Avoiding probate isn't just a legal maneuver; it's about keeping your family's financial life private, saving a ton of time, and making sure the assets you've worked for actually end up with your loved ones. The most reliable ways to do this involve tools like revocable living trusts, correctly naming beneficiaries on your accounts, and using joint ownership to let assets pass directly, no court required.

Why Avoiding Probate Should Be Your Priority

So what is probate, really? It’s the formal court process that gives a will its legal stamp of approval and oversees how a deceased person’s assets are distributed. On paper, it sounds fine. But in reality, for most families, it's a long, frustrating journey filled with delays, unexpected costs, and a total loss of privacy.

Because it's a public affair, your will—along with a detailed list of everything you own—becomes a public record. Anyone can look it up.

For the people you leave behind, this process can freeze critical assets for months, sometimes even years. This makes it incredibly hard to pay bills or manage finances during what's already a deeply emotional time. And the costs? Court fees, executor payments, and attorney bills can take a serious bite out of the inheritance you meant for them to have.

The Real-World Impact on Your Family

The drive to steer clear of probate court is both personal and practical. It’s not just about being financially savvy; it’s about shielding your family from a difficult and unnecessary ordeal. Taking a few proactive steps now can deliver some huge wins for them later:

- Maintain Privacy: Your family's financial details, asset values, and debts stay confidential—not filed away in a public courthouse for anyone to see.

- Save Time: Assets can find their way to your heirs in a matter of weeks, a stark contrast to the typical 18-24 months many probate cases drag on for.

- Reduce Costs: You sidestep hefty court fees and dramatically cut down on legal bills, keeping more of your estate intact for your beneficiaries.

- Ensure Continuity: Your family gets immediate access to the funds and property they need, preventing financial chaos when they are at their most vulnerable.

The whole point of smart estate planning is simple: make things as easy as possible for the people you love after you’re gone. Avoiding probate is one of the most powerful ways to give them—and yourself—that peace of mind.

Probate vs Non-Probate Asset Transfer at a Glance

To see the difference clearly, it helps to put the two paths side-by-side. Here’s a quick look at how assets get from you to your heirs, with and without court involvement.

| Factor | Through Probate Court | Using Avoidance Strategies (e.g. Trust) |

|---|---|---|

| Privacy | Public record; anyone can view asset details. | Completely private; details stay within the family. |

| Timeline | Typically 18-24 months, often longer. | Usually settled within a few weeks to months. |

| Cost | High; includes court fees, legal bills, executor fees. | Minimal; usually just initial setup costs for a trust. |

| Control | Court supervised; little flexibility for the family. | Controlled by your designated successor trustee. |

| Access to Assets | Assets are frozen until the court grants access. | Immediate access for beneficiaries. |

As you can see, the benefits of planning ahead are substantial, turning a potential bureaucratic nightmare into a smooth, private transition for your family.

A Glimpse at the Numbers

The scale of this issue is massive. Every year, courts across the United States handle over 1.2 million probate cases. With the average process taking about 20 months, it’s a far cry from estates managed through trusts, which are often wrapped up in just a few months.

In fact, families who use trusts can slash the time and cost of settling an estate by up to 70%. You can explore more probate statistics to get the full picture of these delays and expenses.

This guide will walk you through the proven strategies to sidestep this cumbersome process, from the comprehensive protection of a living trust to simple yet powerful beneficiary updates. These complexities are especially important to consider in unique family structures, and our guide on estate planning for blended families offers tailored insights.

Using a Revocable Living Trust to Bypass Probate

When you're serious about letting your family sidestep probate court, the revocable living trust is one of the most powerful tools you can have. It might sound intimidating, but the idea is actually quite simple. Think of it as creating a private, secure container for your most valuable assets.

Instead of holding property in your own name, you transfer it into the name of your trust. You don't lose an ounce of control—you remain the trustee, managing everything exactly as you did before. The "revocable" part is what gives you flexibility; you can change it, add assets, or even cancel the whole thing whenever you want.

When you pass away, anything held inside the trust is shielded from the probate process. Your chosen successor trustee—maybe a trusted child, a relative, or a professional—simply follows the private instructions you left in the trust document. This lets them distribute assets directly to your beneficiaries without any court supervision, saving everyone a massive amount of time, money, and stress.

