does not automatically update your forms. | Add a new spouse as a beneficiary or remove an ex-spouse immediately. |

| Birth of a Child | A new person has entered your life who you may want to provide for. | Add the child as a primary or contingent beneficiary, likely using a trust or custodial account. |

| Death of a Beneficiary | If a named beneficiary passes away, your plan may have a critical gap. | Promote a contingent beneficiary to primary or name a new contingent beneficiary. |

| Major Financial Change | A large inheritance or the sale of a business can change your overall estate plan. | Re-evaluate how assets are distributed across all accounts to ensure your plan remains balanced. |

Think of this table as your ongoing checklist. By turning these reviews into a routine, you ensure that your financial legacy always reflects your current wishes, leaving no room for doubt or confusion for the people you care about most.

Common Questions About Beneficiary Designations

Even after you get the hang of what a beneficiary designation does, certain questions always seem to pop up during the actual planning. Let's walk through some of the most common ones I've heard from families over the years and get you some direct, clear answers.

Can I Name My Estate as My Beneficiary?

Technically, you can name your estate as your beneficiary, but it's a move I almost never recommend. Why? Because doing so completely torpedoes one of the biggest perks of using a beneficiary designation in the first place—it shoves the asset right into the probate process.

Once that money is part of your estate, it's subject to court oversight, legal fees, and potential grabs from creditors. It will eventually find its way to your heirs based on your will, but only after a slow, and often expensive, legal slog. The smarter move is almost always to name individuals or a properly structured trust directly on the form.

What Happens If All My Beneficiaries Die Before Me?

This is precisely why naming both primary and contingent (or secondary) beneficiaries is so critical. If every single person you've named on an account passes away before you do, that asset is suddenly left without a designated recipient.

In that scenario, the account defaults back to your estate. Just like naming your estate on purpose, this outcome forces the money into probate court, where it's distributed according to your will or, if you don't have one, state law. This is exactly why a death in the family should be an immediate trigger to pull out and review all of your beneficiary forms.

Paul Mauro's 50+ Years of Experience: "The simplest forms often prevent the biggest headaches. A beneficiary designation is a direct contract with a financial institution, and in most cases, it doesn't need to be notarized or witnessed like a will. Your signature is what makes it a legally binding instruction."

Does a Beneficiary Designation Form Need to Be Notarized?

In the vast majority of cases, the answer is no. A beneficiary designation form is a standard document provided by the financial institution that holds your account—your bank, brokerage firm, or insurance company. You just need to fill it out accurately, sign it, and get it back to them.

That simple act creates a legal contract between you and the institution. A good rule of thumb, though, is to always ask for written confirmation that they've received and officially recorded your updated designation in their system. This simple step ensures your wishes are locked in and leaves no room for error down the road.

At Smart Financial Lifestyle, we believe that making smart financial decisions is about creating clarity and security for your family. Understanding the details of your beneficiary designations is a powerful step in that journey.

To continue building your financial wisdom, visit us at https://smartfinancialifestyle.com.