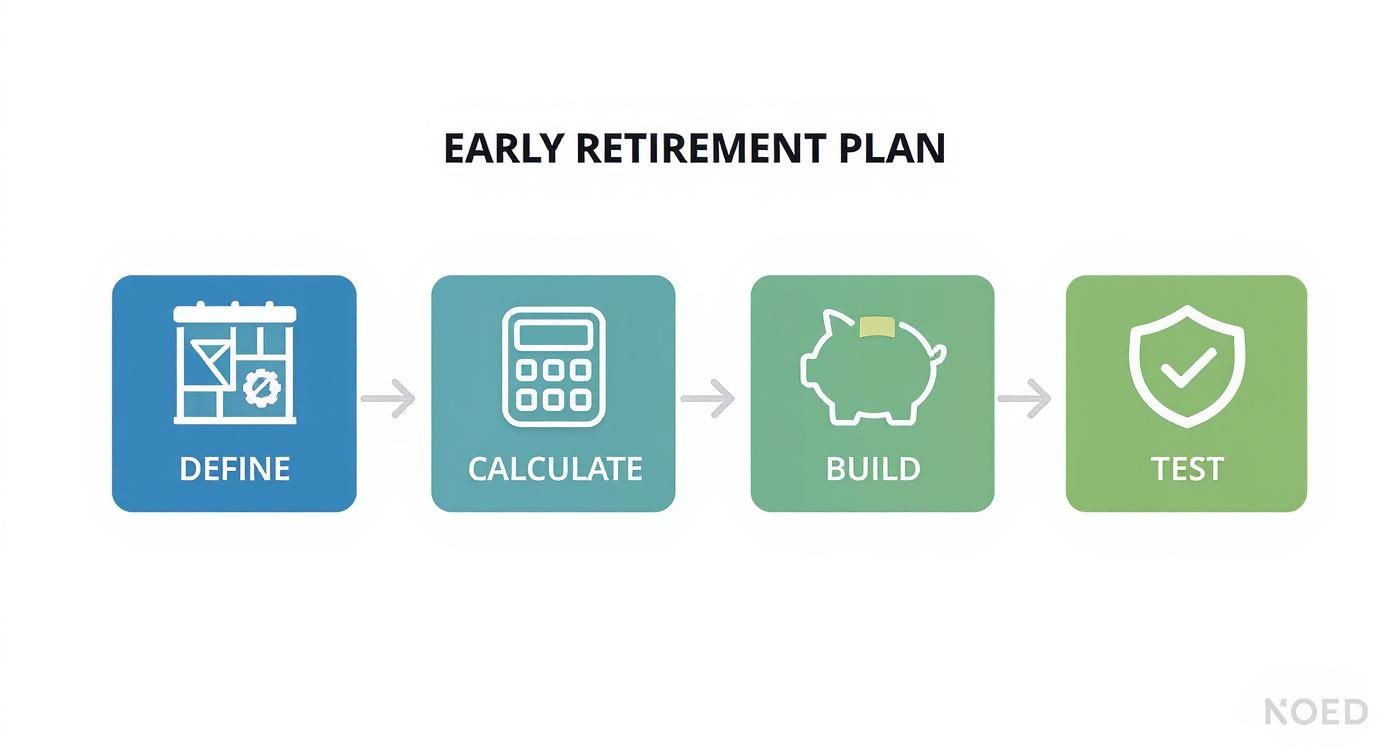

Wondering how to plan for early retirement? It’s not about some secret formula. It really boils down to a clear, actionable framework built on four foundational pillars:

- Defining your future lifestyle.

- Calculating your exact financial independence (FI) number.

- Building an aggressive wealth-generation engine.

- Stress-testing your plan for real-world challenges.

This structured approach is what makes the goal feel achievable instead of just some far-off, abstract dream.

Your Early Retirement Action Plan

Escaping the nine-to-five grind years ahead of schedule isn't about luck; it's the result of intentional, strategic planning. The journey to financial freedom can feel immense, but breaking it down into manageable stages turns a lofty dream into a concrete project. Think of this guide as your roadmap, designed to demystify the process one step at a time.