How a Living Trust Works in the Real World

Let's make this tangible. Imagine a couple, Sarah and Tom, who own a home, a joint savings account, and an investment portfolio. If they only have a will, all those assets get tangled up in their probate estate, becoming part of a public court record.

Instead, they set up the "Sarah and Tom Family Trust." Here’s what that looks like in practice:

-

Drafting the Trust Document: They meet with an attorney to create the trust agreement. This legal document names them as the initial trustees, their children as the beneficiaries, and appoints a successor trustee to take over after they're both gone.

-

Funding the Trust: This is the most important part of the whole process. They have to actually retitle their assets into the trust's name. The deed to their house is changed from "Sarah and Tom" to "Sarah and Tom, Trustees of the Sarah and Tom Family Trust."

-

Updating Financial Accounts: They do the same for their savings and brokerage accounts, changing the ownership to the trust. The accounts now technically belong to the trust, but Sarah and Tom still have full authority to make deposits, withdrawals, and investment decisions.

The payoff? When Sarah and Tom pass away, their successor trustee can step in and manage these assets immediately. They can pay final bills, sell the house if needed, and give the remaining funds to the children based on the trust's rules—all done privately and efficiently.

A trust is like a pre-written script for your assets. It tells your successor trustee exactly what to do, who gets what, and when, allowing them to skip the lengthy and public court performance of probate.

The Critical Step of Funding Your Trust

Just creating the trust document is only half the job. An unfunded or partially funded trust is one of the most common and costly mistakes people make. If an asset isn't formally retitled into the trust's name, it stays outside its protection and will almost certainly end up in probate court anyway.

To make sure your trust works as designed, you have to be diligent about transferring ownership.

- Real Estate: You'll need to sign and record a new deed for every property.

- Bank Accounts: Head to your bank with a copy of your trust certificate to retitle checking, savings, and money market accounts.

- Non-Retirement Investments: Work with your financial advisor to change the ownership on brokerage accounts and mutual funds.

- Business Interests: Ownership in an LLC or other business also needs to be formally assigned to the trust.

This entire process, known as funding the trust, is what gives the strategy its power. It’s an administrative task upfront that pays off enormously in saved time, money, and headaches for your loved ones down the road. If this is new to you, it helps to learn more about what a revocable living trust is and the powerful protection it provides.

Beyond Probate Avoidance: Additional Benefits

While skipping probate is a huge win, a revocable living trust offers other key advantages that a simple will just can't match.

It creates a clear plan for managing your finances if you become incapacitated. If an illness or injury leaves you unable to handle your own affairs, your designated successor trustee can step in immediately. They can pay your bills and manage your investments for your benefit, avoiding the need for a court to appoint a conservator.

A trust also gives you far more control over how and when your beneficiaries get their inheritance. You can specify that assets should be held until a beneficiary reaches a certain age, create funds for education, or even set up a lifetime trust to protect assets from a beneficiary's creditors or a future divorce. This level of customized planning is a powerful way to make sure your legacy is handled with the care and wisdom you intended.

The Power of Smart Beneficiary Designations

You might be surprised to learn that one of the simplest and most effective ways to bypass probate is already built into many of your most valuable accounts. We're talking about assets like your 401(k), IRA, life insurance policies, and annuities. These don't have to get tangled up in your will.

Instead, they can pass directly to your loved ones through a simple form: the beneficiary designation.

This is a powerful tool because it creates a direct, contractual transfer. When you pass away, the financial institution is legally obligated to give the funds to the person you named on that form. Your will has no say in the matter, and the probate court is completely sidestepped.

Why This Simple Form Is So Critical

Think of a beneficiary designation as a specific instruction that overrides your will's general directions. While your will lays out a broad plan for your estate, these forms are like express lanes for certain assets. They get money into your family's hands quickly, often within weeks, rather than being frozen for months—or even years—in probate.

This speed is crucial. Life insurance proceeds might be needed right away to cover final expenses or replace lost income. Retirement funds could be essential for a surviving spouse's financial stability. By using these forms correctly, you provide your family with critical cash flow right when they need it most.

