How to Reduce Taxes in Retirement for Good

When it comes to your taxes in retirement, the name of the game is proactive income management. The goal is to shift from just saving for retirement to strategically planning for a tax-efficient one.

This really boils down to using smart withdrawals from your different accounts and timing your Roth conversions just right. It’s all about controlling your taxable income so you—not the IRS—get to keep more of your hard-earned money.

Building Your Low-Tax Retirement Blueprint

Think of this as your playbook for getting ahead of retirement taxes. We want to move you from a reactive position, where you just get a tax bill and pay it, to a proactive one where you’re the architect of a lower-tax future. Getting that mindset right is the foundation for everything we’ll cover.

A lot of new retirees get blindsided by what’s known as the “tax torpedo.” This is a nasty surprise that happens when a small bump in your income—maybe from a pension or a Required Minimum Distribution (RMD)—pushes you into a much higher effective tax bracket.

It can cause a painful ripple effect, suddenly making more of your Social Security benefits taxable and even jacking up your Medicare premiums.

Understanding Your Financial Toolbox

Dodging that torpedo starts with knowing the tools you have at your disposal. You likely have three main types of accounts, and each one gets taxed differently. The order you pull money from them is absolutely critical.

- Tax-Deferred Accounts (Traditional 401(k)s, IRAs): This is the money you got a tax break on when you put it in. It grew without being taxed along the way, but now you’ll pay ordinary income tax on every single dollar you take out.

- Tax-Free Accounts (Roth 401(k)s, Roth IRAs): You funded these with after-tax money, which means all your qualified withdrawals in retirement are 100% tax-free. This is your golden ticket.

- Taxable Accounts (Brokerage Accounts): You also funded this with after-tax dollars. The good news here is you only pay capital gains tax on the growth when you sell an investment, which is often at a lower rate than income tax.

It’s a huge mistake to think of these accounts as interchangeable. A common blunder is tapping into tax-deferred accounts first, which can needlessly inflate your taxable income right at the start of your retirement.

The most powerful lever you can pull in retirement is your control over your annual income. By strategically choosing which accounts to draw from and when to convert funds to a Roth, you can essentially set your own tax rate year after year.

Instead of waiting for massive RMDs to dictate your financial life, a well-built plan lets you smooth out your tax bill over decades. This guide will give you that blueprint. We’ll start with the smartest way to sequence your withdrawals and then layer in more advanced tactics like Roth conversions and charitable giving.

The goal is simple: help you build a durable, tax-efficient retirement that supports your family and your legacy for years to come.

Before we dive into the step-by-step strategies, it helps to see the big picture. All the tactics we'll discuss fall into one of three core pillars.

Three Pillars of Retirement Tax Reduction

| Strategy | Primary Goal | Best For |

|---|---|---|

| Tax-Aware Withdrawals | Control annual taxable income by tapping accounts in a specific order (Taxable -> Tax-Deferred -> Tax-Free). | Everyone, but especially those in the early years of retirement before RMDs begin. |

| Strategic Roth Conversions | Move money from tax-deferred to tax-free accounts during low-income years to reduce future RMDs and create a source of tax-free cash. | Retirees with large traditional IRA/401(k) balances who anticipate higher tax rates in the future. |

| Timing & Gifting Tactics | Optimize Social Security, manage RMDs with charitable donations, and use tax-efficient investments to minimize the overall tax bite. | Retirees who are charitably inclined or need to fine-tune their income to stay below key tax thresholds. |

Understanding these three pillars is the key. Every piece of advice in this guide is designed to help you master one or more of these foundational strategies to create a truly resilient financial plan.

Mastering Your Retirement Withdrawal Sequence

One of the biggest financial decisions you'll make in retirement has nothing to do with what you spend, but where you pull the money from. The order you tap into your different retirement accounts can massively change your lifetime tax bill. It can turn a huge tax headache into a major long-term win.

Getting this sequence right is the bedrock of a low-tax retirement.

