Planning to protect your assets from nursing home costs is a lot like planning for retirement. You need a proactive strategy, and the sooner you start, the better your options will be. The goal is to use legal tools, like irrevocable trusts, to legally separate your savings and home from your name long before you might need care.

This isn't about hiding money. It's about understanding the rules—especially Medicaid's five-year look-back period—and making sure your life's savings aren't counted when determining eligibility for government help. If you wait until there's a crisis, your choices become dramatically limited.

The Financial Reality of Long-Term Care Costs

It’s a conversation most families would rather put off, but it’s one of the most important ones you’ll ever have for your financial survival. Long-term care might feel like a distant problem, but its financial impact can arrive with stunning speed, capable of wiping out a lifetime of careful saving in just a few short years.

Facing this reality isn’t about dwelling on the negative. It's about empowering yourself to take control. The first step toward building a solid defense is truly understanding the sheer scale of the costs involved, which are often far higher than people imagine.

The hard truth is that a prolonged nursing home stay represents one of the single greatest financial threats to the average American family's legacy and retirement security. Without a plan, your assets are exposed and vulnerable.

This isn't a problem you can afford to ignore. Once care begins, the financial pressure is immediate and relentless, leaving very little room for error.

Breaking Down the Staggering Numbers

Let's put some concrete figures to this challenge. As of 2024, the average cost for a semi-private room in a U.S. nursing home is around $9,277 per month. That adds up to about $111,325 annually.

Need a private room? The average jumps to $10,646 per month, or roughly $127,750 per year. These numbers underscore why proactive planning isn't just a good idea—it's an absolute necessity. Very few retirement accounts can withstand that kind of financial drain for long.

An Overview of Asset Protection Strategies

The good news is that you have options. Throughout this guide, we'll walk through the specific methods and legal tools designed to shield your assets from nursing home costs. Each strategy serves a different purpose and is better suited for certain family situations and timelines.

If this feels overwhelming, our guide on how to approach long-term care costs can provide a solid foundational perspective.

To give you a roadmap for what’s to come, here’s a quick overview of the core strategies we'll be covering.

At-a-Glance Asset Protection Strategies

Navigating the world of asset protection can feel complex, but the main strategies each have a clear purpose. This table breaks down the most common approaches, who they're generally best for, and a key point to keep in mind for each one.

| Strategy | Best For | Key Consideration |

|---|---|---|

| Medicaid Planning & Trusts | Those planning 5+ years in advance. | Requires giving up control of assets. |

| Long-Term Care Insurance | Healthier individuals in their 50s-60s. | Premiums can be high and may increase. |

| Medicaid Compliant Annuities | Crisis situations (immediate need for care). | Converts assets to income; complex rules apply. |

| Spousal Protections | Married couples where one spouse needs care. | Specific rules protect the community spouse. |

Think of this table as a starting point. As we dive deeper into each strategy, you'll get a much clearer picture of how these tools can fit into your own financial plan.

Navigating the Medicaid Look--Back Period

When it comes to protecting your assets from nursing home costs, timing isn't just important—it's everything. The reason boils down to one critical, often misunderstood rule: the Medicaid look-back period. Getting a handle on this rule is the absolute first step you must take before making any moves with your money.

Simply put, when you apply for Medicaid to help pay for long-term care, the state agency will literally "look back" at all your financial records for the previous five years (60 months). What are they looking for? Any assets you gave away, sold on the cheap, or otherwise transferred for less than they were worth.

The government put this rule in place to stop people from handing over their life savings to their kids on a Monday and applying for public assistance on a Tuesday. If they find any of these "uncompensated transfers," you're facing a penalty.

How the Penalty Period Works

The penalty isn't a fine you have to pay back. It’s much worse. It's a period of Medicaid ineligibility where you'll be forced to pay for your own nursing home care out-of-pocket, even though your assets are low enough that you should have qualified.

Here’s how they calculate the penalty period: they take the total value of the gifts or transfers and divide it by the average monthly cost of a nursing home in your state. This number, called the "penalty divisor," is a big one—easily $8,000 to $12,000 a month depending on where you live.

