How Is Social Security Amount Determined a Clear Guide to Your Benefits

Your Social Security check isn't some number pulled out of a hat—it’s a direct reflection of your life's work. The Social Security Administration (SSA) has a pretty straightforward, three-step method to figure out what you'll get. They pinpoint your 35 highest-earning years, adjust them for inflation, average them out, and then run that number through a special formula.

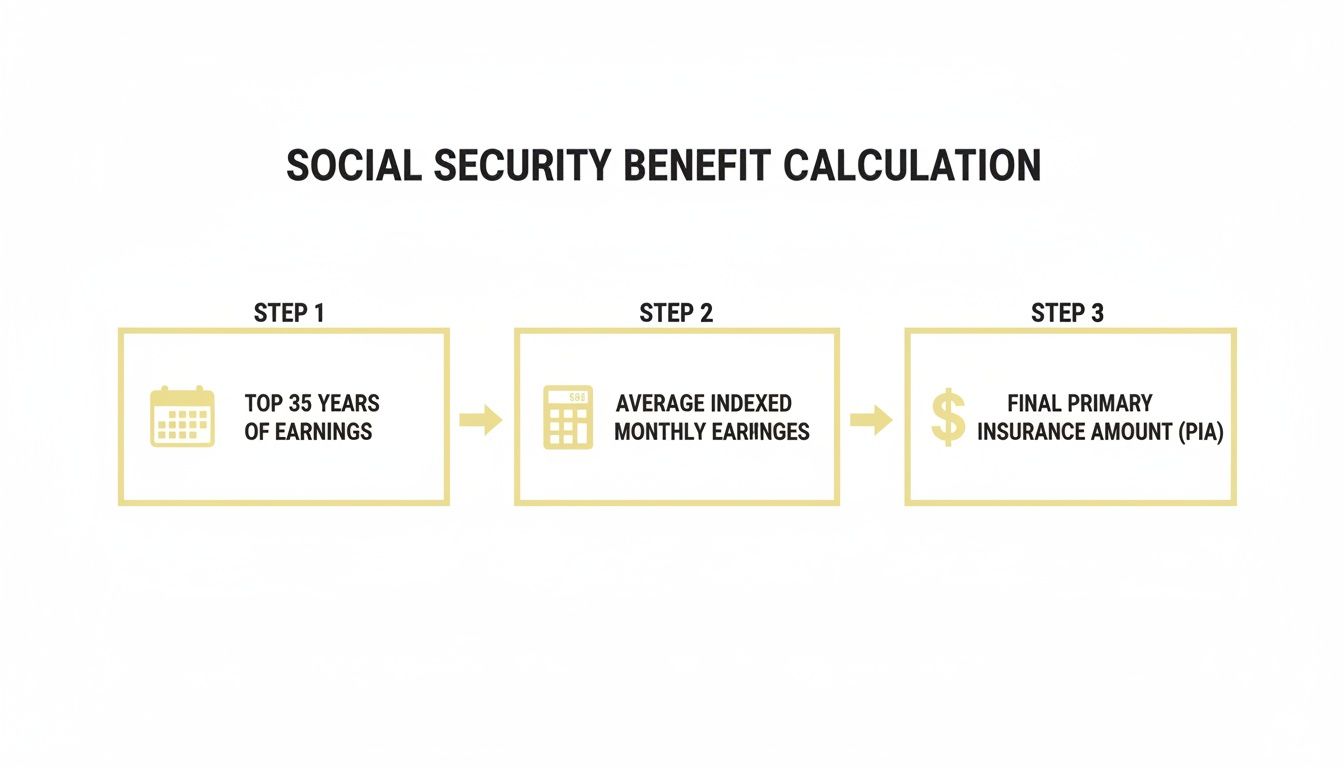

Your Social Security Benefit Calculation at a Glance

Getting a handle on how your benefit amount is determined is the first real step toward making smart financial moves for your family. It strips away the mystery and lets you see exactly how your career choices translate into retirement income. The whole system is built right on top of your work history, zeroing in on your most productive years.