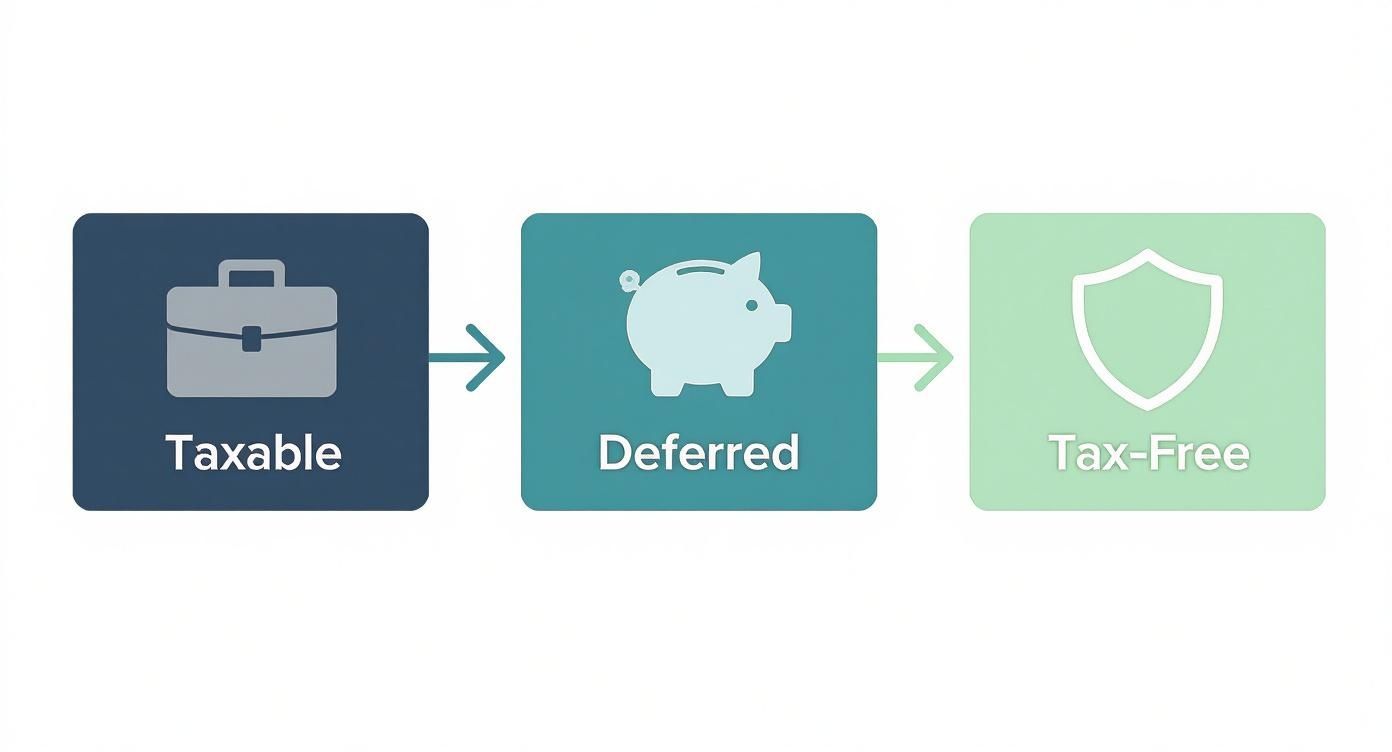

Now, the conventional wisdom usually points to a simple three-step path: use your taxable accounts first, then your tax-deferred ones, and save your tax-free Roth accounts for last. That’s not bad advice, but a truly savvy retirement plan is much more dynamic and flexible, adapting to your specific tax situation each year.

This graphic gives you a quick look at the standard withdrawal order most people follow.

It lays out that classic path, starting with taxable brokerage funds, moving to tax-deferred IRAs and 401(k)s, and keeping the Roth accounts in your back pocket.

Start with Your Taxable Brokerage Accounts

For most retirees, tapping into taxable brokerage accounts first is a powerful opening move. You’ve already paid income tax on the money you invested, so when you sell, you only owe capital gains tax on the growth. That’s a huge advantage, especially in your first few years of retirement.

Even better, in years where your total taxable income is low, you might just qualify for the 0% long-term capital gains tax rate. This is a golden opportunity to sell some appreciated investments and generate cash for living expenses without paying a dime in federal tax on those gains. All while your other retirement accounts keep growing untouched.

