Losing a spouse is devastating, and the last thing you want to think about is money. It’s emotionally exhausting, and financial paperwork can feel like an impossible weight to carry.

The goal right now isn't to make huge, life-altering decisions. It's about creating a small pocket of order in the middle of chaos. Think of this as financial triage—we’re just going to focus on securing your immediate footing. This will give you the breathing room you need to grieve without the added stress of financial uncertainty.

We'll simply identify the most critical tasks and tackle them one by one. It's all about finding essential information, getting a handle on your immediate cash flow, and making sure you don't miss out on any benefits you're entitled to.

Your First Financial Steps After Losing a Spouse

Locating Essential Documents

Your first job is to become a bit of a detective in your own home. You'll need to track down several key documents to settle your spouse's affairs and claim any benefits. Don't feel pressured to find everything in a single day. Just grab a folder or a box and start collecting items as you find them.

Here’s what you’re looking for:

- Death Certificates: You’ll need multiple certified copies of this. The funeral home can usually help you order them, so don't hesitate to ask.

- Will or Trust Documents: These are the legal papers that outline how assets should be distributed. Check the home office, any safes, or with your family attorney if you have one.

- Social Security Information: You'll need your spouse's Social Security number to notify the administration.

- Financial Account Statements: Gather the most recent statements you can find for bank accounts, investment portfolios, retirement plans (like a 401k or IRA), and credit cards.

- Insurance Policies: Look for any life insurance policies, as well as home, auto, and health insurance.

This search is often where the new reality really sinks in. You might discover you weren't as involved in the day-to-day finances as you thought, and that’s completely normal.

Recent research shows just how common this is. A report from UBS found that 83% of widows run into major roadblocks when they take control of the family finances. To make matters worse, one in four widows admitted they didn't even know where all their partner’s assets were located. This just highlights how important this first step is.