The first, and honestly most critical, step is envisioning what your life will actually look like post-work. This isn't just a daydreaming exercise—it's a practical necessity that forms the bedrock of all your financial calculations. Only from there can you translate that vision into a tangible financial target.

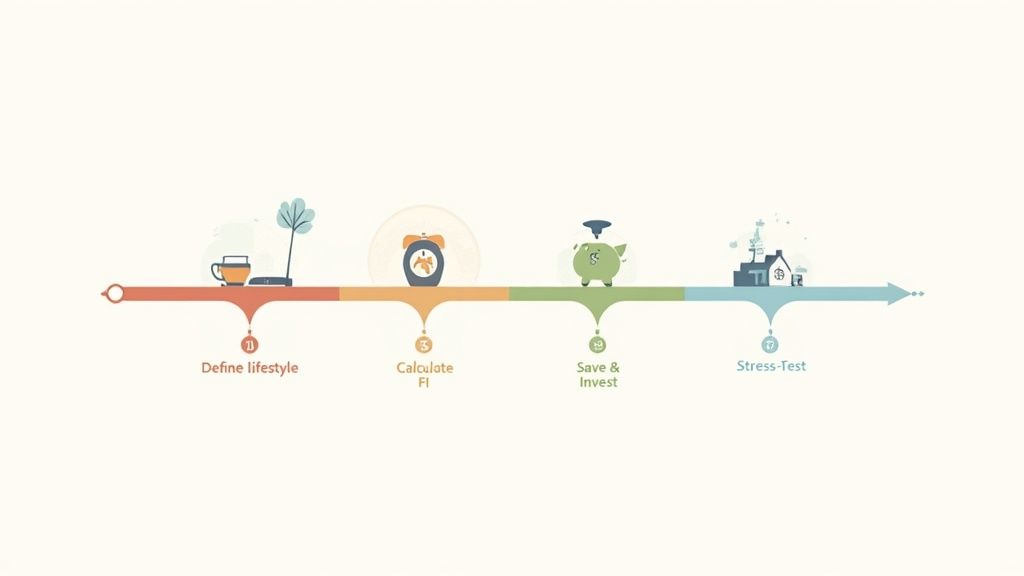

Defining Your Core Pillars

The path to early retirement follows a logical progression from vision to execution. Each stage builds upon the last, creating a solid and resilient strategy that can adapt to life's inevitable curveballs.

This simple flowchart lays out the four core pillars of a successful early retirement plan.

As you can see, it's a journey from the abstract "Define" phase to the concrete "Test" phase, which ensures your plan is both aspirational and practical.

The most effective retirement plans are not just spreadsheets and investment accounts; they are detailed blueprints for a life you are genuinely excited to live. Without a clear vision, financial targets are meaningless.

To help you get started, we’ve summarized these foundational pillars in the table below. Think of this as your high-level checklist for the entire journey. For a deeper dive into creating a quick and effective framework, our guide on The 15-Minute Retirement Plan is a great place to start.

Four Pillars of Early Retirement Planning

Understanding these stages is the first step toward building real momentum. This table breaks down the core objective of each pillar and gives you a simple, immediate action you can take to get started.

| Pillar | Core Objective | Your First Action |

|---|---|---|

| Define Your Vision | Create a clear picture of your desired post-work lifestyle, including location, hobbies, and daily routines. | Write down what an ideal week in early retirement looks like for you, from morning to evening. |

| Calculate Your Number | Determine the exact amount of money needed to fund your envisioned lifestyle indefinitely. | Estimate your projected annual retirement expenses and apply the 4% Rule to get a preliminary target. |

| Build Your Engine | Create and execute an aggressive savings and investment strategy to reach your financial target. | Max out contributions to tax-advantaged retirement accounts like a 401(k) or Roth IRA. |

| Test Your Plan | Ensure your financial strategy is resilient enough to withstand market downturns, inflation, and unexpected events. | Run a "fire drill" by simulating how your portfolio would perform during a past recession. |

Getting a handle on these four areas transforms the vague idea of "retiring early" into a series of clear, manageable steps you can start working on today.