Think of your taxable account as a bridge. It can fund the early years of your retirement, allowing your tax-deferred and tax-free accounts to compound for longer, which is a key component of the best retirement withdrawal strategies available.

This approach gives you a ton of control over your taxable income before Social Security benefits and Required Minimum Distributions (RMDs) start to complicate the picture.

Strategically Tap Tax-Deferred Accounts Next

Once you've spent down some of your taxable money—or when it makes sense from a tax-bracket perspective—it’s time to start taking distributions from your traditional IRAs and 401(k)s. Remember, every dollar you pull from these accounts is taxed as ordinary income, so you have to be careful.

The real key here is to withdraw just enough to cover your spending needs without accidentally bumping yourself into a higher tax bracket.

Here's how this plays out in the real world:

- The Situation: A married couple, both 64, needs $60,000 for their annual expenses. They don't have a pension and haven't started taking Social Security yet.

- The Strategy: First, they sell investments from their brokerage account, realizing $30,000 in long-term capital gains. Because they have no other income, these gains fall squarely within the 0% capital gains bracket.

- The Smart Move: For the other $30,000 they need, they pull from their traditional IRA. This withdrawal is small enough to keep them in the lowest federal income tax bracket.

This blended approach lets them live comfortably while keeping their tax bill incredibly low. It’s a perfect illustration of how to actively manage your income from one year to the next.

Preserve Your Tax-Free Roth Accounts for Last

Your Roth IRA is your ultimate weapon against taxes in retirement. Because every qualified withdrawal is 100% tax-free, it usually makes sense to let this account grow for as long as you possibly can. Keeping your Roth funds on the sidelines gives you a few major advantages.

- A Tax-Free Safety Net: It’s the perfect source of cash for large, unexpected expenses—like a new roof or a big medical bill—without creating a massive tax bomb in a single year.

- RMD Management: Unlike traditional IRAs, Roth IRAs have no Required Minimum Distributions. This money can continue to grow, tax-free, for your entire life.

- Legacy Planning: Roth IRAs are a fantastic tool for passing wealth to your kids or grandkids. They can inherit it and enjoy tax-free withdrawals, making it an incredibly efficient way to leave a legacy.

By saving your Roth for later in retirement, you create a powerful buffer against rising tax rates, unexpected costs, and the income spikes that RMDs can cause. This disciplined sequence gives you flexibility and control, making sure you keep more of your hard-earned money right where it belongs—with you and your family.

Unlocking the Power of a Roth Conversion

Of all the strategies out there for cutting your tax bill in retirement, the Roth conversion is easily one of the most powerful. It’s a pretty straightforward move: you take money from a pre-tax account, like your traditional IRA or 401(k), and move it into a post-tax Roth IRA.

Now, you do have to pay income tax on the amount you convert today. But in return, that money grows and can be withdrawn completely tax-free for the rest of your life. It's all about paying Uncle Sam on your own terms.

Instead of waiting for the government to force your hand with Required Minimum Distributions (RMDs), you get to decide when to recognize that income. The big idea is to pay taxes now, at a rate you can control, to avoid getting hit with a much bigger tax bill down the road.

Timing Your Conversions in the Gap Years

The real magic of a Roth conversion is all in the timing. For most retirees, there's a sweet spot known as the "gap years"—that period after you've stopped working but before you start taking Social Security and RMDs.

During these years, your taxable income is often the lowest it will ever be in retirement. This is a golden opportunity.

You can strategically convert chunks of your traditional IRA each year, essentially "filling up" the lower tax brackets (like the 12% and 22% brackets) with the conversion income. By doing this systematically, you're chipping away at your future RMD problem without ever pushing yourself into a painfully high tax bracket. This is at the heart of the pretax contribution vs Roth debate; you're picking your tax battleground.

A Roth Conversion in Action

Let’s look at a real-world example with a couple, Mark and Susan, both age 63. They just retired with a combined $1.2 million in their traditional IRAs and plan to hold off on Social Security until they turn 70.

- Their Goal: Slash their future RMDs. At their current balance, those distributions, combined with Social Security, would push them into a much higher tax bracket.

- The Plan: Over the next seven years (from age 63 to 69), they'll systematically convert funds from their traditional IRAs over to Roth IRAs.