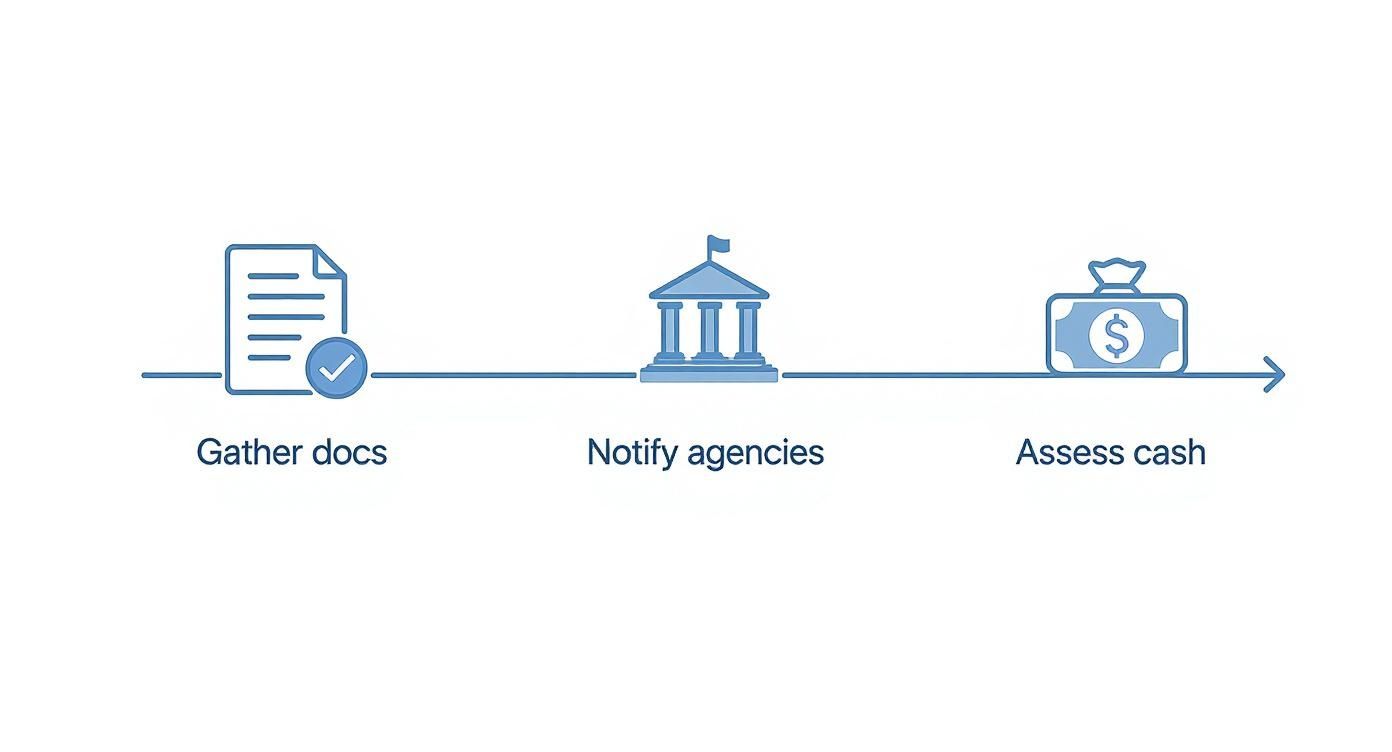

This simple timeline breaks down the three most important priorities for the first few weeks: gathering documents, notifying key agencies, and figuring out your immediate cash flow.

Following a clear path like this helps prevent feeling overwhelmed by breaking a massive task into much smaller, more manageable stages.

To help you get started, here's a simple checklist of the most critical tasks to tackle in the first few weeks. It's designed to be straightforward and actionable.

Immediate Financial Priorities Checklist

| Task | Documents Needed | Key Contact |

|---|---|---|

| Order Death Certificates | Basic personal information | Funeral Home or Vital Records Office |

| Locate Will or Trust | None, just search personal files/safe | Family Attorney (if applicable) |

| Notify Social Security | Spouse's SSN, Certified Death Certificate | Social Security Administration |

| Contact Spouse's Employer | Spouse's Employee ID (if known) | Human Resources (HR) Department |

| Start Life Insurance Claim | Policy Number, Certified Death Certificate | Insurance Company Agent or Customer Service |

| Secure Bank Accounts | Account Numbers, Certified Death Certificate | Local Bank Branch or Customer Service |

| Alert Credit Bureaus | Spouse's SSN, Certified Death Certificate | Equifax, Experian, TransUnion |

This checklist isn't meant to be exhaustive, but it covers the non-negotiable items that need your attention first. Ticking these off will build a solid foundation for everything that comes next.

Notifying Key Organizations

Once you have the death certificate, it’s time to start making some calls and sending some emails. This step is critical for stopping certain payments, starting benefits, and protecting your spouse's identity from potential fraud.

Make a list and work through it systematically. Your key contacts will include:

- Social Security Administration: This should be at the top of your list. Survivor benefits don't start automatically; you have to apply for them. Taking some time to learn how to maximize Social Security benefits is a crucial part of securing your long-term income.

- Your Spouse's Employer: Get in touch with the HR department. You'll need to ask about any final paychecks, accrued vacation time, and any employer-sponsored life insurance or retirement plans.

- Financial Institutions: Notify banks, credit card companies, and investment firms. This helps secure the accounts and starts the process of retitling them into your name.

- Insurance Companies: Start the claims process for any life insurance policies you found.

- Credit Bureaus: Contact Equifax, Experian, and TransUnion to place a fraud alert. This is a simple but powerful step to prevent identity theft.

Remember, it is perfectly okay to ask for help with this. Lean on a trusted family member, a close friend, or your financial advisor to help you make these calls. You do not have to do this all by yourself.

By methodically working through these first steps, you create the foundation you'll need for the next phase of your financial journey. This isn't about having all the answers right now. It's about taking small, deliberate actions that move you toward stability and, eventually, peace of mind.