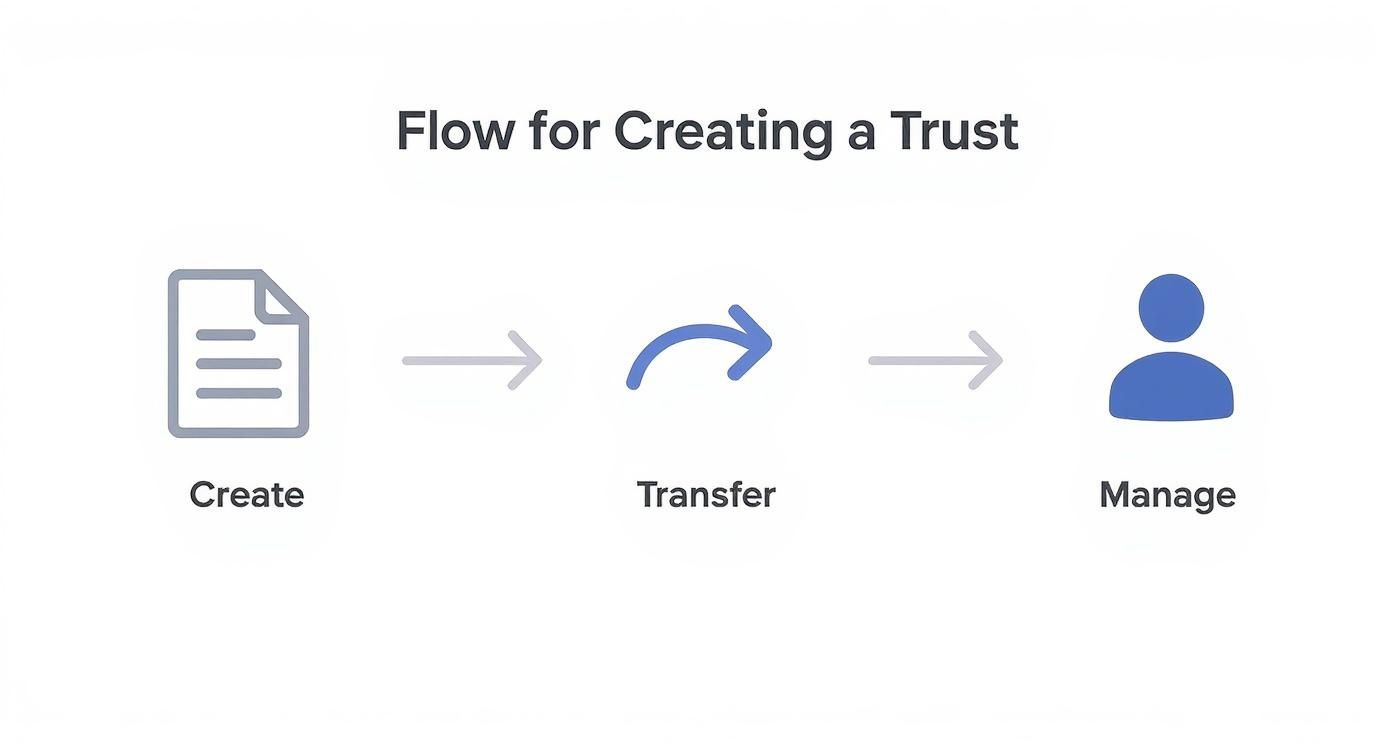

This graphic shows a simplified view of how another key probate-avoidance tool, a trust, is put into action.

The visual highlights the core steps of creating, transferring, and managing assets within a trust, which is another deliberate, structured approach to planning your estate.

The Dangers of Outdated Beneficiary Forms

Forgetting to review and update your beneficiaries is one of the most common—and heartbreaking—estate planning mistakes I see. Life changes, but these forms don't update themselves. A major event like a divorce, a new marriage, or the death of a named beneficiary can make your original intentions totally irrelevant.

Consider this all-too-common scenario: John named his wife as the primary beneficiary on his life insurance policy. Years later, they divorced, and John remarried. He remembered to update his will, leaving everything to his new spouse, but he completely forgot about that old insurance form. When John passed away, the insurance company was contractually bound to pay the entire death benefit to his ex-wife. His current wife got nothing from that policy.

An outdated beneficiary form can unintentionally disinherit the people you love most. It’s a simple piece of paper with the power to override your most current wishes and create lasting family conflict.

This isn’t just about ex-spouses, either. If your named beneficiary passes away before you and you haven't named a backup, that asset could be forced right back into your probate estate by default.

Your Action Plan for Auditing Beneficiaries

To prevent these kinds of disasters, it's essential to do a regular audit of all your accounts. Don't just assume you remember who you named years ago—get it in writing.