It might sound complicated, but it really just boils down to three core ideas that turn decades of work into a reliable monthly check. Think of it as the SSA creating a financial snapshot based on everything you've contributed over the years. Each year of earnings is a building block, and the goal is to get a clear picture of your average income.

This visual helps break down the calculation into its three essential parts, showing how your earnings history ultimately becomes your final benefit amount.

This flowchart simplifies that journey from your work history to your retirement check, really driving home the importance of your 35 highest-earning years in the whole process.

The Three Core Steps

To make sure things are fair and predictable for everyone, the SSA uses the same consistent method for every single retiree. Each step builds on the one before it, slowly refining the numbers until it lands on your personal benefit amount.

Let's walk through the foundational calculation process.

The Social Security Administration has a consistent, three-part system for calculating every single benefit check. Understanding this process is key to seeing how your work history translates into retirement income.

| Step | What It Means for You | Why It Matters for Your Retirement |

|---|---|---|

| 1. Pinpoint Your Top 35 Years | The SSA takes your entire work history, adjusts each year's earnings for inflation, and then pulls out the 35 years you made the most money. This levels the playing field, making sure the $40,000 you earned in 1995 is valued fairly against the $70,000 you earned last year. | This step directly rewards career growth and consistent work. Every high-earning year you add can bump up your average and, ultimately, your final benefit. |

| 2. Calculate Your AIME | Next, they add up those 35 inflation-adjusted years and divide the total by 420 (the number of months in 35 years). The result is your Average Indexed Monthly Earnings (AIME). | The AIME is the key number that represents your average lifetime earnings. A higher AIME is the foundation for a larger monthly benefit. |

| 3. Determine Your PIA | Finally, your AIME is plugged into a weighted formula that uses specific income thresholds called "bend points." This formula calculates your Primary Insurance Amount (PIA). | Your PIA is the benefit you're entitled to receive at your full retirement age. Everything else—like claiming early or late—is an adjustment to this baseline number. |

This process ensures that every benefit is calculated based on the same fundamental principles, providing a predictable foundation for your retirement planning.

This three-step process—indexing your earnings, calculating your AIME, and determining your PIA—forms the bedrock of every Social Security calculation. Getting comfortable with these ideas is crucial before you can start exploring smart strategies to maximize Social Security benefits for your family.

How Your Lifetime Earnings Become Your AIME

So, how does the Social Security Administration (SSA) take a lifetime of work and boil it down to a single number that defines your benefit? It all starts with a crucial first step: calculating your Average Indexed Monthly Earnings, or AIME.

Think of your career earnings as the building blocks for your retirement house. Every year you work and pay into the system, you're adding another brick to the foundation. The stronger those bricks—meaning, the higher your earnings—the more solid that foundation will be for your family's future.

But the SSA doesn't just look at the raw dollar amounts you made over the decades. They have a clever way of making sure everything is valued fairly.

This process ensures that the income you earned early in your career gets the same weight as what you earned more recently.

Leveling the Playing Field with Wage Indexing

First up, the SSA uses a method called wage indexing. It might sound technical, but the idea is simple: it translates your past income into today's dollars. This is all about fairness. Earning $30,000 back in 1990 meant something very different for a family budget than earning $30,000 today.

The government applies an indexing factor to your earnings for every year up until you turn 60. This adjustment brings all those past wages up to a modern value, creating a level playing field across your entire work history. Without this step, your earlier years of lower earnings would unfairly drag down your average.

Identifying Your 35 Highest Years

Once all your past earnings are updated to today's values, the SSA zeroes in on your 35 highest-earning years. This is a really important part of the calculation. Let's be honest, nobody's career is a perfectly straight line upwards. You might have taken time off to raise kids, switched careers, or had a few lean years.

The system is designed to focus on your most productive periods. It doesn't matter if those top-earning years were back-to-back or spread out over four decades. The SSA simply plucks out the 35 best indexed-earnings numbers and lines them up for the next step.

This is where career consistency really pays off. As we often tell our clients, hitting that 35-year mark is a huge milestone for maximizing your retirement income. It makes sure your benefit is calculated based on a full career of your best work, not dragged down by years with zero earnings.