Creating Your New Financial Foundation

After you’ve handled the most immediate financial fires, it’s time to gently start building a sense of stability. This next phase isn't about making drastic changes or big, scary decisions overnight.

It’s simply about taking a quiet, honest look at your new reality and laying a solid foundation for the future you'll build from here. The first step is to get a clear, realistic picture of your income and expenses.

Understanding Your New Income Streams

Your household income has likely changed, maybe dramatically. The goal right now is just to get a complete picture of all the money coming in each month. Don't even worry about the total yet; just make a list of every single source.

This might include:

- Your Personal Salary: If you're working, this is the most straightforward piece of the puzzle.

- Survivor Benefits: This could be from Social Security or a pension plan. These are crucial new income streams to understand and account for.

- Life Insurance Payouts: If you've received a lump sum, it's very important not to count this as monthly income. For now, just set it aside in a safe place, like a high-yield savings account, while you figure out your plan.

- Investment Income: Think dividends from stocks or interest from savings and bonds.

One of the most sobering realities, particularly for younger widows, is the potential for a significant drop in household income. Research shows that widows under 55 can see their income fall by nearly 23% in the years after their loss. This data isn't meant to scare you—it’s to show why taking the time to build a new, sustainable financial plan is so incredibly important.

Creating a Budget That Breathes

I know, the word "budget" can feel tight and restrictive. But I want you to reframe it as a tool for empowerment. It’s your roadmap. It shows you exactly where your money is going, which gives you a sense of control and helps quiet the anxiety. A budget isn't about deprivation; it's about making conscious choices.

Start by just tracking what you spend for a month or two. Use a simple notebook, a spreadsheet, or an app you like. The goal is just to see where every dollar actually goes.

Example Spending Categories

- Fixed Expenses: Mortgage/rent, property taxes, insurance premiums, car payments.

- Variable Expenses: Groceries, utilities, gas, personal care.

- Discretionary Spending: Dining out, hobbies, travel, entertainment.

Once you have that clear picture, you can start making gentle adjustments. You might notice subscriptions you forgot about or see that you’re spending more on takeout than you realized. Small, conscious changes can create a surprising amount of breathing room. Building these skills is a key part of your journey toward achieving financial independence as a woman.

Building Your Emergency Fund

With a clearer view of your income and spending, the very next priority is your emergency fund. This is your financial safety net, designed to cover those awful, unexpected expenses without knocking you off your feet.

Key Takeaway: Your emergency fund is not an investment; it is insurance. It's cash set aside for true emergencies, like a roof leak, a surprise medical bill, or a job loss.

The goal is to save 3 to 6 months' worth of essential living expenses. Please don't feel pressured to do this all at once. Start small by setting up an automatic transfer—even $50 or $100 a month—from your checking to a separate high-yield savings account.

It’s the consistency that builds momentum and, more importantly, security over time. This fund is your first line of defense, giving you invaluable peace of mind as you move forward.

How to Approach Major Financial Decisions

After the initial chaos of gathering documents and figuring out a new budget, the pressure to make big, life-altering decisions can feel intense. Well-meaning friends and family will likely chime in, suggesting you sell the house, invest the life insurance money, or make other huge changes.

My best advice at this stage? Pause.

Grief is a thick fog that clouds judgment. The emotional and mental exhaustion you're feeling is simply not the right state for making sound, long-term financial choices. Give yourself the grace of time. Most financial advisors I know recommend waiting at least 6 to 12 months before doing anything irreversible.

This isn't about putting things off—it's a strategic buffer. It’s about letting the fog lift so you can approach your financial planning with the clarity you deserve.

Evaluating Your Housing Situation

Your home isn’t just an asset on a spreadsheet. It’s a place filled with memories, a source of comfort, and a deep connection to the life you built with your husband. Deciding whether to stay or move is incredibly personal and goes way beyond the numbers.

Before you make a call, think through both the financial and emotional sides of it:

- The Financial Reality: Can you truly afford the mortgage, property taxes, insurance, and all the surprise maintenance costs on your new, single income? A home that was perfectly affordable for two can quickly become a financial strain for one.