Let's walk through a real-world scenario:

- A father gives his son $120,000 as a gift to help him buy his first house.

- Two years later, the father suffers a stroke and needs to move into a nursing home. He applies for Medicaid to cover the costs.

- The state's average nursing home cost (the penalty divisor) is $10,000.

- Medicaid reviews his finances and immediately spots the $120,000 gift made within the five-year look-back window.

- The math is brutal: $120,000 (gift) ÷ $10,000 (monthly cost) = 12.

- The result: The father is now ineligible for Medicaid coverage for 12 months. Even though he's broke, the family is on the hook for a $120,000 nursing home bill they have no way to pay.

This is how a simple, well-intentioned gift can spark a devastating financial crisis for a family at its most vulnerable moment.

The core lesson of the look-back period is this: a financial decision you make today can directly impact your ability to receive essential care five years from now. Proactive planning isn't just helpful; it's the only way to navigate this rule successfully.

What Kinds of Transfers Trigger the Look-Back?

Medicaid agents are trained to scrutinize a wide range of financial moves, not just big cash gifts. Any action that lowers your net worth without you getting something of equal value in return is a potential red flag.

Here are some of the most common transactions that trigger penalties:

- Cash Gifts: Giving money directly to children, grandchildren, or anyone else.

- Selling Assets Below Market Value: Selling your house to your son for $1 is a classic example. Medicaid will treat the difference between the sale price and the fair market value as a gift.

- Adding a Child's Name to a Deed: This is a big one. Putting a child on the deed to your home can be seen as gifting them half the home's value, instantly creating a huge penalty problem.

- Paying for Someone Else's Expenses: Directly paying a grandchild's college tuition or covering the cost of a family wedding can also be flagged as an improper transfer.

The only way to move assets without triggering a penalty is to use a structured legal strategy. This often involves specific tools, like an irrevocable trust, but even that has to be set up and funded before the five-year clock starts ticking. If you're exploring this path, our guide on how to set up a trust fund breaks down the entire process.

Ultimately, the five-year look-back period makes one thing crystal clear: you have to plan ahead. Waiting until a health crisis hits is often too late, severely limiting your options and putting your family's financial future in jeopardy.

Essential Asset Protection Tools and Strategies

Okay, now that we've covered the financial risks and the all-important Medicaid look-back period, it's time to shift from the "why" to the "how." Let's dive into the specific legal and financial instruments you can use to shield your assets from nursing home costs. Think of this as opening up your toolbox—each tool is designed for a specific job in safeguarding your family's future.

With the median annual cost for a nursing home soaring past $100,000, it's no surprise that families are turning to strategies like irrevocable trusts, strategic gifting, and long-term care insurance. These aren't just abstract concepts; they are practical ways to manage these staggering costs and preserve something for your heirs.

We'll break down the most effective strategies, starting with the long-term planning tools and moving into options for a sudden crisis. This will help you get a real sense of what might be the right fit for you.

Using Irrevocable Trusts for Asset Protection

One of the most powerful and common strategies is the Irrevocable Asset Protection Trust. The name says it all: it's irrevocable. Once you place assets into this type of trust, you're legally giving up control and ownership.

That separation is precisely what makes it work. Since the assets are no longer legally yours, Medicaid can't count them when figuring out your eligibility. This is how you can preserve your home, investments, and savings for your family while still qualifying for the help you need.

But here's the catch: the trust has to be set up and funded outside the five-year look-back period. Transferring assets into an irrevocable trust is considered a gift by Medicaid, which officially starts that 60-month clock. This makes it a fantastic tool for proactive planning, but it's not a last-minute fix.