"Social Security benefits are calculated based on your 35 highest-earning years, adjusted for inflation to ensure fairness across decades...Zeros count if you have fewer than 35 years, potentially slashing your benefit—statistics show workers with exactly 35 years average 20-30% higher monthly payments than those with gaps."

Understanding this piece of the puzzle can empower you to make smarter financial choices that truly strengthen your retirement outlook. You can explore more expert insights on how this calculation impacts family financial planning.

Calculating the Final Average

Okay, so the SSA has your top 35 indexed earning years lined up. From here, the math is actually pretty straightforward. They add up the earnings from those 35 years to get one big lifetime total.

Then, they divide that grand total by 420—which is simply the number of months in 35 years (35 x 12 = 420).

The number that pops out is your Average Indexed Monthly Earnings (AIME). This single figure represents your average monthly income over your highest-paid working years, all adjusted for wage growth. It's the bedrock of your Social Security benefit, and every other part of the calculation—from bend points to claiming age—starts right here.

Understanding the PIA Formula and Bend Points

Once we have your Average Indexed Monthly Earnings (AIME), the Social Security Administration does one final calculation to lock in your core benefit. This last step turns your AIME into your Primary Insurance Amount (PIA). If there's one number to know in your retirement plan, this is it—the PIA is the full monthly benefit you’re due at your Full Retirement Age (FRA).

But how do you get from an average earnings number to that final benefit amount? It's not a simple percentage. The SSA uses a special, weighted formula designed to give lower-income workers a stronger safety net while still rewarding folks with higher lifetime earnings.

This is where a concept called "bend points" comes into play.

What Are Social Security Bend Points?

The easiest way to think about bend points is to compare them to tax brackets, but in reverse. Instead of figuring out how much you owe on different chunks of your income, bend points determine how much of your past earnings get replaced in your benefit check.

It's a progressive system. That means the formula replaces a much higher percentage of earnings for lower-income folks than it does for high earners.

For anyone turning 62 in 2024, the formula works across three tiers:

- It replaces 90% of the first $1,174 of your AIME.

- It replaces 32% of your AIME between $1,174 and $7,078.

- It replaces 15% of any AIME amount over $7,078.

Those dollar figures—$1,174 and $7,078—are the bend points for 2024. They change every year with inflation, but the three percentages (90%, 32%, and 15%) always stay the same. This tiered structure is the secret sauce that ensures Social Security provides a stable foundation for all retirees.

The SSA publishes these figures every year, and this visual flowchart breaks down exactly how it all works.

This process confirms how the benefit formula adjusts over time with national wage growth, making sure the math stays relevant for each new wave of retirees.

A Practical Example of the PIA Formula

Let's walk through how this works for a real person. We'll use a retiree named Sarah who has an AIME of $4,500.

Here's how the SSA would calculate her PIA using the 2024 bend points:

-

First Tier (90%): The formula takes the first $1,174 of her AIME and multiplies it by 90%.

- $1,174 x 0.90 = $1,056.60

-

Second Tier (32%): Next, we look at the chunk of her AIME that falls between the two bend points.

- $4,500 (her AIME) - $1,174 (first bend point) = $3,326

- That amount gets multiplied by 32%: $3,326 x 0.32 = $1,064.32

-

Third Tier (15%): Sarah's AIME of $4,500 is below the top bend point of $7,078, so she doesn't have any earnings in this tier.

- $0 x 0.15 = $0

To get her final PIA, we just add up the dollar amounts from each tier.

$1,056.60 (from the 90% tier) + $1,064.32 (from the 32% tier) = $2,120.92

So, Sarah's Primary Insurance Amount is $2,120.92. This is the exact monthly benefit she'll receive if she starts taking Social Security right at her full retirement age. It’s this multi-step formula that turns a lifetime of earnings into a predictable retirement check.