- The Emotional Weight: Does being in the house bring you a sense of stability and comfort? Or does it feel like a constant, painful reminder of what you've lost? There's no right or wrong answer—only what feels right for you.

- Your Future Lifestyle: Think ahead five or ten years. Will this house still fit your life? Consider the physical upkeep, how close you are to family or a support system, and the community you have around you.

Take your time with this. Seriously. Make a pros and cons list. Talk it over with a trusted friend or a financial advisor who can offer an objective view without any emotional pressure. The right path will become much clearer once you've had time to settle into your new normal.

Handling Lump Sum Payouts

Receiving a large sum of money from life insurance, a pension, or a retirement account can feel like both a blessing and a heavy weight. It’s natural to feel an urgent need to "do something" with it right away. Please, resist that urge.

Your first move should be simple and all about security. Park the money in a safe, easy-to-access account, like a high-yield savings or a money market account. This does two critical things:

- It keeps the money protected from the ups and downs of the market while you figure out a plan.

- It keeps the money accessible in case you have immediate needs or an emergency pops up.

Once the money is secure, you can start thinking about what you want it to do for you. Will it supplement your monthly income? Pay off the mortgage? Fund your retirement? Your long-term strategy for these funds will become a cornerstone of your financial plan.

Expert Insight: Be very wary of high-pressure sales pitches for complicated investment products or annuities. A sudden, large inheritance can unfortunately attract opportunistic salespeople. Take all the time you need and work only with a vetted, trusted financial advisor who truly understands your situation.

Navigating Retirement Accounts

Retirement accounts like a 401(k), IRA, or a pension need to be handled with care. As a surviving spouse, you have a few options for a 401(k) or IRA, and each one comes with different tax rules.

- Rollover to Your Own IRA: This is often the most flexible route. It consolidates the money under your control and lets it continue to grow tax-deferred.

- Keep it as an Inherited IRA: This might let you take money out without the 10% early withdrawal penalty if you're under age 59 ½, but the rules can be tricky.

- Take a Lump-Sum Payout: This is almost never a good idea. The entire amount would be hit with income tax, which could easily push you into a much higher tax bracket for the year.

With pensions, your options were likely determined by the choices your spouse made when they set it up. You might be looking at a lump sum or ongoing monthly payments. Getting a handle on these details is crucial for your income planning.

For a deeper dive, you can learn more about calculating the present value of a pension to really understand what this asset means for your financial future. This is one area where talking to a financial professional is absolutely essential to make sure you choose the best option for your long-term security.

Building Your Financial Support Team

Trying to navigate this new financial world on your own can feel incredibly isolating. Please hear this: you are not expected to have all the answers. In fact, the wisest financial decision you can make right now is admitting you don’t have to do this alone.

Assembling a team of trusted professionals isn't a luxury; it's a vital part of finding your footing and securing your peace of mind. These experts are here to provide the objective guidance and specialized knowledge you need to make confident choices for the future.

Identifying Your Key Players

Think of this as building your personal board of directors. Each person brings a different, crucial skill to the table. Together, they give you a complete, 360-degree view of your financial life.

Your core team will likely include a few key roles:

- Certified Financial Planner (CFP): This is your financial quarterback. A good CFP helps you see the big picture—everything from creating a new budget and managing investments to planning for long-term goals like retirement.

- Estate Planning Attorney: This lawyer is essential for updating critical legal documents. They’ll help you revise your will, trusts, and powers of attorney to reflect your new reality as a single individual.

- Certified Public Accountant (CPA): Your tax expert will be invaluable. They can walk you through the tax implications of inheritances, retirement account distributions, and what it means to file as a widow for the first time.

Having these professionals in your corner turns overwhelming complexity into a manageable process. They handle the technical details, which frees you up to focus on healing and making clear-headed decisions.

Finding Advisors Who Truly Understand

Competence is a given, but empathy is non-negotiable. You need advisors who not only know their stuff but also understand the emotional journey you're on. This is more important than many people realize.