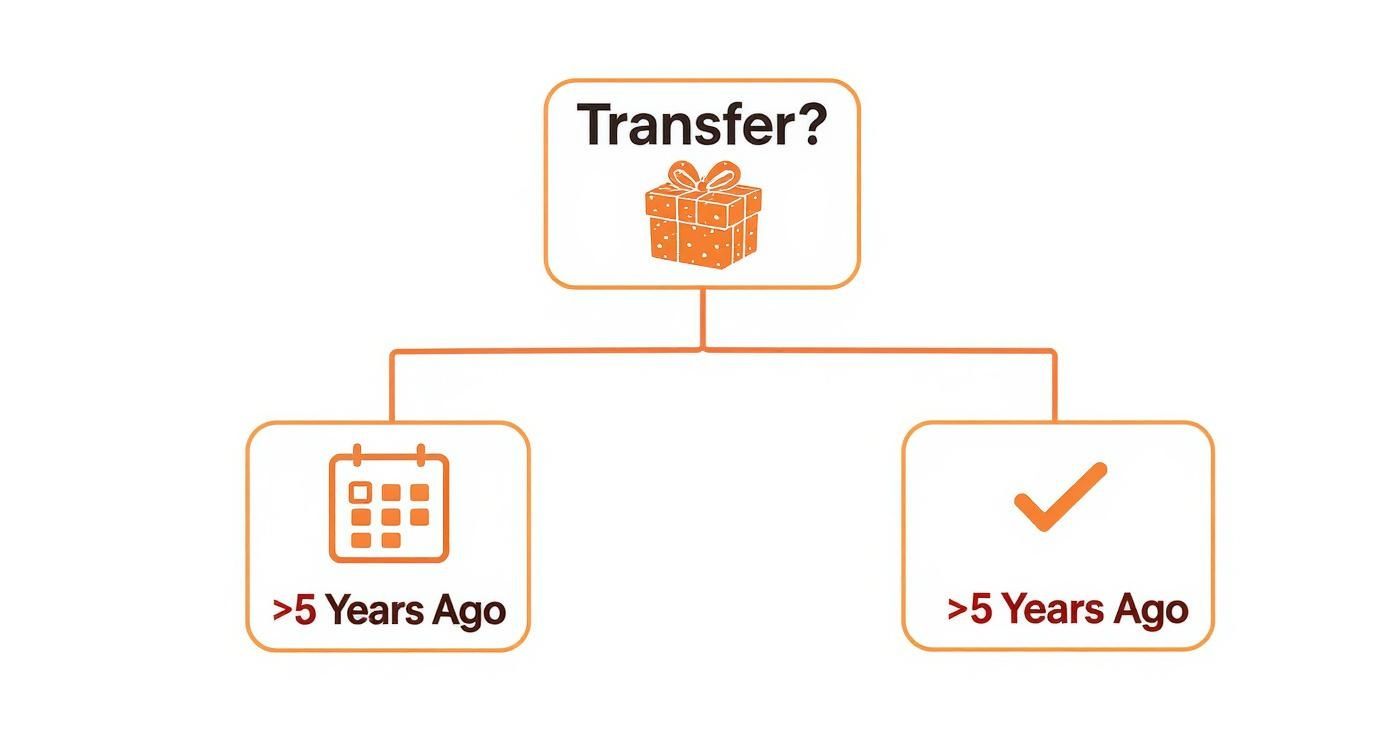

This infographic really drives home the importance of timing when you're thinking about moving assets around for Medicaid planning.

The visual lays out a simple but critical rule: transfers made more than five years before you need care are generally in the clear. Anything moved within that look-back window, however, can create major eligibility headaches.

Long-Term Care Insurance: A Viable Option

While legal structures like trusts are a cornerstone of asset protection, Long-Term Care (LTC) Insurance offers a different kind of shield. It's a specific type of policy designed to cover the costs of nursing homes, assisted living, and even in-home care services.

It works just like any other insurance policy. You pay premiums, and in return, you get a benefit you can draw on when you need it.

LTC insurance is often a great fit for people who are:

- In relatively good health and can pass the medical underwriting.

- In their 50s or early 60s, which is when premiums tend to be more affordable.

- Sitting on significant assets they want to protect but maybe aren't ready to lock them away in an irrevocable trust.

The biggest hurdle is the cost. Premiums can be expensive, and they have a notorious history of increasing over time. Still, for the right person, a solid policy brings incredible peace of mind and can be the very thing that prevents you from having to spend down your life savings.

