Liquid Net Worth vs Net Worth Explained

The real difference between liquid net worth vs net worth is simple. Total net worth gives you the full financial picture, while liquid net worth shows your immediate financial flexibility. It’s a bit like this: think of total net worth as the full value of your house, and liquid net worth as the cash you have on hand for an emergency repair. Both numbers are critical for smart financial planning, but they tell you very different things.

Defining Your Financial Standing

To really get a handle on your financial position, you have to look beyond a single number. Your total net worth offers a complete snapshot of your financial health by subtracting everything you owe (liabilities) from everything you own (assets). This calculation includes long-term assets like your home, retirement accounts, and business investments.

Your liquid net worth, on the other hand, is a crucial, real-time measure of your financial resilience. It zeroes in on assets that you could turn into cash quickly—we’re talking within a few days—without taking a major hit on their value. This means cash in checking and savings accounts, money market funds, and publicly traded stocks. Essentially, it tells you what you could get your hands on immediately in a crisis.

Your total net worth is a measure of wealth you’ve built over time, reflecting long-term success. Your liquid net worth is a measure of your immediate security, reflecting your ability to handle whatever life throws your way.

Understanding the Components

The fundamental distinction comes down to what gets included in each calculation. Net worth considers both liquid and illiquid assets, like real estate and business ownership, giving you that broad view of your accumulated wealth. But liquid net worth is much more restrictive, focusing only on assets that offer immediate financial access. If you want to dig deeper into how these assets are categorized, you can read more about the net worth vs liquid net worth distinctions on Indeed.com.