- The Execution: Every year, they convert just enough to fill up the 22% federal tax bracket without spilling over into the next one. For a married couple filing jointly in 2024, that means converting around $120,000 annually.

By the time they turn 70, Mark and Susan will have moved over $800,000 into their Roth accounts. Sure, they paid taxes along the way, but they did it at a manageable rate. Now, their remaining traditional IRA balance is much smaller, which means their future RMDs won't create a tax nightmare.

This disciplined approach is precisely why Roth conversions have become such a go-to strategy for retirees. Financial experts will tell you that mapping out conversions year by year—projecting your income, withdrawals, and taxes for each stage of retirement—is the key. It smooths out your tax obligations, keeping them low and predictable instead of letting them spike when you least expect it.

Common Pitfalls to Avoid

As powerful as they are, Roth conversions have some critical rules and potential traps. Knowing what they are is the key to making this strategy work for you, not against you.

- Pay Taxes with Outside Funds: This is a big one. Always use money from a taxable brokerage or savings account to pay the tax bill on the conversion. If you use money from the conversion itself, you’re shrinking the amount that actually makes it into the Roth, which defeats a lot of the purpose.

- Respect the Five-Year Rule: Any money you convert has to stay in the Roth IRA for five years before you can withdraw the converted principal tax-free and penalty-free. There's a separate five-year clock for each conversion you make. This is crucial for anyone under 59½, but it’s a good rule of thumb for all retirees to plan around.

- Watch for Medicare Surcharges (IRMAA): A large conversion can spike your modified adjusted gross income (MAGI). That sudden income jump could trigger higher Medicare Part B and D premiums two years down the line. Make sure your conversion amount doesn't accidentally push you over those IRMAA income thresholds.

By carefully planning your conversions, you can transform a future tax headache into a smart, strategic decision today. It gives you far more control over your financial destiny in retirement.

Untangling RMDs and Social Security Taxes

The moment you turn 73, the retirement game changes, whether you’re ready or not. That’s the age when the IRS requires you to start taking Required Minimum Distributions (RMDs) from your tax-deferred retirement accounts, like a traditional IRA or 401(k). If you’ve spent decades saving diligently, this can feel like a sudden tax trap you didn't see coming.

Those mandatory withdrawals are taxed as ordinary income, and a large RMD can easily bump you into a higher tax bracket. This sets off a chain reaction, potentially making more of your Social Security benefits taxable and even jacking up your Medicare premiums. The trick is to get ahead of this, not just react when the bill comes due.

Shrink Future RMDs Before They Start

By far the best way to defuse the RMD tax bomb is to shrink the account balance the IRS uses for its calculation. This is where the Roth conversion strategy we talked about earlier really shines. Every dollar you convert to a Roth IRA in your 60s is one less dollar in your traditional IRA that will be subject to RMDs in your 70s.

Think of it like strategically draining a reservoir before the floodgates are forced open. You’re choosing to pay taxes on your own terms during your lower-income “gap years” between retiring and starting Social Security. Doing this reduces the principal used to calculate your mandatory withdrawal, giving you far more control.

A smaller traditional IRA balance directly translates to a smaller future RMD. This simple cause-and-effect is the foundation of a proactive retirement tax plan, turning a future obligation into a current opportunity.

This move doesn't just lower your RMDs; it also builds a powerful, tax-free war chest in your Roth IRA. That gives you incredible flexibility for big expenses down the road without triggering a tax avalanche.

Give Smarter With a Qualified Charitable Distribution

For retirees who are charitably inclined, there's a uniquely powerful tool that becomes available starting at age 70½. It’s called a Qualified Charitable Distribution (QCD), and it lets you donate up to $105,000 each year directly from your traditional IRA to a qualified charity.

This is a fantastic strategy for a couple of reasons:

- It Satisfies Your RMD: Once you reach RMD age, any amount you donate via a QCD can count toward that year's mandatory withdrawal.

- It’s Not Taxable Income: This is the best part. The money goes straight to the charity and is completely excluded from your adjusted gross income (AGI). You follow the withdrawal rule without adding a single penny to your taxable income.