Here’s a practical checklist to get you started:

- Create a Master List: Make a complete inventory of every single account that has a beneficiary designation. This includes retirement plans (401(k)s, 403(b)s, IRAs), life insurance policies, annuities, and any bank or brokerage accounts with a Payable-on-Death (POD) or Transfer-on-Death (TOD) form.

- Request Current Forms: Call each financial institution and ask for a copy of your current beneficiary designation form on file. Don't hang up until they've confirmed it's on the way. Keep these with your other important estate planning documents.

- Name Both Primary and Contingent Beneficiaries: Always name a primary beneficiary—the first person in line. Just as important, you must also name a contingent beneficiary. This is your backup, the person who inherits if your primary beneficiary has already passed away or refuses the inheritance.

- Be Specific: When naming beneficiaries, use their full legal names and their relationship to you (e.g., "Jane Marie Smith, Spouse"). Stay away from vague terms like "my children," as this can create confusion and legal challenges down the road.

- Schedule Regular Reviews: Set a recurring reminder on your calendar to review these designations every one to two years. More importantly, make it a non-negotiable rule to check them immediately after any major life event.

By being meticulous with these simple forms, you ensure your assets go exactly where you want them to, without the cost, delay, and publicity of probate court.

Leveraging Joint Ownership the Right Way

Owning property with someone else seems like one of the most straightforward ways to make sure it passes on without a headache. And a lot of the time, it is. When it's set up correctly, this strategy can be a fantastic tool for keeping your most valuable assets out of a probate courtroom.

The magic is in a specific legal structure called Joint Tenancy with Right of Survivorship (JTWROS). It sounds technical, but the concept is simple: when one owner passes away, their share automatically and instantly transfers to the surviving owner.

That’s it. No court, no will, no delay. The asset never even touches the deceased's probate estate. It's a direct, seamless handoff, which is why you see it used so often for major assets like a family home, a primary bank account, or even a car title. For married couples, it's practically a foundational piece of their estate plan.

Understanding the Automatic Transfer

That "right of survivorship" is the most critical part of the equation. It's a legal principle that overrules anything you might have written in your will.

Let's say you and your brother own the family vacation cabin as joint tenants with the right of survivorship. In your will, you've stated that your half of the cabin should go to your daughter. As soon as you pass away, that part of your will becomes irrelevant for the cabin. The deed takes precedence, and your brother instantly becomes the sole owner.

This makes JTWROS incredibly powerful for avoiding probate, but it also means you have to be absolutely sure that the automatic transfer is what you want. There are no take-backs.

The Hidden Risks of Adding a Joint Owner

On the surface, adding a joint owner—especially a non-spouse like one of your kids—looks like a simple fix. But this is where things can get messy, creating problems you likely never saw coming.

Think about a common scenario. An aging mother, Mary, adds her responsible son, David, to her life savings account. Her intentions are good. She wants him to easily pay her bills if she gets sick and to inherit the money quickly when she's gone, avoiding probate.

But that simple move just opened a Pandora's box of potential issues:

-

Exposure to Their Creditors: The second David's name is on that account, the law sees that money as partially his. If David runs into financial trouble—a divorce, a lawsuit, even bankruptcy—his creditors can now legally seize the money in that "joint" account to pay his debts. Mary’s life savings are suddenly at risk because of something that has nothing to do with her.

-

Unintended Gifting: When you add a non-spouse as a joint owner, you're legally making a gift of half the asset. If it's a large account or a paid-off house, that "gift" could be large enough to require you to file a federal gift tax return. It's an unexpected tax complication most people don't consider.

-

Loss of Control: Once you add a joint owner, you're no longer the sole decision-maker. Want to sell that jointly owned property? You need their signature. This can easily lead to family disagreements if your goals and your child's goals suddenly diverge.

Adding a child as a joint owner on an asset might feel like a convenient shortcut, but it's like handing them a key to your financial house. You're also giving their financial problems a key to your house, too.

A Better Approach for Many Families

Because of these serious risks, using joint ownership with your kids or other relatives is often not the best way to avoid probate. It works beautifully for married couples in most states, but the potential for disaster with non-spouses is just too high.

Fortunately, there are much safer alternatives that accomplish the exact same goal.

- For bank accounts, a Payable-on-Death (POD) designation is a far better choice. It keeps the account out of probate but doesn't give your child any ownership rights (or risks) while you're alive.