A staggering statistic reveals that approximately 70% of widows switch financial advisors within a year of their spouse’s death. Why? It often happens because the previous advisor never built a relationship with them, focusing only on their husband. As research on why women leave their financial advisors shows, this lack of genuine connection is a massive issue.

You deserve an advisor who listens more than they talk and makes you feel heard, respected, and completely understood.

Questions to Ask a Potential Advisor

When you're ready to talk to potential advisors, treat it like an interview. You're the one in charge of hiring the right person for your team. Come prepared with a few questions that cut to the heart of their experience and their approach.

Key Questions to Vet Your Advisor:

- "How much of your practice is dedicated to working with widows?" This is a great way to gauge their direct experience with your specific situation. An advisor who regularly guides women through this transition will already know the unique challenges and opportunities you're facing.

- "Can you describe your process for working with a new client who has recently lost their spouse?" Listen for an answer that emphasizes taking things slowly and educating you along the way—not rushing into big investment decisions.

- "How are you compensated?" You need to understand this from the get-go. Are they "fee-only," meaning you pay them directly (which reduces conflicts of interest)? Or are they "fee-based" and earn commissions by selling you products? Transparency here is absolutely vital.

- "What will our communication look like?" Find out how often they’ll meet with you and how they prefer to keep you in the loop. You want someone proactive and accessible, not someone you have to chase down for answers.

Your Gut Feeling Matters: Beyond the answers to these questions, pay close attention to how you feel during the conversation. Do you feel comfortable asking what might seem like a "silly" question? Do you feel rushed or talked down to? Trust your intuition. It's rarely wrong.

Finding the right people is one of the most powerful steps you can take. It transforms a journey of uncertainty into a path with clear, confident, and supported steps forward.

Designing Your Future and Legacy

After dedicating so much time and emotional energy to navigating the immediate aftermath of your loss, you can now start to gently shift your focus. It’s a move from just getting through the day to intentionally designing what comes next.

This is a deeply healing and empowering part of the process. It’s where your financial plan stops being about crisis management and starts being about aligning your money with your life's purpose. We're building a future that provides not just security, but genuine fulfillment in your next chapter.

Investing for Your New Goals

Your financial goals have almost certainly changed, and that means your investment strategy needs to change with them. The approach you and your husband built as a couple was designed for a different life; it may no longer fit your individual timeline or comfort with risk.

The key now is to create an investment plan that supports your vision for the future. Do you dream of a quiet, comfortable retirement? Or maybe you want to travel the world? Perhaps being in a strong position to help your children or grandchildren is what matters most to you now.

A Note on Risk: It's completely normal to feel more cautious with money right now. A good financial advisor understands this. They'll work with you to build a diversified portfolio aimed at steady, long-term growth—not chasing aggressive, stressful gains. The goal is peace of mind, not sleepless nights.

Think of your investment portfolio as a tool to help you reach those goals. It will likely include a mix of different assets to provide both growth and stability.

- Stocks and Mutual Funds: These offer the potential for long-term growth to help your money outpace inflation over time.

- Bonds: Generally more stable than stocks, bonds can provide a source of regular, predictable income.

- Real Estate: This could be your primary home or other properties that generate rental income.

The right mix is completely unique to you. This is where the guidance of your financial team is invaluable—they can help translate your life goals into a tangible, practical investment strategy.

Reclaiming Your Estate Plan

You are now the sole steward of your family’s assets, which makes it absolutely critical to update your own estate plan. The will and other documents you created with your husband were designed for a life you shared, and they no longer reflect your reality or your individual wishes.

This isn’t just about deciding who gets what. It’s about ensuring your affairs are managed exactly as you want them to be, protecting your loved ones from confusion and conflict down the road.

An estate plan is a collection of legal documents that work together. Here's a look at the key pieces you'll need to review with an attorney.