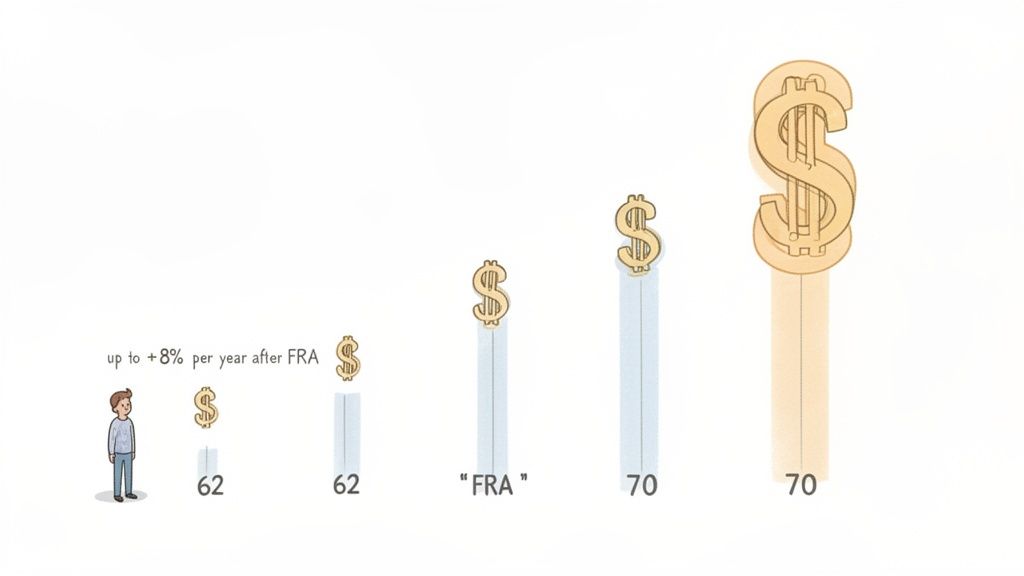

How Your Claiming Age Transforms Your Benefit

Your Primary Insurance Amount (PIA) is the foundation of your Social Security, built from a lifetime of your hard work. But the actual dollar amount that lands in your bank account each month boils down to one of the biggest financial decisions you'll ever make: when you choose to start taking benefits.

This single choice has the power to permanently increase or decrease every single check you receive for the rest of your life. It's a pivotal moment in your family's financial story.

Think of your PIA as the baseline—the 100% benefit you’ve earned. Your claiming age acts like a volume knob on that baseline. Claiming early gives you a smaller stream of income, but you get it sooner. Waiting gives you a much larger, more powerful income stream later on.

The Three Key Milestones

Your path to claiming benefits is marked by three critical ages. Each one represents a different strategy with its own set of trade-offs for your family's financial future.

- Age 62 (The Earliest Option): You can start your benefits as early as age 62. The appeal is obvious—getting cash flow right away. But this comes at a steep price. Claiming early permanently cuts your monthly benefit by up to 30% compared to waiting for your Full Retirement Age.

- Full Retirement Age (The Baseline): This is the magic number where you are entitled to 100% of your earned PIA. Your Full Retirement Age (FRA) is somewhere between 66 and 67, depending on the year you were born. Reaching this milestone is the key to getting your full, unreduced benefit.

- Age 70 (The Maximum Benefit): For every single year you delay claiming past your FRA, your benefit grows by a remarkable 8%. These bonuses, known as delayed retirement credits, stop adding up at age 70. Waiting until this point maximizes your monthly payment for life.

This choice isn't just about chasing the biggest number; it's about matching your benefits to your family's long-term needs. The difference in your monthly income between claiming at 62 versus 70 can be more than 75%.

To see how this plays out, let's look at a quick comparison. Imagine your full benefit (PIA) at age 67 is $2,000 per month. Here's what your monthly check would look like depending on when you claim.

Claiming Age vs. Monthly Benefit Amount (Example PIA of $2,000)

| Claiming Age | Percentage of PIA Received | Example Monthly Benefit | Lifetime Payout by Age 85 |

|---|---|---|---|

| 62 | 70% | $1,400 | $386,400 |

| 67 (FRA) | 100% | $2,000 | $432,000 |

| 70 | 124% | $2,480 | $446,400 |

As you can see, waiting not only increases your monthly income significantly but can also lead to a larger total payout over your lifetime, providing a stronger financial safety net.