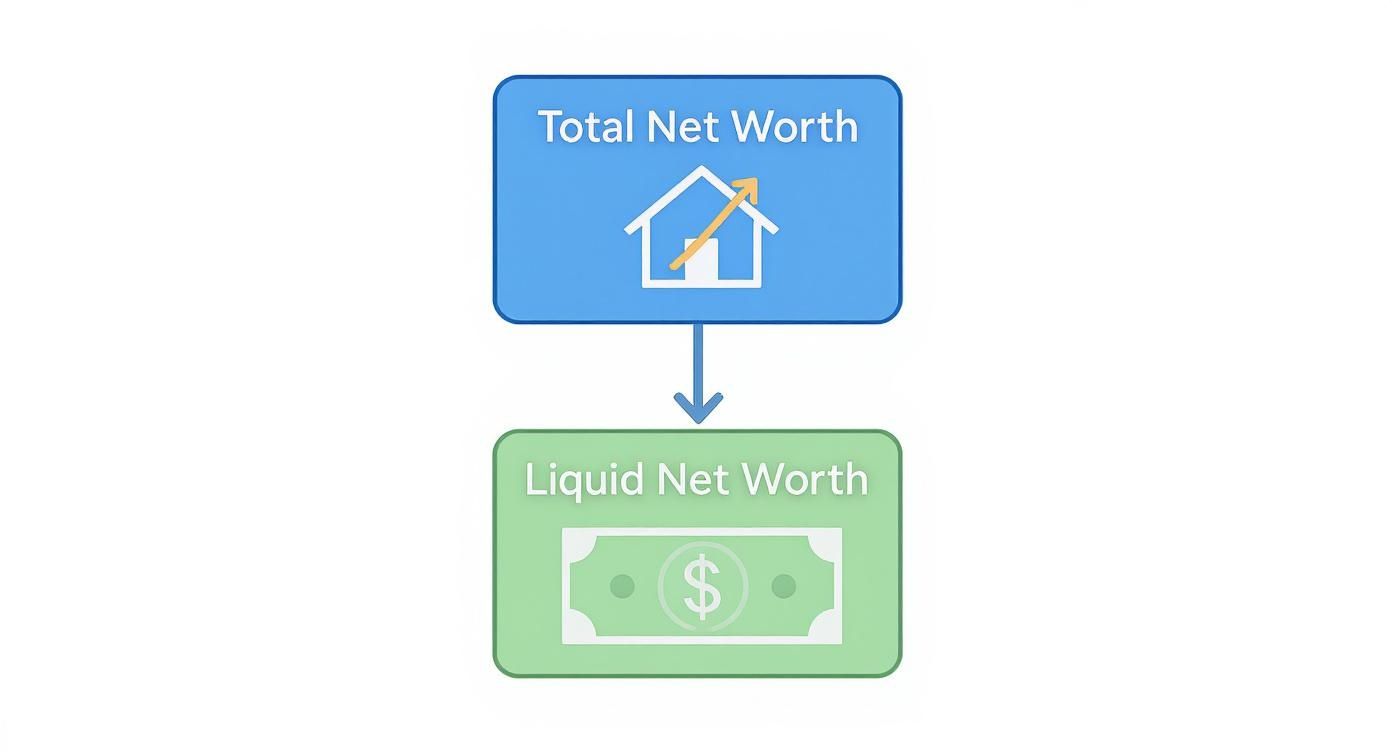

This hierarchy diagram really helps visualize how liquid net worth is just one piece of your total net worth.

As you can see, all your liquid assets are part of your total net worth, but not all of your total net worth is liquid.

Quick Comparison Net Worth vs Liquid Net Worth

To make the differences crystal clear, let's break them down side-by-side. This table gives a quick summary of what each metric is used for and what it includes.

| Metric | Total Net Worth | Liquid Net Worth |

|---|---|---|

| Primary Use | Measures long-term wealth accumulation and retirement readiness. | Measures short-term financial stability and emergency preparedness. |

| Includes | All assets (real estate, retirement accounts, investments, cash). | Only assets easily converted to cash (checking, savings, stocks). |

| Calculation | (All Assets) - (All Liabilities) | (Liquid Assets) - (Short-Term Liabilities) |

| Flexibility | Low; selling assets like a home or business can take months. | High; assets can be accessed within days without penalty. |

Ultimately, both numbers serve a purpose. Total net worth is your report card for long-term wealth building, while liquid net worth is your first line of defense against unexpected financial shocks. Knowing both gives you a much more complete and actionable understanding of your financial life.

How to Accurately Calculate Each Metric

Knowing the difference between liquid net worth and total net worth is one thing, but running the numbers correctly is a whole different ballgame. To get a clear picture, you have to be methodical, listing out every single asset and liability. Think of it as a financial check-up—it shows you the true state of your long-term wealth and your short-term stability.

For instance, household wealth in the U.S. has bounced back significantly since the Great Recession, with median wealth jumping 21.2% between 2016 and 2019. But here's the catch: a lot of that growth is tied up in illiquid assets like real estate. This can mask the reality of a family's day-to-day financial flexibility. If you want to dive deeper, you can explore the full research on household wealth trends.

Let's walk through the math with a fictional example, Alex, to see how these numbers play out in the real world.

Calculating Alex’s Total Net Worth

Total net worth gives you that big-picture, 30,000-foot view of your financial standing. The formula is as simple as it gets: Total Assets - Total Liabilities = Total Net Worth.

First, Alex needs to list everything they own, both liquid and illiquid:

- Home Value: $500,000

- 401(k) Retirement Account: $200,000

- Brokerage Account (Stocks/Bonds): $50,000

- Savings Account: $20,000

- Checking Account: $5,000

- Car Value: $25,000

Next up, Alex has to tally all outstanding debts:

- Mortgage Balance: $300,000

- Student Loan Debt: $40,000

- Car Loan: $10,000

Now for the easy part. Alex’s total net worth is:

$800,000 (Assets) - $350,000 (Liabilities) = $450,000

This figure shows the overall wealth Alex has built. Getting aggressive with liabilities is one of the best ways to grow this number. For more on that, check out our guide on how to pay off debt faster without making more money.

Calculating Alex’s Liquid Net Worth

Okay, now let’s shift gears to liquid net worth, which is all about immediate financial access. The formula here is: Liquid Assets - Short-Term Liabilities = Liquid Net Worth. While you typically only include current liabilities like credit card debt, we'll use total liabilities here to get a more conservative, worst-case-scenario estimate.

For this calculation, we only count assets that can be turned into cash quickly and without a penalty:

- Brokerage Account (Stocks/Bonds): $50,000

- Savings Account: $20,000

- Checking Account: $5,000

Notice what’s missing? The house, the car, and the 401(k). Those are all illiquid.