Your New Estate Plan Checklist

| Document | Purpose | Key Considerations for Update |

|---|---|---|

| Last Will & Testament | Directs the distribution of your assets after your death. | You'll need to designate a new executor (who manages your estate) and clearly name your beneficiaries. |

| Durable Power of Attorney | Appoints someone to make financial decisions for you if you become unable. | You must name a new agent, as your husband was likely the primary person designated before. |

| Healthcare Directive | Outlines your wishes for medical treatment and end-of-life care. | Appoint a new healthcare proxy to make medical decisions if you cannot communicate them yourself. |

| Living Trust (if applicable) | Can help your estate avoid the lengthy and public process of probate court. | Review and update the trustee and beneficiaries to align with your current wishes. |

Working with an experienced estate planning attorney on this is non-negotiable. They will make sure your documents are legally sound and truly reflect your intentions, giving you the final say in how your legacy unfolds.

Living a Life of Purpose

Ultimately, financial planning for a widow is about so much more than managing money. It’s about using your financial resources to build a life that feels authentic and purposeful to you, right now.

This is your opportunity to redefine what wealth means on your own terms. For you, it might mean:

- Creating a secure retirement that allows you to live comfortably without financial worry.

- Traveling and pursuing new hobbies that bring you joy.

- Supporting your family by helping with a grandchild’s education or a child’s down payment.

- Building a charitable legacy by giving to causes that were meaningful to both of you.

When you approach it this way, financial planning transforms from a daunting chore into an act of self-care and empowerment. You are taking control, making your own choices, and building a foundation for a future filled with security, purpose, and peace.

A Few Common Questions We Hear

Navigating your finances after losing your husband brings up countless questions, big and small. Let’s walk through some of the most common concerns widows face, with clear, direct answers to help you find your footing.

How Soon Should I Make Big Financial Decisions?

If I could give just one piece of advice here, it would be this: wait. Financial experts almost universally advise waiting at least six to twelve months before making any significant, irreversible financial moves.

This isn’t about procrastination; it’s a strategic pause. This includes decisions like selling your home, making huge investments with life insurance proceeds, or giving large financial gifts to your kids.

The time immediately following a loss is a fog of emotion. That’s not the headspace for making choices that will affect the rest of your life. Use this time to focus on the immediate steps—gathering documents, figuring out a new budget, and just getting a handle on your cash flow. Once the picture is clearer and you've had time to breathe, you’ll be in a much better position to make sound judgments.

Am I Entitled to My Spouse’s Social Security Benefits?

Yes, in most cases, you are entitled to survivor benefits from Social Security. The amount you'll get depends on a few things, like your age, your husband's earnings record, and whether you're still caring for minor children.

You can typically start receiving these survivor benefits as early as age 60 (or 50 if you are disabled). But be aware, the benefit amount goes up if you can wait until your full retirement age to claim them.

It's so important to contact the Social Security Administration as soon as you can after your spouse's death. These benefits do not start automatically. An agent can walk you through your specific options and help you figure out the best timing to maximize what you receive.

Applying promptly ensures you don’t miss out on payments you’re entitled to.

What Should I Do with a Life Insurance Payout?

A life insurance payout can feel like a huge weight of responsibility landing on your shoulders at the worst possible time. The absolute best first step is to simply put the money somewhere safe, accessible, and liquid.

Think about these options for now:

- A high-yield savings account: This keeps the money secure while earning a bit of interest, and you can get to it whenever you need it.

- A money market account: This works much like a savings account, offering safety and easy access.

This simple action protects the funds while you take the time you need to build a real financial plan with an advisor you trust. Don't let anyone pressure you into immediately investing it in complicated products. Your long-term goals—like paying off the mortgage, funding retirement, or supplementing your income—will eventually guide the strategy. Just resist making any quick moves until you have a clear plan you feel confident about.

At Smart Financial Lifestyle, we believe in making smart financial decisions that create security and peace of mind for generations. Paul Mauro’s 50+ years of experience have shown that with the right guidance, women in transition can build a future of confidence and purpose. To learn more about how we can support your journey, visit us at https://smartfinancialifestyle.com.