Envisioning Your Post-Work Lifestyle

Before you run a single calculation or open a brokerage account, the real work of early retirement planning starts with a simple question: What will you actually do all day? This isn't just daydreaming; it's about crafting a concrete blueprint for your future. Your answers will shape every single financial decision you make from here on out.

The idea of leaving work for good often brings up images of endless vacations. But the truth is, a fulfilling retirement is built on purpose and engagement, not just escape. A vague goal like "travel more" isn't nearly enough to build a solid financial plan around.

From Vague Dreams to a Detailed Blueprint

It’s time to move past fuzzy ideas and get specific. The best way to do this is to ask yourself a series of pointed questions that paint a vivid picture of your ideal life after work. The more detail you can bring to this vision, the more accurate your financial projections will be.

Let's dig into some of the key lifestyle factors you need to think through:

- Your Home Base: Are you staying put in your current home? Downsizing to a condo? Maybe you’re planning a move to a place with a lower cost of living. That decision alone can dramatically alter your housing budget.

- Daily Routines: What does an ideal Tuesday look like for you? Is it filled with volunteering, taking classes at the local college, tending a garden, or finally getting that passion project off the ground?

- Travel Style: When you say "travel," do you mean month-long international backpacking trips or weekend getaways to nearby cities? A globetrotter's budget looks completely different from a homebody's.

- Hobbies and Passions: Are your interests expensive, like boating or woodworking? Or are they low-cost pursuits like hiking and reading? Be honest about what truly brings you joy.

Thinking through these details is what transforms a retirement plan from a boring spreadsheet into a life you are genuinely excited to live. This vision becomes your "why"—the motivation that will keep you focused through the years of saving and investing.

Your financial target is a direct reflection of your life choices. A plan to live a quiet, minimalist life in a rural town will require a fundamentally different nest egg than one designed for frequent international travel and city living.

For instance, a couple planning to downsize and pour their time into local community projects might aim for annual expenses around $50,000. On the other hand, a pair who wants to keep a larger home and take two big international trips per year could easily need $90,000 or more. This clarity is everything.

Defining Your Timeline and Trade-Offs

Once you have a clear vision, you can start mapping out a realistic timeline. This isn't about just picking a random age, like 50 or 55. It's about grappling with the financial realities and trade-offs that come with your target date.

Retiring at 45 versus 55 presents some massive differences:

- Shorter Accumulation Phase: Pulling the plug at 45 gives you ten fewer years to save and invest. That demands a much more aggressive savings rate to hit your goal.

- Longer Retirement Horizon: Your nest egg might need to last for 50 years or more, making it far more vulnerable to the long-term effects of inflation and market swings.

- Healthcare Bridge: You'll be on the hook for funding your own healthcare for 20 years before you become eligible for Medicare at age 65. That's a huge expense to plan for.

This process of envisioning your future also has a funny way of revealing what truly matters to you. Many people I've worked with find that their ideal retirement is actually less expensive than they initially imagined. For more ideas on filling your days with purpose, check out our guide on what to do during retirement.

Ultimately, this exercise is all about aligning your money with your values. By defining what your ideal life looks like, you create a personalized roadmap that makes the entire journey of planning for early retirement feel both meaningful and achievable.

Calculating Your Financial Freedom Number

Okay, you’ve pictured your ideal retirement. Now it’s time to put a price tag on it. Every solid early retirement plan hinges on one critical figure: your Financial Independence (FI) Number. This is the total amount you need invested to fund your lifestyle forever, without ever having to work for money again.

Think of it as your personal finish line. This isn't some fuzzy estimate; it's the specific target that will steer every saving and investing decision from here on out. The simplest way to find it is with the 4% Rule.