So, Alex’s liquid net worth calculation looks like this:

$75,000 (Liquid Assets) - $350,000 (Liabilities) = -$275,000

A crucial point of confusion is how to treat retirement funds. A 401(k) is absolutely part of your total net worth, but it is not part of your liquid net worth. Cashing it out early means facing steep penalties and taxes, making it anything but accessible for immediate, penalty-free use.

The massive difference—a $450,000 total net worth versus a -$275,000 liquid net worth—is exactly why you need to track both. Alex has built solid long-term wealth but doesn't have much short-term wiggle room. An unexpected emergency could mean taking on even more debt.

Why This Distinction Shapes Your Financial Strategy

Getting the calculations down is one thing, but the real magic happens when you know how to use these two numbers to shape your financial life. The difference between liquid net worth vs net worth isn't just an accounting detail; it’s a practical guide for how you handle risk, jump on opportunities, and build a secure future. Each number tells a different story and serves a unique purpose.

Your liquid net worth is your financial first-aid kit. It's the number that tells you whether a surprise car repair, an unexpected medical bill, or a sudden job loss is a minor speed bump or a full-blown crisis. Having strong liquidity gives you options and breathing room, letting you handle life's curveballs without being forced to sell long-term investments at a bad time or rack up high-interest debt.

On the flip side, your total net worth is your long-term compass. This is the big picture, the benchmark for your most ambitious goals—like a comfortable retirement, funding a child's education, or leaving a meaningful legacy. It’s the scorecard for your wealth-building efforts over years, and even decades.

The Asset-Rich, Cash-Poor Dilemma

The importance of this distinction really hits home when you look at a classic financial trap: being "asset-rich, cash-poor."

Picture a retiree who owns their home free and clear and has a healthy 401(k), giving them a total net worth of over $1 million. On paper, they look fantastic. But if their checking account only has a few thousand dollars, their liquid net worth is practically on life support.

What does this feel like day-to-day?

- Financial Stress: A sudden $5,000 roof leak could force them to sell stocks at a loss or take out an expensive loan.

- Missed Opportunities: They can't easily help a grandchild with a down payment or invest in a promising opportunity that requires cash now.

- Reduced Quality of Life: Despite their high net worth, their daily spending is tight, creating a constant low hum of financial anxiety.

Now, consider a young professional with a more modest $200,000 total net worth, but $50,000 of it is sitting in liquid savings and brokerage accounts. This person has far more immediate freedom and security. They can handle emergencies with confidence and make life choices without being handcuffed by a lack of accessible cash.

A high total net worth provides long-term security, but a healthy liquid net worth provides immediate peace of mind. A successful financial strategy requires nurturing both.

Ultimately, your liquid net worth dictates your ability to act, while your total net worth reflects the value of what you’ve built. The true art of financial planning lies in balancing both, ensuring you have the resources you need for today and the wealth you want for tomorrow.

Applying These Metrics at Different Life Stages

Knowing the math behind liquid net worth vs. net worth is one thing, but making that knowledge work for you is where the real power lies. The right balance between cash on hand and long-term wealth isn’t a set-it-and-forget-it number. It shifts dramatically as your career, family, and goals evolve. What works for a young professional just starting out is completely different from the strategy a retiree needs to protect their life's savings.

This is why context is everything in financial planning. The distribution of assets in the United States really drives this point home. Data shows the top 1% of households hold about $14.8 trillion in assets, but much of that is often tied up in illiquid holdings like businesses and real estate. It’s a clear example of how a high net worth on paper doesn't always mean you have easy access to cash.

Let’s walk through how your financial focus should shift by looking at three common life stages.

The Mid-Career Professional

If you're in the middle of your career, you’re likely juggling a mortgage, raising a family, and trying to save for retirement. Your main focus is on building total net worth, but you can't afford to ignore liquidity. The name of the game is asset accumulation—growing your retirement accounts, chipping away at your mortgage to build home equity, and investing for the long haul.