- For your home, a Transfer-on-Death (TOD) deed (in states that allow it) or putting the property into a revocable living trust are superior options.

These strategies give you the probate-avoidance benefits you're looking for without exposing your life's savings to someone else's creditors or accidentally giving up control of your own assets. You maintain full command during your lifetime and ensure a smooth transfer when the time comes.

More Practical Ways to Keep Your Estate Out of Court

While living trusts and joint ownership are heavy hitters in estate planning, they're not the only tools in the shed. Several other straightforward strategies can keep specific assets out of the court system, and honestly, some of them are incredibly easy to set up.

Think of these as direct instructions for your assets. They ensure your property goes exactly where you intend it to, without the typical probate delays. Many just require filling out a simple form at your bank or brokerage, making them a key part of a well-rounded plan.

Use TOD and POD to Your Advantage

Transfer-on-Death (TOD) and Payable-on-Death (POD) designations are probably the simplest probate-avoidance tricks in the book. They essentially turn your regular financial accounts into assets that pass directly to your chosen heir.

You'll find POD designations on liquid accounts like checking, savings, and CDs. You just ask your bank for their POD form, name a beneficiary, and you're done. When you pass away, that person can claim the money with a death certificate and proper ID.

TOD designations work the same way but for investment accounts—think brokerage accounts holding stocks, bonds, and mutual funds. You name a beneficiary, and those securities transfer to them outside of probate. The best part? During your lifetime, the beneficiary has zero access to or control over these accounts.

These designations are completely revocable. If you change your mind, you just fill out a new form to name a different beneficiary. This flexibility is a huge plus, letting your estate plan evolve as your life does.

It's a clean, effective way to handle your most common financial assets. But keep in mind, these tools only transfer assets; they don't manage them. For a deeper dive into the duties involved in managing finances for someone else, our guide on financial responsibilities under a power of attorney has the details you'll want to know.

Keep Your Home Out of Probate with a TOD Deed

What about your house? For many people, it's their single largest asset. Luckily, the same transfer-on-death concept has been extended to real estate. Many states now allow Transfer-on-Death Deeds (TODDs), sometimes called beneficiary deeds.

This powerful tool lets you name someone to inherit your real estate automatically, sidestepping probate entirely. Here's the play-by-play:

- First, you sign and record a TODD at your county recorder's office, just like any other property deed.

- While you're alive, nothing changes. You keep complete ownership and can sell, refinance, or rent the property without anyone's permission.

- After you pass, your beneficiary just needs to file your death certificate with the county, and they officially become the new owner.

This is a fantastic alternative to putting a child on your deed as a joint owner, which can expose your home to their creditors, lawsuits, or divorce proceedings.

Check if You Qualify for Small Estate Procedures

What happens if your estate is on the smaller side? Most states have recognized that forcing a modest estate through the full-blown, expensive probate process doesn't make much sense. Their solution is a set of simplified procedures, often using a small estate affidavit.

Instead of a formal court case, an heir can use a simple sworn statement—the affidavit—to claim property. For families with fewer assets, this is one of the best answers to the question of "how to avoid probate court."

The main catch is that every state has its own definition of a "small" estate, setting a cap on its total value. The thresholds vary wildly, from as low as $25,000 in some places to more than $180,000 in others.

To give you an idea of how much these limits can differ, here’s a quick look at a few states.

Sample Small Estate Affidavit Thresholds by State

| State | Personal Property Limit | Real Estate Limit | Notes |

|---|---|---|---|

| California | $184,500 | $61,500 | Total estate value cannot exceed $184,500, but certain assets are excluded from the calculation. |

| Florida | $75,000 (Summary Admin) | Homestead is exempt | Florida offers "Summary Administration" for estates under $75,000 and "Disposition Without Administration" for very small estates covering final expenses. |

| Texas | No set dollar limit | No set dollar limit | Eligibility is more nuanced, depending on assets exceeding debts (excluding the homestead) and whether all heirs agree on the plan. |

It's crucial to remember that these figures can be updated by state legislatures, so always double-check the current laws where you live. If your estate falls under your state's limit, your loved ones could potentially settle your affairs in weeks, not months, saving a lot of time, money, and stress.

Answering Your Top Questions About Avoiding Probate

As you start putting these powerful estate planning strategies in place, it’s completely normal for questions to bubble up. The world of trusts, beneficiaries, and deeds has its own language, and getting clarity is the smartest thing you can do. We've put this section together to give you direct, straightforward answers to the most common concerns we hear from families, cutting through the confusion so you can move forward with total confidence.