Understanding The 4% Rule

The 4% Rule is a classic retirement guideline. It suggests you can safely withdraw 4% of your starting portfolio value each year, adjust that amount for inflation annually, and have a very high chance of your money lasting at least 30 years.

To get your FI Number, you just flip the math: multiply your desired annual retirement income by 25.

Let's look at a couple of real-world examples:

- A couple wanting $70,000 per year to live on would need $1,750,000 invested ($70,000 x 25).

- A single person aiming for $40,000 annually would need a $1,000,000 nest egg ($40,000 x 25).

This quick calculation turns a vague dream into a concrete goal. But—and this is a big but—the rule isn't foolproof. It was built on historical data for a traditional 30-year retirement. If you're retiring early, you might need your money to last 40, 50, or even 60 years. For that kind of longevity, a more conservative withdrawal rate of 3% to 3.5% is probably a smarter move.

You can play around with different scenarios using our retirement withdrawal rate calculator. See for yourself how a small tweak can dramatically impact how long your money will last.

Projecting Your Annual Expenses

Your FI Number is only as good as the expense projection it’s built on. This step requires an honest and detailed look at what your life will actually cost in retirement. You need to account for everything, from the boring stuff to the fun stuff.

Start by breaking down your future budget into categories:

- Housing: Is your mortgage paid off? Don't forget to budget for property taxes, insurance, and the inevitable maintenance costs that pop up.

- Healthcare: This is the big one for early retirees, as you won't be eligible for Medicare until age 65. Get familiar with the ACA Marketplace and research potential premiums.

- Daily Living: This bucket covers groceries, utilities, transportation, and all the little things that keep life running.

- Discretionary Spending: What’s the point of retiring if you can’t enjoy it? Be sure to factor in your travel plans, hobbies, dining out, and entertainment.

- Taxes: Don't forget Uncle Sam. Withdrawals from traditional 401(k)s and IRAs are taxed as income, so that needs to be part of your spending plan.

Here's a secret I've learned over the years: the most powerful lever you have isn't picking the perfect stock—it's controlling your savings rate. How much you save matters far more than your investment returns, especially when you're just starting out.

Seriously, bumping your savings rate from 15% to 30% of your income can slash your time to retirement by more than half. That’s the magic of compound interest at work.

The Generational Savings Landscape

Of course, your ability to build this nest egg depends heavily on when you start. We see massive differences in retirement savings across generations, with age playing a huge role in preparedness.

For example, Baby Boomers have an average 401(k) balance of $249,300, while Gen X is a bit behind at $192,300. The gap gets wider with younger folks—Millennials average just $67,300, and Gen Z is just getting started with an average of $13,500.

These numbers tell a clear story: starting early is a game-changer. But no matter how old you are, the core principles don't change. Calculating your FI number gives you a clear target, transforming the abstract question of "how to plan for early retirement" into a specific, measurable goal you can chase down.

Building Your Wealth Generation Engine

Alright, you’ve got your target number. Now it’s time to build the engine that gets you there. This is where the rubber meets the road—turning strategy into action.

Building serious wealth isn't just about earning a big paycheck. It's about creating a system that saves and invests for you, day in and day out, almost on autopilot.

Think of it as playing both offense and defense with your money. Your offense is all about maximizing your income and investments. Your defense is about smart, surgical expense management. You have to master both to really shorten your timeline to financial freedom.

Maximize Your Tax-Advantaged Accounts

Your most powerful wealth-building tools are your tax-advantaged retirement accounts. Seriously, think of these as financial cheat codes. The money you put in here grows with huge tax benefits that can turbocharge your returns over the years.

Here’s the order of operations I recommend to almost everyone:

- Your 401(k) or 403(b): First things first. If your employer offers a match, contribute enough to get 100% of it. No excuses. It’s free money and an immediate, guaranteed return. Max it out if you can.

- Roth IRA: This is a brilliant tool for tax diversification. You contribute with after-tax money, which means your qualified withdrawals in retirement are completely tax-free. That’s a massive win.