At the same time, a healthy liquid net worth is non-negotiable. It’s the financial firewall that protects you from a sudden job loss or a major home repair without forcing you to sell off investments and derail your long-term plans.

- Primary Goal: Aggressively grow total net worth through smart investments and paying down debt.

- Liquidity's Role: Maintain a robust emergency fund that covers 6-9 months of living expenses. This protects your long-term assets from being liquidated at the wrong time.

- Actionable Tip: Max out your contributions to retirement accounts like a 401(k) or IRA. While you’re doing that, set up automatic monthly transfers to a high-yield savings account to steadily build your liquid reserves.

The Retiree

Once you hit retirement, the script completely flips. The focus shifts from accumulating wealth to preserving it and creating a steady income stream. This makes liquid net worth the top priority. The biggest challenge for a retiree is generating enough cash to cover living expenses without being forced to sell assets—like stocks or real estate—during a market downturn.

Having enough liquidity gives you the breathing room to navigate volatile markets and handle unexpected costs, especially for healthcare, without chipping away at your core retirement portfolio. A solid cash cushion is what lets you sleep at night.

For retirees, liquidity isn't just an emergency fund; it's a strategic tool. It gives you control over when and how you tap into your lifelong savings, helping you preserve your total net worth for the long haul.

The Entrepreneur or Business Owner

Entrepreneurs live in a world of financial uncertainty. With income that can swing wildly and a constant need to reinvest in the business, a strong liquid net worth is absolutely critical. Their total net worth might look impressive on paper because it’s tied up in business equity, but cash flow is what actually keeps the lights on.

For a business owner, liquidity serves a dual purpose: it’s both a personal safety net and a business contingency fund. It provides the capital to get through slow seasons, jump on growth opportunities, or cover unexpected operational costs without having to take on expensive debt. To see how your own finances stack up, you can explore our guide to average net worth by age and percentile.

As you move through life, your financial priorities will naturally change. The key is to recognize these shifts and adjust your strategy accordingly. The table below offers a simple guide to how your focus might evolve depending on where you are in your journey.

Financial Priorities Based on Life Stage

| Life Stage/Persona | Primary Focus (Liquid vs. Total) | Key Financial Goal | Actionable Tip |

|---|---|---|---|

| Early Career Professional | Liquid Net Worth | Build a 3-6 month emergency fund. | Automate savings into a high-yield account before focusing on aggressive investing. |

| Mid-Career Family Steward | Total Net Worth (with strong liquidity) | Grow investments and reduce debt (mortgage). | Max out retirement accounts while maintaining a 6-9 month emergency fund. |

| Entrepreneur | Liquid Net Worth | Ensure business and personal cash flow stability. | Maintain separate personal and business emergency funds, each covering at least 6 months. |

| Pre-Retiree (5-10 years out) | Shifting focus toward Liquid Net Worth | De-risk portfolio and build a cash buffer for retirement. | Start building a "cash bucket" to cover the first 1-2 years of retirement expenses. |

| Retiree | Liquid Net Worth | Preserve capital and generate reliable income. | Maintain 2-3 years of living expenses in cash and short-term bonds to avoid selling assets in a down market. |

Ultimately, understanding the interplay between liquid and total net worth allows you to make more intentional decisions. It’s not about picking one over the other; it’s about finding the right balance for your specific situation to build a resilient and prosperous financial life.

Strategies to Grow Both Financial Metrics

Knowing the difference between liquid net worth vs. net worth is a great start, but the real work begins when you take deliberate steps to grow both. A solid financial plan builds long-term wealth without giving up the short-term flexibility that helps you sleep at night.

The good news is that these two goals aren't at odds with each other. In fact, strengthening one often helps the other. Growing your total net worth is the long game. It boils down to two simple levers: making your assets grow and making your debts shrink.

This means making consistent contributions to retirement accounts like a 401(k) or IRA, letting compound growth work its magic over decades. At the same time, getting aggressive with high-interest debt—think credit cards or personal loans—gives your net worth a direct boost by chipping away at what you owe.

Enhancing Your Liquid Net Worth

While your total net worth builds quietly in the background, shoring up your liquidity requires a more hands-on approach. The absolute cornerstone here is a solid emergency fund. It's your financial first-aid kit for life's inevitable surprises.