This is a huge win-win. You get to support a cause you're passionate about while pulling off a brilliant tax-reduction maneuver. A lower AGI can also lead to other great benefits, like reducing taxes on your Social Security and keeping your Medicare premiums from creeping up.

Navigating the Social Security and RMD Collision

The final piece of this puzzle is seeing how your RMDs and Social Security benefits will collide. For many retirees, this is where the "tax torpedo" strikes. A large RMD landing on top of your Social Security check can suddenly cause up to 85% of your benefits to become taxable.

This is exactly why timing your Social Security claim is so important. By delaying your benefits until age 70, you not only lock in a larger monthly check for life but also open up a wider window in your 60s for those strategic Roth conversions. You can methodically shrink your IRA balances before your Social Security income starts, preventing that future income spike.

These two income streams have to be managed together. To get the full picture, you can learn more about how to maximize Social Security benefits in our detailed guide, which breaks down the long-term impact of your claiming decision.

By treating RMDs and Social Security as interconnected parts of one financial plan, you can make them work in harmony. It's this careful coordination that lets you keep control over your taxable income and build a truly resilient, low-tax retirement.

Advanced Tax Reduction Strategies to Consider

Once you've got a handle on withdrawals and conversions, a few other powerful tactics can really fine-tune your financial plan. Think of these as the next layer of efficiency—ways to protect your portfolio, plan for your legacy, and even manage future healthcare costs with some incredible tax advantages.

![]()

These moves take a bit more foresight, but the long-term savings can be substantial. It’s about shifting your mindset from just managing income to strategically optimizing every corner of your financial life.

Turn Market Losses into Tax Wins

Even in a down market, there’s a silver lining. It’s a strategy called tax-loss harvesting, and it’s something you can do in your regular taxable brokerage accounts. The idea is to intentionally sell investments that have lost value.

Now, this isn't about ditching a good investment forever. It's about crystallizing that "paper loss" so you can use it to your advantage.

That loss becomes a valuable tool. You can use it to cancel out capital gains from other, more successful investments you’ve sold during the year. And if your losses are bigger than your gains? You can use up to $3,000 of the excess to wipe out some of your ordinary income, which is often taxed at a much higher rate. Any leftover losses can be carried forward to future years. It's a savvy way to find a positive in an otherwise negative market turn.

The Overlooked Power of a Health Savings Account

I’ve heard a Health Savings Account (HSA) called the ultimate retirement account, and honestly, it’s hard to argue. It offers a rare triple-tax advantage that you just can't find anywhere else.

- Tax-Deductible Contributions: The money you put in is tax-deductible, which lowers your taxable income right now.

- Tax-Free Growth: Your HSA funds can be invested, and they grow completely tax-free.

- Tax-Free Withdrawals: You can pull money out tax-free at any time to pay for qualified medical expenses.

Once you hit 65, the HSA gets even better. You can withdraw money for any reason—not just medical costs. Those non-medical withdrawals are just taxed like a traditional IRA. This makes it a fantastic backup retirement account for healthcare and anything else life throws your way.

Consider Your State Tax Burden

Federal taxes are only half the story. Where you live in retirement can have a massive impact on your tax bill, since state income, sales, and property taxes are all over the map.

Moving to a more tax-friendly state is obviously a huge decision, but for some people, it can be a total game-changer. Right now, seven states have no state income tax at all. Others give retirees special breaks on Social Security and pension income.

Before you start packing boxes, you have to look at the whole picture. A state with no income tax might have sky-high property or sales taxes that could wipe out your savings. It’s all about finding the right balance for your financial situation and the lifestyle you want.

The decision to move is deeply personal, but it’s one of the most powerful levers you can pull to shrink your lifetime tax burden. It’s definitely worth exploring as part of a comprehensive retirement plan.

Planning for Your Legacy and Beyond

Thinking about retirement taxes often bleeds into how you want to pass your wealth to the next generation. With smart gifting and estate planning, you can make sure your legacy goes to your loved ones, not Uncle Sam.

A simple starting point is the annual gift exclusion. You can gift up to a certain amount to as many people as you want each year without even having to file a gift tax return. It's a straightforward way to reduce the size of your taxable estate while helping family and friends now.