- Health Savings Account (HSA): This is the unsung hero of retirement accounts. An HSA is a triple-tax-advantaged beast: your contributions are tax-deductible, the money grows tax-free, and you can withdraw it tax-free for qualified medical expenses.

Tackle these accounts in this "waterfall" sequence. It ensures you’re grabbing the best tax breaks first. Only after you’ve maxed these out should you even think about putting money into a regular taxable account.

Construct a Resilient Taxable Portfolio

Once your tax-advantaged accounts are humming along, the next piece of the puzzle is a taxable brokerage account. This account gives you total flexibility. For early retirees, this is critical because you can access this money before the traditional retirement age without penalties.

The heart of any good portfolio is asset allocation—how you split your money between different investments, mainly stocks and bonds. For most people chasing early retirement, the simplest and most effective strategy is to stick with low-cost index funds.

A common and solid approach for an early retiree is a portfolio weighted heavily toward stocks, maybe an 80/20 or even 90/10 split between total stock market index funds and total bond market index funds. This is a setup built for long-term growth.

This isn't about day trading or trying to find the next hot stock. It's about owning a tiny slice of the entire market and letting compound interest and broad economic growth do all the hard work for you. It's a proven, set-it-and-forget-it approach that helps keep emotions out of your financial decisions.

Play Both Offense and Defense

Building wealth is a two-sided coin. On one side, you have your offense—how much you earn. On the other, your defense—how much you keep. Focusing on just one side is like trying to row a boat with one oar. You'll just go in circles.

Financial Offense Strategies

- Career Growth: Don't just show up to work. Actively chase promotions, learn to negotiate your salary, and pick up skills that make you more valuable.

- Side Hustles: Got a skill or a passion? Turn it into a side hustle. Even an extra few hundred bucks a month can make a massive difference in your savings rate.

Financial Defense Strategies

- Strategic Spending: This isn't about depriving yourself of everything you enjoy. It’s about being intentional. Spend lavishly on the things you love and cut costs ruthlessly on everything else.

- Diligent Tracking: You can't optimize what you don't measure. Use a budgeting app or a simple spreadsheet to see exactly where your money goes. Awareness is everything.

Let's look at a quick example. A family brings in $120,000 and saves 15% of it ($18,000 a year). Then, they get strategic. A negotiated raise adds $10,000, a small side business brings in another $8,000, and they slash $6,000 by cutting unused subscriptions and dining out less.

Suddenly, their total available for savings jumps to $42,000. Their savings rate skyrockets to 32% of their new $138,000 income. That one year of focused effort just shaved years off their retirement timeline.

Combining earning more with spending less creates a powerful "savings gap" that fuels your investments. It might feel like a long road, but the mindset around retirement is changing for the better. In America, just 21% of people now believe it will take a "miracle" to retire comfortably, a huge improvement and way more optimistic than the global average of 43%. You can read more about these global retirement insights to see the bigger picture. This shift shows that with a solid game plan, retiring early is more possible than ever.

Solving The Healthcare and Tax Puzzle

Let's be blunt: few things can wreck a solid early retirement plan faster than healthcare costs and taxes. These aren't just minor budget items you can figure out later. They are massive financial hurdles that need their own dedicated strategy.

If you get this part right, you protect your hard-won freedom. But if you overlook them, you could find yourself burning through your nest egg years, or even decades, ahead of schedule.

For anyone aiming to retire before age 65, healthcare is the big, scary question mark. You're on your own until Medicare kicks in, and building that bridge can get very expensive, very fast. In the same way, how you pull money from your accounts can mean the difference between paying a little in taxes or a whole lot.

Navigating The Pre-Medicare Healthcare Maze

The moment you leave your job, you also leave its subsidized health insurance behind. For many new early retirees, this is the single biggest financial shock of the entire transition. The good news? You have options. Understanding them is the first step.