A key takeaway is that LTC insurance is a pre-planning tool. If you wait until you're older or have health issues, it can become outrageously expensive or you might not be able to get it at all.

Crisis Planning with Medicaid Compliant Annuities

What happens if a health crisis hits out of the blue and you haven't done any of this pre-planning? This is where "crisis planning" comes in, and one of the go-to tools is the Medicaid Compliant Annuity (MCA).

An MCA is a unique financial product that lets you convert a "countable" asset (like a chunk of cash from savings) into a "non-countable" stream of income. You buy the annuity with a single lump-sum payment, and it immediately starts paying you back in fixed monthly installments over a period based on your life expectancy.

Here's how it plays out in the real world:

Imagine Sarah, a single individual, has $150,000 in savings—way over the $2,000 asset limit for Medicaid in most states. She needs nursing home care right now. An elder law attorney might advise her to purchase a $148,000 MCA.

That one move instantly transforms her $150,000 in countable assets into just $2,000 in countable assets plus a new monthly income stream. Boom. She now meets the asset test for Medicaid. The income from the annuity helps cover a portion of her care costs, and the state must be named the primary beneficiary on the annuity. It's a powerful last-minute strategy.

Protections for a Community Spouse

When one spouse needs nursing home care, Medicaid has specific rules to prevent the spouse who stays at home (the "community spouse") from being left with nothing. These are called spousal impoverishment protections, and they are a lifesaver for many couples.

These rules allow the community spouse to keep a certain amount of assets and income that would otherwise have to be spent down. The exact amounts change and vary by state, but they follow federal guidelines.

- Community Spouse Resource Allowance (CSRA): This is the slice of the couple's combined assets the community spouse gets to keep. In 2024, this can be up to $154,140 in many states.

- Monthly Maintenance Needs Allowance (MMNA): This rule lets the at-home spouse keep a certain amount of the couple's total monthly income for living expenses, often up to $3,853.50.

For married couples, these protections are a critical piece of the puzzle. They ensure the healthy spouse has the financial footing to continue living independently and with dignity. If you're looking at how these strategies fit into a bigger picture, you might want to learn more about the role of a retirement plan trust in estate planning, as it offers another layer of security for your family's financial legacy.

Common Mistakes That Can Cost You Everything

Navigating asset protection can feel like walking through a minefield. You can have all the right tools, but knowing where the traps are buried is just as crucial. One well-intentioned but misguided step can unravel years of careful saving, leaving your family's financial future exposed right when it matters most.

Here’s the thing about protecting assets from nursing home costs: it's not intuitive. Many of the "common sense" solutions people try are the very actions that cause the biggest problems down the road. These mistakes often come to light at the worst possible time—when a health crisis hits, forcing quick decisions while emotions are running high.

The Dangers of Adding a Child to Your Deed

One of the most frequent—and dangerous—mistakes we see is a parent adding an adult child's name to the deed of their house or a bank account. It seems so simple, right? A quick way to avoid probate and make sure the house passes smoothly. In reality, it's an incredibly risky move that can backfire spectacularly.

When you add a child's name to your property, you aren't just giving them access. You are legally handing over partial ownership. This means your home is now legally tied to their financial life, along with all its potential bumps and bruises.

Let’s look at a real-world scenario we’ve dealt with:

- A mother adds her son to the deed of her fully paid-off home.

- Two years later, her son causes a serious car accident and is found at fault. The lawsuit judgment is far more than his auto insurance covers.

- Because he is a legal owner of his mother's house, the creditor's attorneys can now slap a lien on the property to satisfy the judgment against him.

Just like that, the mother's home—her biggest asset—is at risk of being sold to pay off her son's debts. This same vulnerability applies to a child’s divorce, bankruptcy, or any other legal trouble they might stumble into.

By trying to simplify things, you can unintentionally expose your life savings to risks you have absolutely no control over. An asset is only as safe as its most vulnerable owner.