A Story of Strategic Patience

Let's look at David and Maria, a couple planning their next chapter. David's PIA was calculated to be $2,200 a month at his FRA of 67. He was tempted to claim at 62 to leave a demanding job, which would have meant taking a reduced benefit of $1,540 per month (a 30% cut).

But after talking about their real goals—traveling to see the grandkids and making sure Maria would be secure if he passed away first—they made a different plan. David decided to work part-time for a few more years and delayed his Social Security until he turned 70.

By waiting, his benefit grew by 24% above his PIA. His new monthly benefit became $2,728. That’s a staggering $1,188 more each month than if he’d claimed at 62. This decision not only gave them more income for their retirement together but also massively increased the survivor benefit Maria would receive, giving them both lasting peace of mind.

Why Your Claiming Age Matters So Much

The timing of your Social Security claim is more than a math problem; it's a reflection of your family's priorities. It directly shapes the size of your monthly check, the potential survivor benefits for your spouse, and your overall financial resilience against inflation and unexpected costs down the road.

A larger, delayed benefit acts as a powerful form of longevity insurance, helping ensure you don't outlive your resources. And since the rules are always evolving, staying informed is critical. You can learn more about how the goalposts might move by reading our guide on whether the official retirement age is going up.

Special Circumstances That Can Change Your Payout

While your earnings record and when you decide to claim are the cornerstones of your Social Security benefit, life isn't always a straight line. Social Security has a handful of special rules designed to handle these unique situations, making sure the system can adapt to different family dynamics and career paths.

Getting a handle on these rules is a huge part of making smart financial choices, especially when you're planning for your whole family. It ensures the final calculation reflects your complete story, not just a simplified version. These rules cover everything from supporting a spouse to accounting for a career spent outside the Social Security system.

Spousal and Survivor Benefits

One of the most powerful provisions for families is the availability of spousal and survivor benefits. Think of these rules as a crucial financial safety net, making sure a lower-earning or non-working spouse isn't left in a tough spot during retirement or after a partner's passing.

Here’s a quick rundown of how they generally work:

- Spousal Benefits: If you're married, you might be able to claim a benefit based on your spouse's work record. This can be up to 50% of your spouse's full retirement age benefit, though the amount is reduced if you claim before reaching your own full retirement age. This is a game-changer if your own retirement benefit is much lower.

- Survivor Benefits: If your spouse passes away, you could be eligible to receive a survivor benefit. This can be as much as 100% of what your deceased spouse was receiving or would have been entitled to at their full retirement age.

These benefits can even extend to divorced spouses, as long as the marriage lasted 10 years or more and you haven't remarried. These options can get complicated, but they're incredibly valuable. You can get a clearer picture by exploring different Social Security strategies for married couples.

The Windfall Elimination Provision and Government Pension Offset

Some careers—especially in state and local government jobs like teaching or law enforcement—don’t pay into the Social Security system. Instead, those employees contribute to a separate pension plan. When those same people also have enough years working in the private sector to qualify for Social Security, a couple of special rules kick in.

These rules, the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO), are there to prevent what the Social Security Administration sees as "double-dipping."

The WEP and GPO adjust the Social Security benefit formula for individuals who receive a pension from non-covered employment. The goal is to align their benefit calculation more closely with that of workers who paid into Social Security their entire careers.

In simple terms, WEP can lower your own Social Security retirement benefit, while GPO can reduce any spousal or survivor benefit you might be eligible for. These adjustments often catch public servants by surprise, so it's absolutely critical to factor them into your retirement plan if you have a government pension.

Working abroad can sometimes trigger similar adjustments. Social Security determination accounts for international work through the Windfall Elimination Provision (WEP) and special agreements that blend global credits without overlap. If you earned foreign income not covered by U.S. Social Security, WEP can change the benefit formula, potentially shrinking your monthly payment. For example, over 250,000 Americans face this annually, with average cuts around $500 monthly. However, with savvy planning, U.S. expats with 30 or more years of substantial U.S. earnings can avoid WEP entirely.

Common Questions About Your Social Security Amount

Thinking about how Social Security calculates your final number can bring up some very real, practical questions. After all, this isn't just theory—it’s about your family's financial security for years to come.