Here are the most common paths people take:

- ACA Marketplace (Obamacare): This is the go-to for most early retirees. The magic here is that your eligibility for subsidies hinges on your Modified Adjusted Gross Income (MAGI). If you can carefully manage your income through strategic withdrawals, you can qualify for huge premium tax credits that make coverage affordable.

- Short-Term Health Plans: These are much cheaper upfront, but the coverage is thin. They often won't touch pre-existing conditions and are definitely not a long-term fix. Think of them as a temporary patch to fill a gap, not the foundation of your healthcare plan.

- COBRA: This lets you keep your old employer's coverage for up to 18 months. While the continuity is nice, you'll be paying 100% of the premium plus an administrative fee. It’s almost always a painfully expensive choice.

The single most powerful tool for managing healthcare costs in early retirement is controlling your taxable income. A low "on-paper" income can unlock massive ACA subsidies, turning a premium that looks impossible into a manageable monthly expense.

Let’s look at how this plays out for a hypothetical 55-year-old couple just starting their early retirement.

Pre-Medicare Healthcare Options Comparison

As you'll see in this table, the trade-offs between different healthcare options are stark. Cost, coverage, and who it's best for vary dramatically.

| Coverage Option | Best For | Potential Downside | Typical Cost Structure |

|---|---|---|---|

| ACA Marketplace | Long-term coverage with potential for significant premium subsidies. | Premiums can be high without subsidies; network limitations are possible. | Monthly premium, with potential tax credits based on income. |

| COBRA | Individuals who want to maintain their exact same coverage for a short period. | Extremely expensive as you pay the full premium plus an admin fee. | High fixed monthly premium. |

| Short-Term Plan | Healthy individuals needing temporary coverage between other plans. | Does not cover pre-existing conditions; limited benefits and high out-of-pocket costs. | Low monthly premium, but with very high deductibles. |

Choosing the right path here is absolutely critical to making your retirement numbers work.

Designing a Tax-Efficient Withdrawal Strategy

Just as critical as healthcare is how you handle taxes. The goal isn't just to have enough money; it's to keep as much of that money as you possibly can. A smart withdrawal strategy can literally save you tens, or even hundreds, of thousands of dollars over the course of your retirement.

The key is realizing that different accounts are taxed differently. Your traditional 401(k) or IRA withdrawals? Taxed as ordinary income. Qualified Roth IRA withdrawals? Completely tax-free. Investments in a taxable brokerage account? Subject to capital gains taxes, which are often much lower than income tax rates.

One of the most powerful tools in the early retiree's playbook is the Roth conversion ladder. This involves converting a piece of your traditional IRA or 401(k) to a Roth IRA each year. You’ll pay income tax on the amount you convert that year, but after five years, you can pull out that converted principal completely tax-free.

This is a game-changer for two big reasons:

- It gives you a way to access retirement funds before age 59½ without getting hit with a penalty.

- You can strategically do these conversions in your low-income years to "fill up" the lower tax brackets, dramatically cutting your lifetime tax bill.

Another essential but often overlooked concept is asset location. This simply means putting your tax-inefficient investments (like bonds that spit out regular income) inside your tax-advantaged accounts. Meanwhile, your tax-efficient investments (like stock index funds) go in your taxable brokerage accounts. This simple organization minimizes the annual tax drag on your portfolio, letting your money grow faster.

By weaving these tax and healthcare strategies into your early retirement plan from day one, you're building a financial foundation that is not just sufficient, but truly resilient.

Making Your Plan Resilient to Market Shocks

Getting a big pile of money saved up is really only half the battle. A truly solid early retirement plan isn't just about growth; it’s about being tough enough to take a punch. Your plan has to withstand the market shocks, inflation spikes, and surprise life events that are pretty much guaranteed to happen over a retirement that could last decades.

This means you need to shift your thinking from pure accumulation to wealth preservation. The strategies that get you to retirement are often very different from the ones that keep you in retirement. It’s all about building a financial fortress that can bend without breaking when the economic storms roll in.