Improper Gifting and the Look-Back Trap

We’ve already talked about the five-year look-back period, but the mistake of casual gifting deserves its own warning sign. Writing checks to grandkids for birthdays or helping a child with a down payment are acts of love. But in the eyes of Medicaid, they are uncompensated transfers that start the penalty clock ticking.

The mistake isn't the act of giving. It's the failure to document it correctly or understand the timing. A gift made four years and eleven months before a Medicaid application can trigger a surprisingly long period of ineligibility. The only truly safe way to transfer significant wealth is within a structured legal framework, like a properly drafted and funded irrevocable trust.

The Biggest Mistake: Waiting Too Long

Ultimately, the most devastating mistake of all is simply doing nothing. Far too many families wait until a health crisis forces them into "crisis mode" before they even start thinking about protecting their assets. By then, the five-year look-back period is a massive roadblock, and many of the most powerful strategies are no longer available.

Planning for long-term care isn't a morbid conversation; it's a financial planning conversation. It requires the same proactive mindset you apply to retirement or investing. And the odds are high—about 70% of people turning 65 today will need some form of long-term care in their lifetime.

Trying to DIY your way through this is a recipe for disaster. The rules are wildly complex, vary by state, and change constantly. Relying on online articles alone often leads straight to one of the costly errors we just covered. Working with an experienced elder law attorney isn't an expense; it's the most critical investment you can make to secure your family's future.

Why You Need an Elder Law Attorney on Your Team

Trying to protect your assets from nursing home costs on your own is like trying to do your own complex surgery after reading a medical textbook. You might grasp the basic ideas, but the real world is full of nuances where one small mistake can have permanent, costly consequences. This is not a DIY project.

Building a solid plan requires specialized legal know-how. A general estate planner or your trusted financial advisor, while great at what they do, usually doesn’t have the deep, niche knowledge of Medicaid law. It’s an incredibly complex and constantly changing field. This is precisely where an elder law attorney becomes the most valuable player on your team.

Their entire practice revolves around the unique legal needs of older adults—from long-term care planning and government benefits to guardianship and the tricky rules around estate recovery. They are the specialists who know your state's specific regulations inside and out.

What an Elder Law Attorney Actually Does for You

An elder law attorney is much more than a document-drafter. Think of them as your personal strategist, guiding you through an intricate web of rules to create a plan that is both cohesive and legally sound.

Their role typically includes:

- A Deep Dive into Your Finances: They'll conduct a thorough review of your assets, income, and overall family situation to spot potential vulnerabilities and find hidden opportunities.

- Crafting a Custom Strategy: Based on your specific goals and timeline, they’ll recommend the right tools for the job—whether that’s an Irrevocable Trust, a spousal protection plan, or a crisis strategy involving a specialized annuity.

- Drafting and Executing Legal Documents: This is critical. They ensure that all trusts, deeds, and other legal paperwork are created and funded correctly to hold up under the intense scrutiny of Medicaid law.

- Working with Your Financial Team: A good attorney doesn’t work in a silo. They collaborate with your financial advisor to make sure the legal strategy and the financial strategy are perfectly in sync.

Finding the Right Professional for Your Family

Not all attorneys are created equal, especially in this field. When you're looking for someone to handle something this critical, you have to ask the right questions to make sure you're getting a true specialist.

During your first meeting, don't be shy. Ask them directly about their experience. A great question is, "How many Medicaid asset protection plans do you create each year?" A confident, experienced specialist will have no problem giving you a clear answer and even walking you through case studies similar to your own situation.

This kind of professional guidance is becoming more essential every day. The global need for long-term care is exploding. The World Health Organization estimates that the number of people aged 60 and older will hit approximately 2.1 billion by 2050. This demographic wave makes it vital to get expert help in protecting your assets from nursing home costs. You can discover more insights about global long-term care trends on nber.org.

Ultimately, the cost of hiring an experienced elder law attorney is a small investment when compared to the potential loss of your entire life savings. They provide the expertise, strategy, and peace of mind you need to ensure your plan not only works on paper but actually holds up when your family needs it most. It's about securing your legacy for the generations to come.