Let's dig into some of the most common points of confusion. Getting straight answers here will help you plan with a lot more confidence and make smarter decisions as retirement gets closer.

What Happens If I Don’t Have 35 Years of Earnings?

This is one of the most frequent questions we hear, and for good reason. If you have fewer than 35 years of earnings, the Social Security Administration (SSA) doesn't just ignore the missing years; they plug in a zero for each one.

Unfortunately, those zeros get averaged in with your actual earning years, which pulls down your Average Indexed Monthly Earnings (AIME). A lower AIME leads to a smaller Primary Insurance Amount (PIA) and, you guessed it, a reduced final benefit.

For instance, if you only worked for 30 years, your AIME calculation will have five big fat zeros dragging it down. This is exactly why even a few years of part-time work late in your career can be so valuable—a year of low earnings is always better for your calculation than a year with no earnings at all.

How Do Cost-of-Living Adjustments Affect My Benefit?

Cost-of-Living Adjustments, or COLAs, are a fantastic feature designed to protect your benefits from getting eaten away by inflation. They aren't guaranteed every single year, but they play a huge role in helping your retirement income keep up with rising prices.

Each year, the SSA looks at a specific inflation measure called the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If that index shows a significant jump, a COLA is announced for the next year.

Your monthly benefit then gets bumped up by that percentage, starting in January. For example, a 3.2% COLA on a $2,000 monthly benefit would increase it to $2,064. This adjustment happens automatically for everyone receiving benefits.

This built-in protection is one of the most powerful parts of Social Security, helping ensure your income doesn't lose its punch over a long retirement.

Can I Work and Still Receive Social Security Benefits?

Yes, you absolutely can, but there are some important rules to know if you claim benefits before you reach your Full Retirement Age (FRA). This is often called the "earnings test" or "earnings limit."

Here's how it works:

- If You're Under Your FRA for the Whole Year: The SSA will hold back $1 from your benefits for every $2 you earn above the annual limit. For 2024, that limit is $22,320.

- In the Year You Reach Your FRA: The rule gets a lot friendlier. In the months before your birthday month, the SSA holds back $1 for every $3 you earn above a much higher limit ($59,520 in 2024).

The moment you hit your Full Retirement Age, the earnings test vanishes completely. From that month on, you can work and earn as much as you like with absolutely no reduction in your Social Security benefits.

How Do Taxes Impact My Social Security Amount?

It comes as a surprise to many, but your Social Security benefits might be subject to federal income taxes. Whether you'll owe anything depends on what the IRS calls your "combined income."

It's a simple formula. You just add up three things:

- Your adjusted gross income (AGI)

- Any nontaxable interest you received

- Half of your Social Security benefits for the year

The tax thresholds are set by law. For 2024, if your combined income is between $25,000 and $34,000 (for single filers) or $32,000 and $44,000 (for joint filers), up to 50% of your benefits could be taxed. If your income is above those upper limits, up to 85% of your benefits may be taxable.

How Can I Get an Official Estimate of My Benefits?

The absolute best way to see what your future Social Security check might look like is to go straight to the source.

Head over to the official SSA.gov website and create a personal my Social Security account. This is a free, secure service that gives you direct access to your personalized Social Security Statement, which is built on your actual, real-life earnings record.

Inside your statement, you'll find a goldmine of information:

- Benefit Estimates: See exactly what the SSA projects you'll receive if you claim early at 62, at your Full Retirement Age, or if you wait until age 70.

- Disability Benefits: Find out what your potential monthly benefit would be if you became disabled and could no longer work.

- Survivor Benefits: See what your spouse, children, or other family members could receive in benefits upon your death.

- Earnings Record: You can review your entire work history year by year. This is your chance to make sure it's accurate and report any errors you spot.

Making a habit of checking your statement every year or two is a cornerstone of smart retirement planning. It gives you real numbers to work with and shows you exactly how your career choices are shaping your family's future security.

At Smart Financial Lifestyle, we believe in empowering you with clear information to make confident financial choices for your family's future. For more insights on building a secure retirement, visit us at https://smartfinancialifestyle.com.