Here are a few actionable steps you can take to build up your cash reserves:

- Open a High-Yield Savings Account: These accounts pay much better interest rates than the savings account at your local brick-and-mortar bank, helping your cash grow faster without any extra effort.

- Automate Your Savings: This is a classic for a reason. Set up automatic transfers from your checking to your high-yield savings each week or month. "Paying yourself first" is the easiest way to build that liquid cushion.

- Invest in Liquid Assets: Cash is king, but you can also look at investments that are easy to sell, like index funds or ETFs in a standard brokerage account. They offer growth potential while still being pretty easy to access.

A well-built emergency fund is truly the foundation of financial security. For a step-by-step walkthrough, check out our emergency fund checklist with 8 must-have steps.

Nurturing your liquid net worth isn't just about saving; it's about creating financial freedom. It gives you the power to handle emergencies, seize opportunities, and make life decisions from a position of strength, not desperation.

Striking the Right Balance

The real magic happens when you pursue both goals in harmony. Think about it: aggressively paying down your mortgage builds home equity (boosting total net worth) and frees up monthly cash flow that you can then funnel into savings (boosting liquid net worth).

Likewise, once your emergency fund is fully stocked, any extra cash can be put to work in investments geared toward long-term growth.

Ultimately, a smart strategy takes care of your needs today while building the future you want. By taking small, consistent steps to grow your assets, shrink your liabilities, and build a healthy cash reserve, you create a resilient financial foundation that can weather any storm while steadily growing your wealth for years to come.

Answering Your Key Questions

As you start wrapping your head around the difference between liquid net worth and total net worth, a few common questions always seem to pop up. Let's tackle them head-on so you can apply these concepts with total confidence.

Should My 401k Be Included in My Liquid Net Worth?

Nope. A 401(k) or any similar retirement account is considered an illiquid asset, so it only belongs in your total net worth calculation.

Sure, you can often take a loan or make an early withdrawal, but that move usually comes with a nasty sting of penalties and taxes. Liquid net worth is all about the cash you can get your hands on quickly without losing a big chunk of it in the process.

How Often Should I Calculate These Figures?

Think of it this way: calculate your total net worth once or twice a year. That’s the perfect rhythm for tracking your progress on big, long-term goals like retirement.

Your liquid net worth, on the other hand, deserves a closer look—maybe every quarter or even every month. This is your immediate financial cushion. Keeping a close eye on it helps you stay on top of your budget, make sure your emergency fund is healthy, and react quickly to any of life's curveballs.

Can You Have a High Total Net Worth but Low Liquidity?

Absolutely, and it’s a surprisingly common trap to fall into. It’s often called being "asset rich, cash poor." Someone might own valuable real estate, have a massive retirement portfolio, or run a successful business—all things that pump up their total net worth.

But if they have very little cash in the bank or investments they can sell in a pinch, their liquid net worth could be dangerously low. This is a precarious spot to be in. It makes handling an unexpected medical bill or a major home repair incredibly difficult without having to sell off a long-term asset or take on more debt.

Being transparent about both liquid and illiquid assets is crucial, especially during major life transitions like divorce. Hiding or misrepresenting assets can lead to severe legal and financial penalties, as courts prioritize a fair and complete picture of a couple's finances.

What Is a Good Liquid Net Worth to Aim For?

There’s no magic number here, because your ideal liquid net worth really depends on your lifestyle, income, and who relies on you. A solid rule of thumb is to have enough liquid assets to cover 3 to 6 months of essential living expenses. That’s your core emergency fund.

But if your income is unpredictable, you’re already retired, or you have more dependents, aiming for a bigger buffer of 9 to 12 months of expenses is a much safer bet. The goal is to have enough liquidity to give you peace of mind without letting too much cash sit on the sidelines, missing out on long-term growth.

At Smart Financial Lifestyle, we believe that understanding these financial nuances empowers you to build a secure future for yourself and your loved ones. Our approach combines practical wisdom with timeless principles to help you make smarter financial decisions. To learn more about building a resilient financial life, visit us at https://smartfinancialifestyle.com.