Answering Your Key Asset Protection Questions

After digging into the core strategies for shielding your assets from nursing home costs, it's totally normal for a bunch of "what if" questions to pop up. This is where the rubber meets the road—how do these big ideas actually apply to your family?

Let's walk through some of the most common questions and concerns we hear from families every day. We'll give you direct, no-nonsense answers to help you figure out your next steps. These are the things that keep people up at night: their home, their timing, and what this is all going to cost.

Can I Protect My House From The Nursing Home?

For most of us, our home is more than just an asset on a balance sheet; it's where our memories live. So, it's a huge relief to know that yes, you can absolutely take steps to protect it.

The gold standard for protecting your home long-term is to transfer it into a properly structured Irrevocable Trust. Once the house is in the trust and you're past the five-year look-back period, Medicaid no longer considers it your property. It's officially off the table.

But that's not the only way. Depending on your situation, you might have other options:

- Spousal Protections: If you're married and one spouse needs care while the other remains at home (the "community spouse"), the house is generally an exempt asset.

- "Lady Bird" Deeds: In some states, this special type of deed lets you pass your home directly to your heirs upon death while you keep full control during your lifetime. This can help avoid probate and, in some cases, fend off Medicaid estate recovery.

Speaking of which, you have to be aware of Medicaid Estate Recovery. This is a federally required program where the state tries to claw back the money it spent on your care from your estate after you pass away. A house still titled in your name is their number one target. This is precisely why getting an elder law attorney involved is non-negotiable—they know the specific state rules to make sure your home is truly safe.

Is It Ever Too Late To Start Planning?

This question is a big one, and the answer is a mix of good news and a serious warning. While the absolute best time to plan was yesterday, it is almost never too late to take meaningful action.

The most powerful tools, like the Irrevocable Trust, need that five-year runway to be completely effective against the Medicaid look-back period. If you're planning ahead, that's your goal.

But what if a crisis is already knocking on the door? This is where "crisis planning" comes in. Even if a loved one is on the verge of needing nursing home care, a skilled elder law attorney can still protect a surprising amount of the assets. They might use strategies like:

- Purchasing a Medicaid Compliant Annuity, which turns a countable pile of cash into a non-countable income stream.

- Strategically spending down assets on things Medicaid allows, like prepaying for funeral expenses, making essential home repairs, or even buying a new car.

While crisis planning can't save every last penny, it's not uncommon to salvage 50% or more of a family's life savings that would otherwise be completely wiped out by care costs. The trick is to act fast and get professional help immediately.

How Much Does An Asset Protection Plan Cost?

It's completely understandable to worry about legal fees. Many families hold off on getting help because they're afraid of the cost. The truth is, the price of a plan depends on how complex your financial life is and which strategies you need.

A relatively straightforward plan built around an Irrevocable Trust could cost several thousand dollars. If you have multiple properties, business interests, or a more complicated financial picture, the cost will naturally be higher.

But it's critical to frame this cost as an investment, not an expense. Think about it: a single year in a nursing home can easily top $125,000. Spending $5,000 to $15,000 on a rock-solid legal plan that protects hundreds of thousands in assets isn't just a good deal—it's an incredible value. Always ask for a flat-fee arrangement upfront so you know exactly what you're paying for. No surprises.

Will My Standard Living Trust Protect My Assets?

This is a huge, and frankly dangerous, misconception. A standard revocable living trust—which is a fantastic tool for avoiding probate—provides zero protection from nursing home costs.

Why? Because with a revocable trust, you still have total control. You can change it, dissolve it, or pull assets out whenever you want. Since you can access the money, Medicaid considers it fully available to you and will count it against your asset limit.

True asset protection requires you to legally give up ownership and control. That’s the specific job of an Irrevocable Trust. It’s a completely different tool designed for a very different purpose.

At Smart Financial Lifestyle, we believe that making smart financial decisions is about having the right knowledge and guidance. Protecting your family’s legacy from long-term care costs is one of the most important steps you can take. To continue learning and building your financial wisdom, explore more resources at https://smartfinancialifestyle.com.