For those with more assets, trusts can offer more control and tax efficiency, ensuring your wealth is managed and distributed exactly how you envision.

The world is also getting smaller when it comes to retirement planning. Tax-friendly international destinations are more accessible than ever. In fact, a recent report found that 61% of countries across 44 evaluated programs offer specific tax benefits for retirees. The 2025 Global Retirement Report even highlights that half of these countries have no wealth or inheritance tax for new residents. It’s a big step, but for some, international relocation is becoming a serious strategic move. You can dive deeper by reading the full report on 2025 global retirement findings.

Your Retirement Tax Questions Answered

Digging into the world of retirement taxes can feel like a chore, but getting a handle on a few key strategies is what separates a good retirement plan from a great one. Big-ticket items like Roth conversions and withdrawal sequencing always bring up questions, and getting clear answers is how you build the confidence to act.

This section tackles the most common questions we hear from retirees just like you. Think of it as your go-to cheat sheet for making smarter moves with your money.

When Is the Best Time to Do a Roth Conversion?

The perfect time for a Roth conversion is almost always during your "low-income" years. For most folks, this golden window opens right after they stop working but before they start claiming Social Security and taking Required Minimum Distributions (RMDs). We often call these the "gap years."

In this period, your taxable income is likely the lowest it will be in your entire adult life. That creates a unique opportunity to move money from a traditional IRA over to a Roth IRA and pay the conversion tax at a much lower marginal rate than you would in the future.

Other great times to consider a conversion include:

- Years with large deductions: If you have a year with unusually high medical expenses or other big deductions, that can help offset the income from a conversion and shrink your tax bill.

- Down market years: When the stock market is down, so is your account balance. This means you can convert more shares for the same tax cost, setting yourself up for more tax-free growth when the market recovers.

The core strategy here is to strategically "fill up" the lower tax brackets (like the 10%, 12%, and 22% brackets) with conversion income each year. It’s a methodical way to chip away at your future RMD problem without accidentally pushing yourself into a higher tax bracket.

Can I Use a Qualified Charitable Distribution to Offset My RMD?

Yes, absolutely. For charitably-minded retirees aged 70½ and older, the Qualified Charitable Distribution (QCD) is one of the most powerful tax-saving tools out there. It’s a true win-win for you and the causes you support.

A QCD lets you donate up to $105,000 per year (for 2024) directly from your traditional IRA to a qualified charity. This move packs a powerful one-two punch. First, the amount you give through a QCD counts toward satisfying your RMD for the year.

Second—and this is the big one—the amount you donate is completely excluded from your adjusted gross income (AGI). You get to fulfill your RMD obligation without adding a single dollar to your taxable income for the year.

Lowering your AGI is a huge win. It can have other positive ripple effects, such as reducing the portion of your Social Security benefits that are subject to tax and potentially lowering your Medicare Part B and D premiums.

This makes a QCD a much more tax-savvy way to give than just writing a check and taking the standard charitable deduction.

How Does Delaying Social Security Help Reduce My Lifetime Taxes?

Holding off on claiming Social Security is a cornerstone of a tax-smart retirement plan, and its benefits go way beyond just getting a bigger monthly check. For every year you wait past your full retirement age (up to age 70), your benefit grows by about 8%. That’s a guaranteed return you just can't find anywhere else.

From a tax perspective, delaying creates a larger window of those low-income "gap years." This gives you maximum flexibility to pull off strategic Roth conversions at much lower tax rates.

Think of it this way: by drawing down your traditional IRA and 401(k) balances through conversions before Social Security starts, you're proactively shrinking the future RMDs that would eventually get stacked right on top of your Social Security income.

This approach helps you control your taxable income over your entire retirement. You avoid the dreaded "tax torpedo," where the combined hit of RMDs and a big Social Security check shoves you into a higher tax bracket and makes more of your benefits taxable. It's all about smoothing out your income over decades instead of letting it spike when you’re in your 70s and 80s.

At Smart Financial Lifestyle, we believe that making smart financial decisions is the key to building wealth and redefining the American dream. These strategies are more than just numbers—they are about creating security, peace of mind, and a lasting legacy for your family. To learn more about building a resilient financial future, visit us at https://smartfinancialifestyle.com.