Stress-Testing Your Portfolio

Let's be blunt: hope is not a strategy. The first thing you need to do is see how your portfolio would have held up during past meltdowns. Go back and look at historical events like the 2008 financial crisis or the dot-com bust of the early 2000s. If you were already retired then, would your portfolio have survived?

This exercise isn't meant to scare you. It’s designed to expose weaknesses in your plan. If a historical stress test shows your nest egg would have been wiped out, that's a bright red flag telling you to rethink your asset allocation or withdrawal strategy before it’s too late.

A plan that only works in a bull market is not a plan—it's a gamble. True financial freedom comes from knowing your lifestyle is secure even when the market is chaotic and unpredictable.

Uncertainty is now a huge factor in how people are planning for early retirement. All the recent market volatility has a lot of folks second-guessing their timelines. One survey showed an 8% drop in workers planning to retire before age 65, with over a third changing their plans because of economic worries. You can explore more about how market shifts impact retirement confidence on SSGA.com.

Beyond the 4% Rule with Flexible Withdrawals

Clinging to the rigid 4% Rule can be a dangerous blueprint, especially during volatile markets. A much more resilient approach involves using dynamic or flexible withdrawal strategies. This gives your portfolio some crucial breathing room when the market takes a nosedive.

Here are a few adaptive strategies I've seen work well:

- The Guardrail Method: You set an upper and lower "guardrail" for your portfolio's value. If the market soars and you hit the upper rail, you take out a bit more money. If it crashes and you hit the lower rail, you temporarily tighten your belt and reduce spending.

- Variable Percentage Withdrawal: Instead of pulling out a fixed dollar amount, you withdraw a set percentage of your portfolio's value each year. This automatically adjusts your income to how the market is doing—you spend more in the good years and less in the bad ones.

These methods build adaptability right into your plan. They force you to be disciplined when markets are down, preventing you from the catastrophic mistake of selling too many shares at the worst possible time and locking in those losses. This flexibility is the absolute key to making your money last for a 40, 50, or even 60-year retirement.

Got Questions About Retiring Early? We've Got Answers.

As you start getting serious about early retirement, a lot of "what if" scenarios probably run through your head. It's completely normal. Let's walk through some of the most common questions that come up on the journey to financial independence.

What If I Get Bored? I Can't Just Do Nothing All Day.

This is a huge one, and it trips up more people than you'd think. The fear of an empty calendar is real. My best advice? "Practice" retiring before you actually pull the trigger.

Take a solid week or two off from work—and I mean a real break, no checking emails—and try to live out what you imagine your retired life will look like.

An intentional trial run is the best way to test your assumptions. You might discover that the globetrotting life you dreamed of isn't as fulfilling as you thought, or that a quiet life at home is exactly what you need.

This little experiment helps you iron out the kinks in your vision. It's about building a post-work life filled with purpose, not just killing time.

Seriously, How Much Is Really Enough?

Ah, the million-dollar question (sometimes literally). While the 4% Rule is a fantastic starting point for planning, the "right" number is deeply personal. It's all tied to your spending habits, future healthcare costs, and the kind of lifestyle you want to live. For a retirement that could last 30, 40, or even 50 years, being a little conservative is just plain smart.

In fact, many early retirees find that a 3.5% withdrawal rate gives them a much bigger safety net. This helps buffer against inevitable market swings and surprise inflation spikes.

Can I Still Make Money After I "Retire"?

Absolutely! Retiring early doesn't mean you have to vow to never earn another dollar. Plenty of people find a ton of joy—and extra cash—by working part-time, consulting in their old field, or even turning a hobby into a small business.

This approach, sometimes called a "staged retirement," does more than just supplement your income. It keeps you engaged, connected, and can take a lot of financial pressure off your investment portfolio while you ease into your new life.

At Smart Financial Lifestyle, we believe in building a life from which you don't need an escape. Learn how to align your finances with your deepest values by exploring our resources at https://smartfinancialifestyle.com.