Knowing how to sidestep probate court is one thing, but feeling certain about the details is what brings real peace of mind. Let’s tackle some of the most frequent questions head-on.

Do I Still Need a Will if I Have a Trust?

Yes, you absolutely do. This is a critical point that trips a lot of people up. A will and a trust don’t compete; they work together as a team to protect your family. When your estate plan is built around a trust, your will is often called a "pour-over will."

Think of it as your ultimate safety net. Its main job is to catch any assets you might have forgotten to formally transfer into your trust during your lifetime. The pour-over will directs that these leftover assets be "poured over" into the trust after you pass away. While these specific assets might still have to go through probate, the will ensures they ultimately end up where you intended, managed under the rules you already set in your trust.

More importantly, a trust cannot do one very specific, crucial job: name legal guardians for your minor children. That is a role exclusively for a will. Without a will, a court will make that deeply personal decision for you, and it might not be the choice you would have wanted for your kids.

Is Setting Up a Trust More Expensive Than Probate?

This is a classic "pay me now or pay me later" scenario, but the numbers almost always favor paying now. Setting up a revocable living trust means an upfront investment with a qualified attorney to draft the documents correctly, which can be a few thousand dollars. It’s a one-time cost to get your plan structured right.

In contrast, probate costs are paid by your estate after you're gone. These fees are often much, much higher, frequently calculated as a percentage of your estate's total value. This can include:

- Court filing fees

- Executor compensation

- Attorney's fees

- Appraisal costs

For most families, the initial cost of creating a trust is a drop in the bucket compared to the thousands—or even tens of thousands—of dollars their estate would later lose to the probate process.

The upfront cost of a trust is a planned expense that buys your family privacy, speed, and simplicity. Probate costs are an unplanned drain on their inheritance that buys them delay and frustration.

How Often Should I Review My Estate Plan?

An estate plan is not a "set it and forget it" document. Your life changes, and your plan needs to evolve right along with it. A good rule of thumb is to pull out your documents and give them a thorough review every three to five years.

However, some events should trigger an immediate review. These are non-negotiable moments to check in and make sure your plan still reflects your wishes and protects the people you love. These life events include:

- Marriage or divorce

- The birth or adoption of a child or grandchild

- The death of a spouse, beneficiary, or named trustee

- A significant change in your financial situation (like selling a business or receiving an inheritance)

- Moving to a different state, as estate and probate laws can vary widely

A quick review can prevent enormous headaches down the road and ensure your plan works exactly as you designed it to when your family needs it most.

It's natural to have questions as you navigate the ins and outs of estate planning. Below, we've compiled a few more common queries to help provide even more clarity.

Frequently Asked Questions

| Question | Answer |

|---|---|

| Do I still need a will if I have a living trust? | Yes, it's highly recommended. A will, often called a 'pour-over will' in this context, acts as a safety net. It ensures any assets you forgot to put into your trust are 'poured over' into it upon your death, though these assets may have to go through probate first. It also lets you name guardians for minor children, which a trust cannot do. |

| Can I completely avoid probate for all my assets? | It's possible to avoid probate for the vast majority of assets through careful planning. By using a combination of a funded living trust, beneficiary designations, and joint ownership, most major assets can bypass the court process. However, small, overlooked assets or those acquired right before death might still require some level of probate administration. |

| Is setting up a trust more expensive than probate? | Setting up a trust has an upfront cost for legal drafting, which can range from a few thousand dollars. In contrast, probate costs are paid by your estate after you're gone but are often much higher, typically calculated as a percentage of the estate's value. For many, the initial investment in a trust is significantly less than the fees, court costs, and delays their family would face in probate. |

| How often should I review my estate plan? | It's a good practice to review your estate plan every 3-5 years or after any major life event. This includes marriage, divorce, the birth or death of a family member, a significant change in your financial situation, or moving to a new state, as state laws can vary significantly. |

Getting these details right is the key to a plan that truly works. Taking the time to understand them now is a gift you give your future self—and your family.

At Smart Financial Lifestyle, we believe that making smart financial decisions is about creating peace of mind for you and a lasting legacy for your family. A well-crafted estate plan is a core part of that journey.

Explore more resources and insights to build your family's financial future at https://smartfinancialifestyle.com.